RRSP Home Buyers’ Plan in Alberta

Withdraw up to $60K from your RRSP tax-free for your first home

The federal government raised the RRSP Home Buyers’ Plan withdrawal limit to $60,000 per person on April 16, 2024 — the biggest increase in program history (Canada Revenue Agency, 2024). For an Alberta couple who both qualify as first-time buyers, that’s $120,000 of tax-free RRSP money available for a down payment — and most Edmonton buyers I work with at Metro still don’t realize how the math actually works.

Here’s exactly how the RRSP HBP works in 2026, including the temporary 5-year repayment grace period that expires at the end of this year, the exact rules for a qualifying withdrawal, and how to stack it with the FHSA for maximum down payment impact.

Key Takeaways

– First-time buyers can withdraw $60,000 per person from their RRSPs tax-free under the HBP (raised from $35,000 on April 16, 2024) (Canada Revenue Agency, 2024).

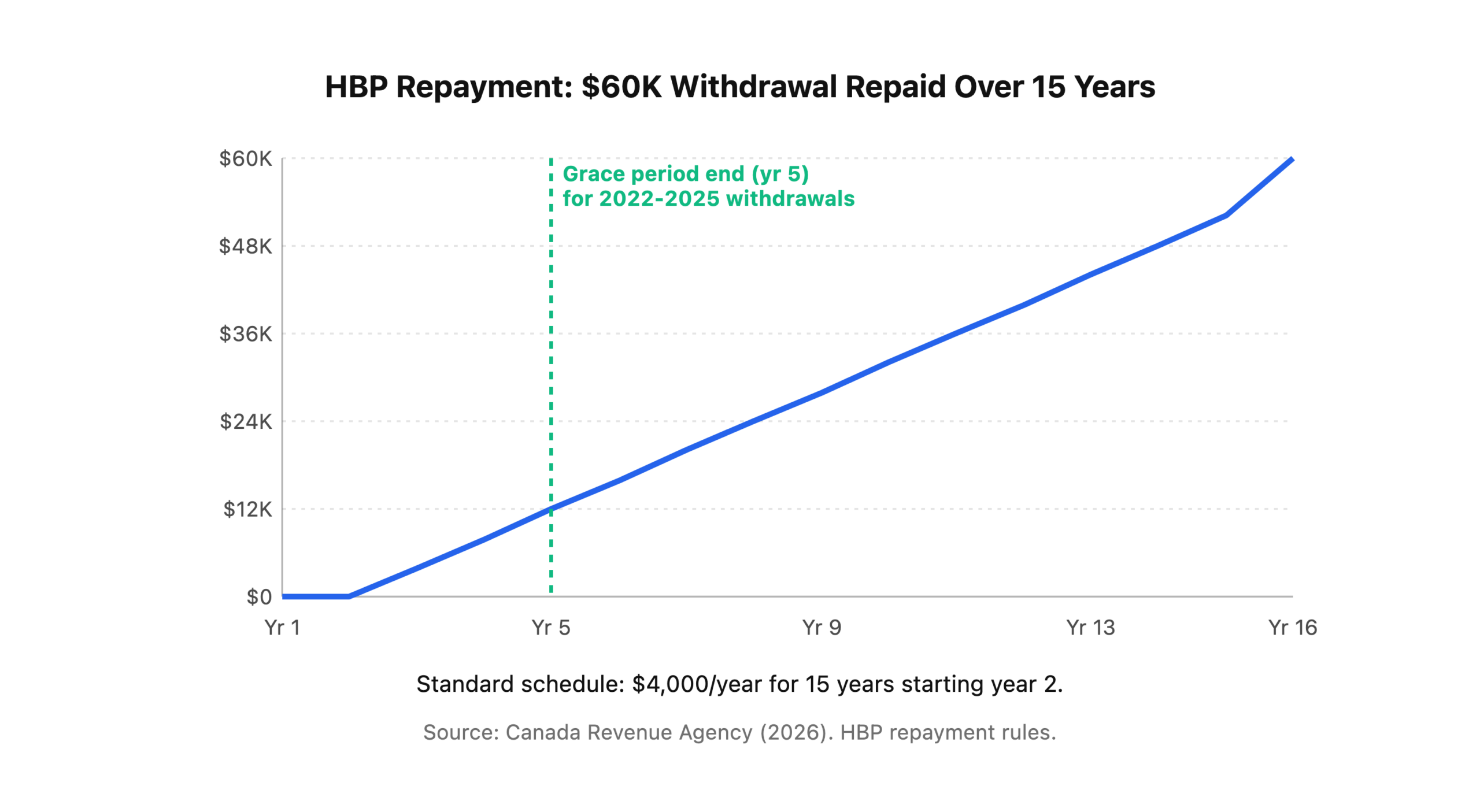

– Withdrawals must be repaid over 15 years starting year 2 after withdrawal — or year 5 under the temporary grace period for withdrawals made between January 1, 2022 and December 31, 2025.

