Mortgage Broker Edmonton

Edmonton’s median home price sits at $432,250 in 2026 — local broker insights for every neighborhood

Edmonton is one of the fastest-growing major Canadian metros — a 3% population surge that pushed the city past 1.23 million people (Statistics Canada, 2025). That kind of growth creates opportunity, but it also means more competition for homes, tighter timelines, and real money on the line if you pick the wrong lender. As a mortgage broker in Edmonton with 229 five-star Google reviews and access to 30+ lenders, Metro Mortgage Group exists to make sure you don’t.

Key Takeaways

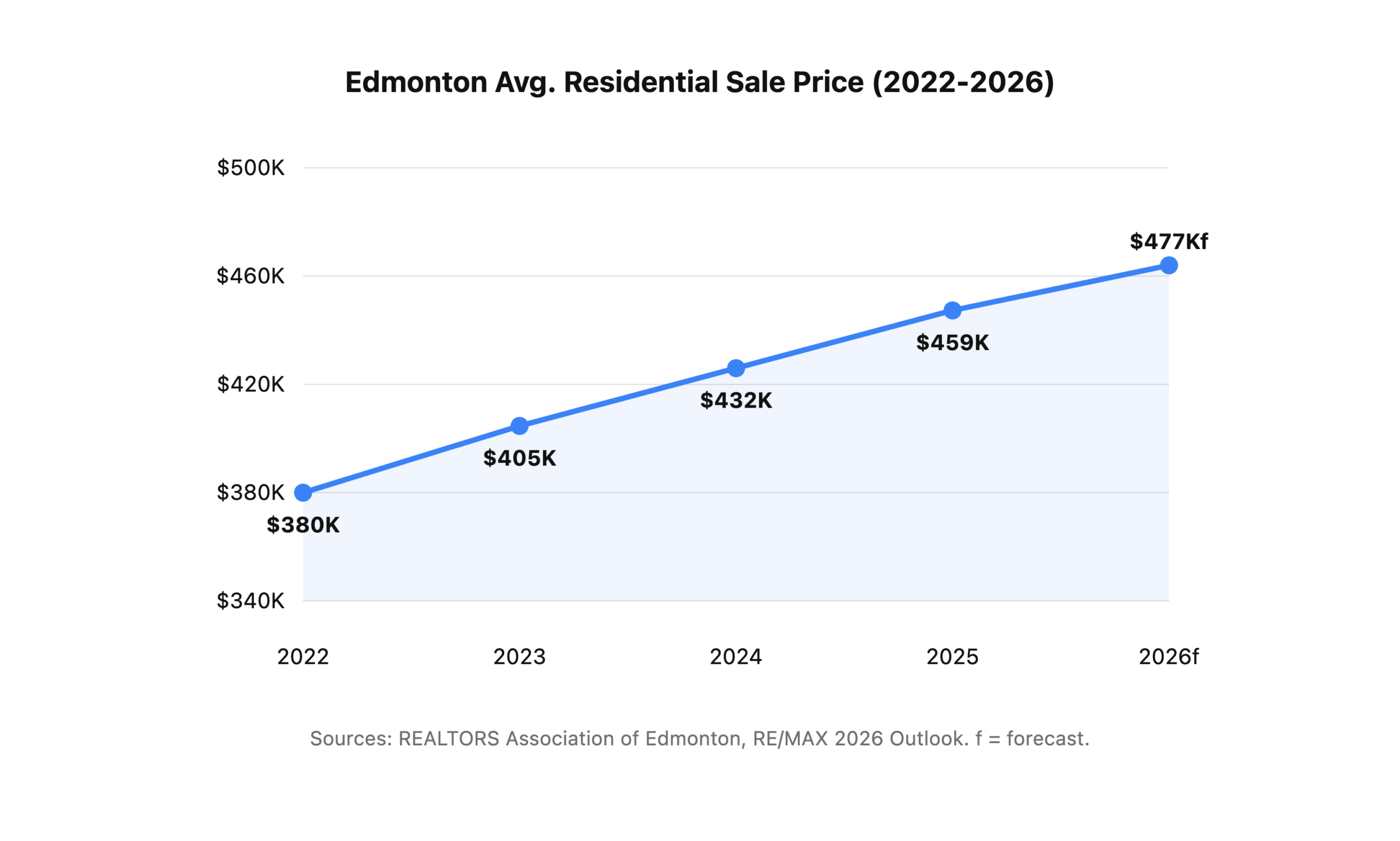

– Edmonton’s median residential sale price hit $432,250 in February 2026, with single-family detached homes at $517,500 (REALTORS Association of Edmonton, 2026).

