April 2026 Alberta Mortgage Rate Update: Where Rates Sit and What Happens Next

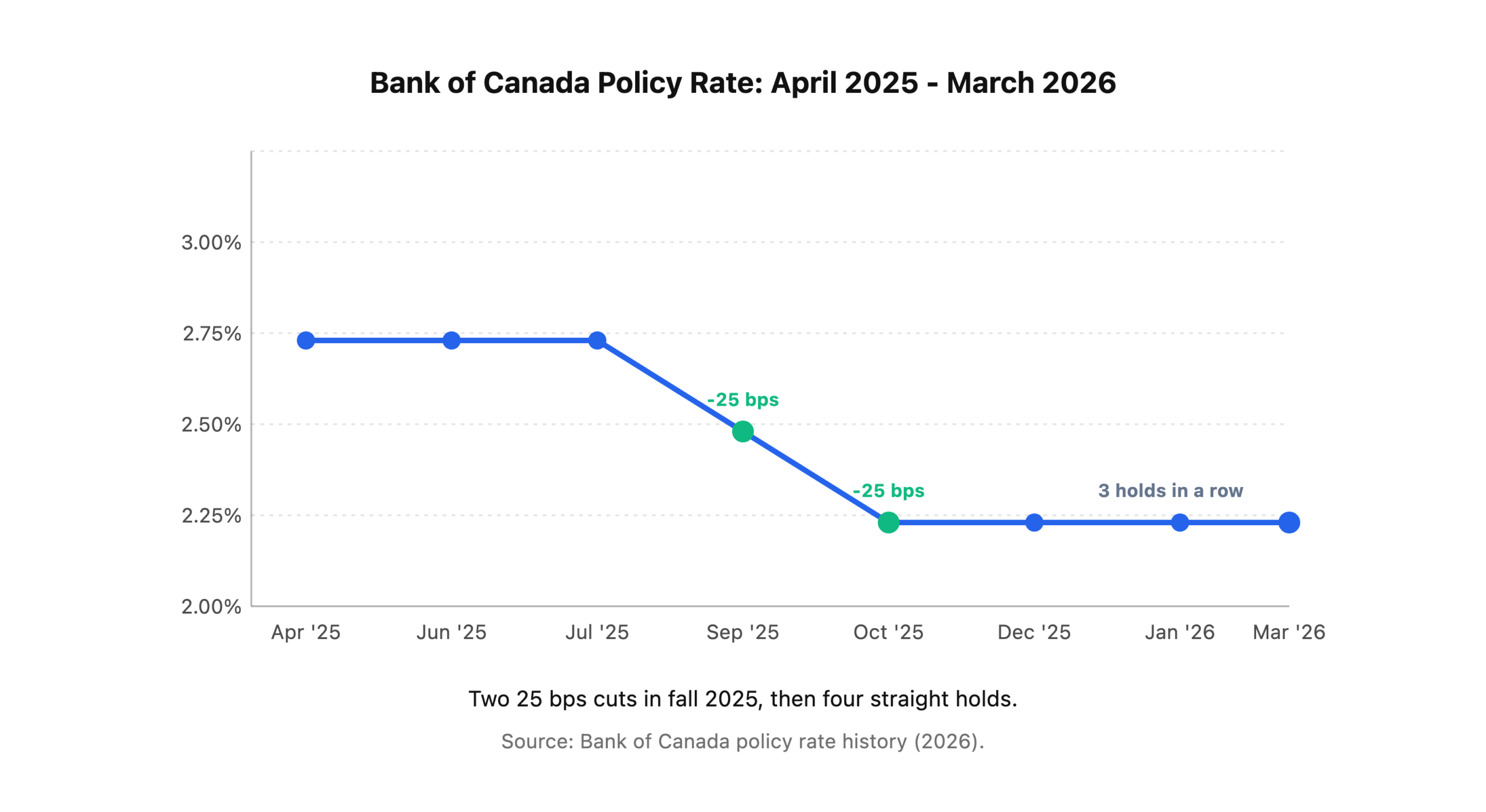

The Bank of Canada held the overnight rate at 2.25% on March 18, 2026 — the third straight hold since the October 2025 cut (Bank of Canada, 2026). For Alberta buyers and anyone staring down a spring renewal, that means no surprise rate relief from the Bank this month, but no new pain either. Here’s exactly where Alberta mortgage rates sit right now, what’s moving them, and what I’m telling Metro clients this week.

Key Takeaways

– Bank of Canada held at 2.25% on March 18, 2026 — third consecutive hold after 75 bps of cuts in fall 2025 (Bank of Canada, 2026).

– Best 5-year fixed insured mortgage rates in Canada sit around 3.75%-3.89%, with the best 5-year variable near 3.30% (WOWA, April 2026).

– The 5-year Government of Canada bond yield closed at 3.06% on April 6 — up 42 bps year-over-year as Middle East oil shocks push long yields higher (Bank of Canada, 2026).

– Alberta’s 2026 GDP forecast was revised up to 2.7% by ATB, outpacing the rest of Canada on oil-driven strength (ATB Financial, March 2026).

What Did the Bank of Canada Do in March?

The Bank of Canada left the overnight rate at 2.25% on March 18 — its fourth consecutive hold in a row and the third since the October 2025 cut (Bank of Canada, 2026). The Bank cited softening growth, weakening labour markets, and Middle East-driven energy shocks as reasons to stay on the sidelines. The next scheduled rate decision lands on April 29, 2026, paired with a fresh Monetary Policy Report.

The bigger picture: the Bank delivered 75 basis points of cuts between September and October 2025, dropping the policy rate from 2.75% down to 2.25%. Since then, four straight holds. Markets are currently pricing in one more possible cut in the second half of 2026, but it’s not guaranteed — and if oil keeps climbing, the next move could just as easily be nothing.