– Stacked with the FHSA, a single Alberta first-time buyer can access $100,000 of tax-advantaged down payment funds; a qualifying couple can access $200,000 (CIBC, 2025).

– Missing a minimum annual HBP repayment triggers that year’s shortfall being added to your taxable income for that year.

What Is the RRSP Home Buyers’ Plan and Who Qualifies?

The RRSP Home Buyers’ Plan (HBP) is a federal program that lets qualifying first-time home buyers withdraw up to $60,000 from their RRSPs tax-free to buy or build a qualifying home — with the condition that the full withdrawal gets repaid back into the RRSP over 15 years (Canada Revenue Agency, 2026). It’s been around since 1992 but the April 2024 limit increase made it dramatically more useful for Alberta buyers.

To qualify as a first-time buyer for HBP purposes, the CRA requires three things:

- You haven’t owned a home you lived in as a principal residence in the current year or any of the previous 4 calendar years

- You’re a Canadian resident from withdrawal through closing

- You have a signed agreement to buy or build a qualifying home with acquisition by October 1 of the year following the withdrawal

The 4-year rule catches a lot of buyers off guard. If you sold your last home in 2020 and have been renting since, you requalify as a first-time buyer for HBP purposes — the clock has reset. This is the same definition used for the FHSA.

What Counts as a “Qualifying Home”?

Any home in Canada that you intend to occupy as your principal residence within one year of buying it. Detached houses, townhouses, condos, mobile homes, and even shares in a co-op housing corporation all qualify. A rental property doesn’t qualify.

How Much Can You Actually Withdraw in 2026?

The federal government raised the HBP withdrawal limit from $35,000 to $60,000 effective April 16, 2024 — the largest single increase in program history, and a direct response to Alberta and Canadian home price appreciation since the previous cap was set in 2019 (Canada Revenue Agency, 2024). The $60,000 limit applies per qualifying individual, so a couple who both qualify as first-time buyers can access up to $120,000 combined.

One important rule: the withdrawal limit is capped by what’s actually in your RRSP. You can’t withdraw $60,000 if your RRSP only has $40,000 in it. And the money must have been in the RRSP for at least 90 days before the withdrawal — last-minute RRSP contributions made immediately before the withdrawal don’t qualify.

Timing Your Withdrawal

The single biggest HBP mistake we see at Metro: buyers who withdraw from the RRSP before they have a signed offer in hand. The CRA requires a written purchase agreement with a closing date before October 1 of the year following your withdrawal, or the withdrawal becomes fully taxable income. On a $60,000 withdrawal, that’s a tax bill of $18,000+ for a typical Alberta earner. Don’t pull the trigger on the withdrawal until your offer is accepted and conditions are close to removal.

How Does RRSP HBP Repayment Work?

You have 15 years to repay the HBP withdrawal back into your RRSP, with repayments starting year 2 after your withdrawal — or year 5 if your withdrawal falls between January 1, 2022 and December 31, 2025 under the temporary grace period (Canada Revenue Agency, 2024). The minimum annual repayment is 1/15th of your withdrawal — so on a maxed $60,000 withdrawal, that’s $4,000/year.

The repayment math is straightforward but easy to mess up:

What Happens If You Miss a Payment?

If you fail to make your minimum annual HBP repayment in a given year, the shortfall is added to your taxable income for that year and taxed at your marginal rate (Canada Revenue Agency, 2026). For an Alberta earner in the 30.5% bracket, missing a $4,000 HBP payment costs about $1,220 in unnecessary tax. And your future repayment schedule doesn’t reset — you still owe the remaining balance.

The practical fix: set up an automatic annual RRSP contribution of at least $4,000/year earmarked as HBP repayment. Most Canadian brokerages let you flag contributions as HBP repayments at tax time.

FHSA or RRSP HBP — Which One Should You Use First?

In almost every case, Alberta first-time buyers should max their FHSA before touching the RRSP HBP — because the FHSA has no repayment obligation, while the HBP forces 15 years of $4,000 annual repayments that compete with your other savings goals (CIBC, 2025). That said, the two programs are fully stackable, and most Alberta buyers we work with end up using both.