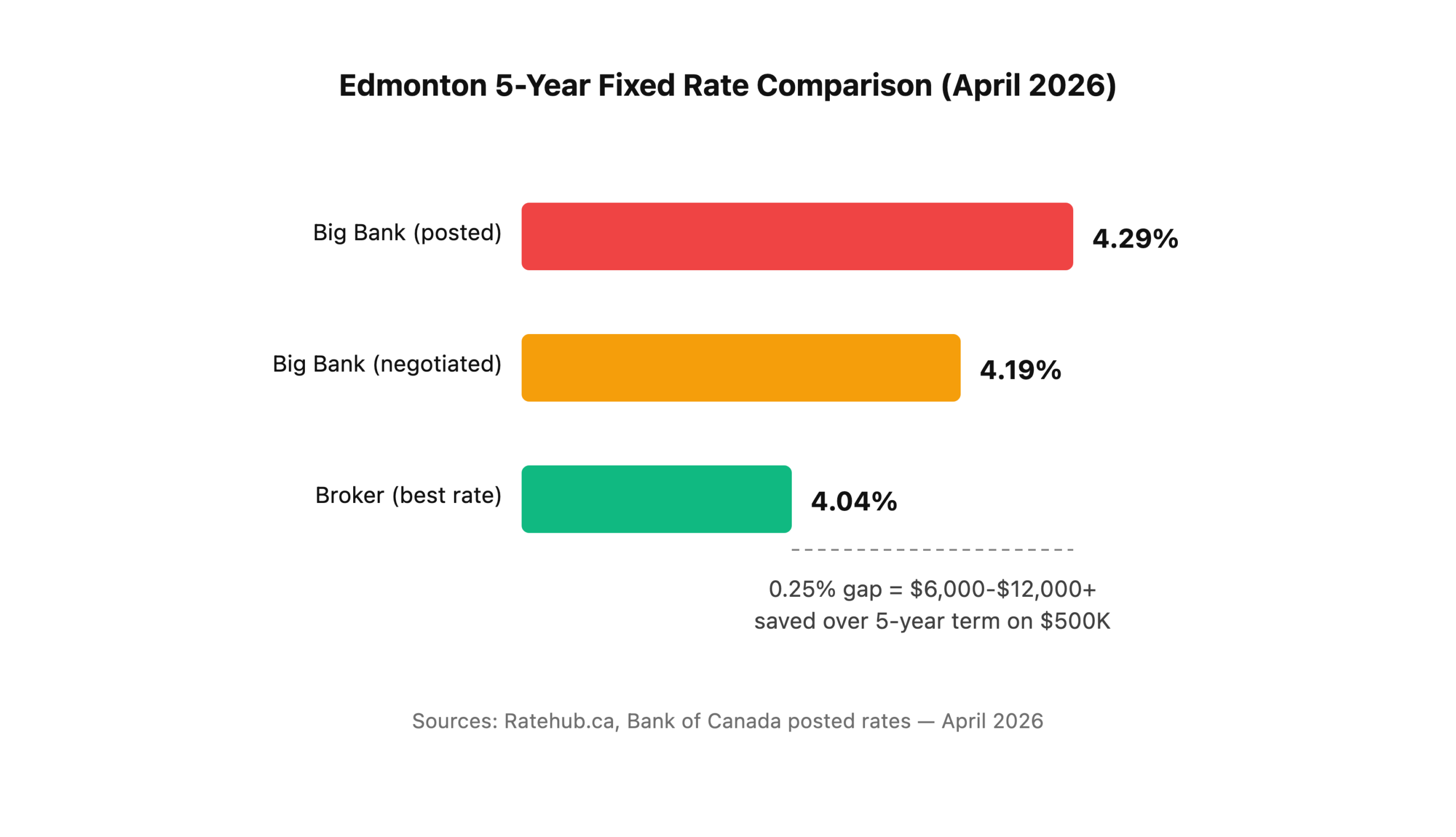

– A mortgage broker typically saves Edmonton buyers 0.25-0.50% compared to posted bank rates — that’s $6,000-$12,000+ on a $500,000 mortgage over a 5-year term (Ratehub.ca, 2026).

– Metro Mortgage Group carries a 5.0-star rating across 229 Google reviews with a 7-broker team and access to 30+ lenders including B-lenders and private capital.

– The Bank of Canada policy rate sits at 2.25%, with 5-year fixed rates starting around 4.04% through brokers vs. 4.29%+ at big banks (Bank of Canada, 2026).

Edmonton’s Housing Market: What Buyers and Homeowners Need to Know in 2026

Edmonton is a balanced market heading into mid-2026, with the median residential sale price sitting at $432,250 — a modest 0.6% dip year-over-year that still leaves prices well above 2023 levels (WOWA.ca, 2026). That balance creates a window where neither buyers nor sellers hold all the cards, and your financing terms matter more than ever.

The numbers tell a clear story. Single-family detached homes carry a median price of $517,500. Semi-detached properties sit at $431,650 (up 1.5% annually). Townhouses have jumped 4.4% to $318,400. Condos, meanwhile, have softened to $191,200, creating an entry point for first-time buyers willing to start with an apartment (REALTORS Association of Edmonton, 2026).

What’s driving all of this? Population. Edmonton was among the fastest-growing major Canadian metros between 2024 and 2025, with strong international migration (Edmonton Global, 2025). CMHC recorded 16,426 housing starts in 2025, a 22% gain, though starts are forecast to pull back 11% in 2026 as supply catches up (CMHC, 2026).