Where Are Alberta Mortgage Rates Right Now?

As of April 7, 2026, the best available 5-year fixed insured mortgage rates in Canada sit around 3.75% to 3.89%, while the best 5-year variable rates hold near 3.30% — making variable roughly 35 to 55 basis points cheaper than fixed for qualified Alberta borrowers (WOWA, April 2026). Prime is still 4.45% at all the Big Six.

Here’s the current snapshot for Alberta borrowers:

| Product | Best Insured | Best Uninsured | Big Bank Posted |

|---|---|---|---|

| 5-year fixed | 3.75%-3.89% | 3.85%-4.04% | ~4.29% |

| 5-year variable | 3.30% | 3.35%-3.40% | Prime -0.45% (~4.00%) |

| Prime rate | 4.45% | 4.45% | 4.45% |

Don’t take the “Big Bank Posted” column at face value. That’s the rate your bank will quote you if you walk in the door unprepared. Every broker relationship in Canada is built on closing the gap between posted and actual — on a $400,000 mortgage, a 0.40% rate difference saves you roughly $7,700 over a 5-year term.

Fixed or Variable in April 2026?

Most Metro clients right now are asking me the same question: with variable 35-55 bps cheaper than fixed, is it finally safe to go variable? My honest take — it depends on your stress test headroom. If you can absorb another 75-100 bps of potential increases without breaking your monthly budget, variable is compelling. If that extra cushion isn’t there, the 3.75% 5-year fixed gives you payment certainty through April 2031, which is worth the 45 bps premium for most first-time buyers.

What’s Actually Driving the Numbers?

Three forces are pulling Canadian mortgage rates in opposite directions right now. Canada’s headline CPI cooled to 1.8% in February — below the Bank’s 2% target for the first time in months (Statistics Canada, 2026). That’s normally a green light for more cuts. But the 5-year GoC bond yield jumped 19 bps in the past month to 3.06% as Middle East oil shocks push long yields higher — and bond yields are what really drive 5-year fixed mortgage pricing.

The tug-of-war:

- Pulling rates down: Cooling inflation (1.8% headline), weak Q4 2025 GDP (-0.6%), national unemployment at 6.7%, US tariff uncertainty

- Pulling rates up: Iran conflict oil shock pushing global energy prices, rising 5-year bond yields, Alberta’s stronger-than-expected economy, base-year inflation effects washing out in March data

The Bank of Canada’s March statement explicitly flagged energy-driven inflation as a near-term upside risk. That’s code for: don’t count on more cuts unless global markets cooperate.

What It Means for Edmonton Buyers and Renewers

Edmonton’s housing market is telling a different story than the national one. Sales jumped 33.1% month-over-month in March 2026 to 2,133 units, and the average price hit $470,819 — up 2.2% year-over-year even as inventory climbed 31.6% YoY (REALTORS Association of Edmonton, April 2026). Translation: more choice for buyers, firmer prices than Ontario or BC, and a negotiating window that’s wider than it’s been in three years.

If You’re Buying Your First Home

Lock in your pre-approval now, at April rates. Even if the Bank of Canada cuts again at the April 29 meeting, bond yields are still elevated — which means 5-year fixed rates may not drop much even if the policy rate does. The rate hold in your pre-approval document is the insurance policy against a surprise move.

If You’re Renewing This Year

Your Big Five bank’s renewal letter will quote you the posted rate (around 4.29%). Every Metro renewal we’ve handled in April has come in 45-80 bps better than that through broker access. On a $300,000 renewal balance, that’s $5,500-$8,000 saved over the next 5 years. Shop before you sign.

If You Have a Variable Already

The rate you’re paying hasn’t moved since October. If you have a fixed-payment variable, your amortization stretched during the 2022-2023 rate shock — and it’s now slowly reverting. Don’t panic-switch to fixed unless your stress test budget can’t handle another 50 bps of uncertainty.

My Take for April 2026

Here’s the thing nobody’s saying out loud: Alberta is outperforming the rest of Canada in a way that matters for mortgage demand. ATB Financial revised Alberta’s 2026 GDP forecast up to 2.7% in late March — versus the roughly 1.6% national forecast (ATB Financial, 2026). Alberta job growth is tracking 3.1% this year. Nominal GDP is running at 6.0% thanks to the energy price tailwind. That’s the backdrop for every mortgage decision in Edmonton and Calgary this year.

What that means in practice: Alberta home prices are likely to stay firmer than Ontario or BC through 2026, buyer demand has more support than national headlines suggest, and the Bank of Canada’s national “hold” stance may actually argue for a slightly more aggressive variable-rate tilt for Alberta borrowers with strong income stability. If you’re in a recession-proof Alberta sector (energy, healthcare, government, education), the variable math looks better than it does for someone in a tariff-exposed Ontario manufacturing town.

The April 29 Bank of Canada decision will either confirm the hold or deliver one more cut. Either way, I’d have your pre-approval signed, your renewal quotes in hand, and your decision framework set before that meeting — not after.

Want a Rate Review Before the April 29 Bank of Canada Decision?

If you’re buying in the next 90 days or your mortgage renews in 2026, the smartest move you can make this week is a free rate review with our team. We’ll pull your best available rates across 30-50+ lenders, run your real stress-tested budget, and lay out fixed vs variable for your specific situation. No pressure, no obligation, no cost. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full breakdown of first-time buyer programs in Alberta, read our complete first-time home buyer Edmonton guide. If you’re weighing your down payment options, check out the FHSA Alberta guide for the tax math that changes everything.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and an Edmonton mortgage broker specializing in first-time buyers, pre-approvals, and rate commentary across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 10, 2026