The decision framework we use at Metro:

- If your total down payment target is ≤ $40K (FHSA cap) — Use FHSA only. No repayment, no complexity.

- If your target is $40K-$100K — FHSA first ($40K), then HBP for the remainder. Keeps HBP repayments minimal.

- If your target is $100K+ — Max both. $40K FHSA + $60K HBP = $100K per person.

- If you’re buying as a couple — Both partners max both programs. $200K combined access.

The hidden cost of the HBP that most Edmonton buyers miss: the repayment dollars that go back into your RRSP get pulled from your after-tax cash flow, but they don’t generate new RRSP deduction room (you already claimed the deduction when you originally contributed). So a $4,000/year HBP repayment feels like saving, but it’s really just returning borrowed money. On a $60K withdrawal, you’ll lose 15 years of potential RRSP deductions worth roughly $18,000 in taxes for a typical Alberta earner. That’s why we generally recommend exhausting the FHSA first — it gives you the tax deduction AND the tax-free withdrawal, with no repayment trap.

Read our FHSA Alberta guide for the full tax-advantage comparison.

How Do You Actually Make an HBP Withdrawal?

To execute a qualifying RRSP Home Buyers’ Plan withdrawal, you need to complete CRA Form T1036 (Home Buyers’ Plan Request to Withdraw Funds) and submit it to your RRSP issuer — not directly to the CRA (Canada Revenue Agency, 2026). Your bank, credit union, or brokerage processes the withdrawal, withholds no tax (since it’s a qualifying HBP withdrawal), and reports the withdrawal to the CRA on a T4RSP slip at year-end.

The 4-step process:

- Sign your purchase agreement with a closing date before October 1 of the year following withdrawal

- Complete Form T1036 with your RRSP institution, confirming HBP eligibility

- Request the withdrawal — funds are typically available within 3-5 business days

- File Schedule 7 with your tax return the following spring to report the HBP withdrawal and begin tracking your repayment schedule

Most Alberta banks can process an HBP withdrawal in one branch visit if you have the purchase agreement and completed Form T1036 in hand. Online brokerages may take 1-2 weeks, so don’t leave it to the last minute.

Frequently Asked Questions

Can I use the HBP and FHSA for the same home purchase?

Yes — they’re fully stackable. A single Alberta first-time buyer can combine up to $100,000 in tax-advantaged down payment funds ($40K FHSA + $60K HBP), and a qualifying couple can access $200,000 (Canada Revenue Agency, 2026). This is now the recommended strategy for most Edmonton first-time buyers with meaningful existing RRSP savings.

What if my spouse isn’t a first-time buyer?

Your spouse’s past home ownership disqualifies them from using the HBP, but doesn’t disqualify you as long as you yourself haven’t owned a home you lived in during the current year or previous 4 calendar years (Canada Revenue Agency, 2026). You can still withdraw your $60,000 — just not your spouse’s $60,000.

Does my RRSP need to be in a specific kind of account?

Only RRSPs qualify — not TFSAs, RRIFs, or locked-in retirement accounts (LIRAs). Funds must have been in the RRSP for at least 90 days before the withdrawal (Canada Revenue Agency, 2026). Spousal RRSPs count, but withdrawals count against the annuitant’s own HBP limit, not the contributor’s.

What if I can’t repay the HBP on schedule?

Any minimum annual repayment you miss gets added to your taxable income that year at your marginal tax rate (Canada Revenue Agency, 2026). For an Alberta earner at 30.5% marginal rate, missing a $4,000 payment costs $1,220 in unnecessary tax. Your repayment schedule doesn’t reset — you still owe the balance in future years.

Is the 5-year grace period the same as a repayment holiday?

Almost. For HBP withdrawals made between January 1, 2022 and December 31, 2025, repayment starts in year 5 instead of year 2 — a 3-year deferral. This gives buyers who withdrew during the peak-rate years extra breathing room, but the total 15-year repayment window still applies from the deferred start date (Canada Revenue Agency, 2024).

Ready to Build Your RRSP + FHSA Down Payment Plan?

The right combination of FHSA, RRSP HBP, and regular savings depends on your income, existing RRSP balance, timeline to purchase, and risk tolerance. Metro’s first-time buyer team builds these plans for Edmonton and Calgary buyers every week — free, no pressure, no obligation. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full down payment math with Alberta-specific examples, read our down payment Alberta complete guide. If you haven’t opened an FHSA yet, read the FHSA Alberta walkthrough — it should be your first move.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 15, 2026