Citation Capsule: Edmonton was among Canada’s fastest-growing census metropolitan areas in 2025, adding a 3% population increase driven by international migration and strong interprovincial migration. — Statistics Canada, 2025

So what does that mean for your mortgage? It means inventory is rising (5,462 active listings in February 2026), competition is stabilizing, and the difference between a good rate and a great rate can save you tens of thousands of dollars. That’s exactly where a mortgage broker earns their keep.

First-time buyer? See our complete first-time home buyer guide.

What Does a Mortgage Broker in Edmonton Actually Do?

A mortgage broker shops your file across 30+ lenders — banks, credit unions, monoline lenders, B-lenders, and private capital pools — to find the best rate and terms for your specific situation. You pay nothing for this service; lenders compensate the broker directly. The result: better rates, broader options, and somebody in your corner who isn’t tied to a single institution.

Here’s what Metro Mortgage Group handles for Edmonton clients:

- Purchase financing — first-time, move-up, investment, and luxury

- Refinancing — pulling equity, consolidating debt, or improving your rate

- Renewals — your existing lender’s renewal letter is almost never the best offer

- Pre-approvals — rate holds that protect you while you shop

- Construction and renovation mortgages — Nelson’s 9+ years in construction means he understands draw schedules and builder timelines firsthand

- Commercial and multi-family financing — small-to-mid-size projects across Edmonton

- Self-employed and non-traditional income — BFS (business-for-self) programs through B-lenders and alternative channels

Why would you limit yourself to one bank’s menu when a broker comparison costs you nothing?

Need commercial or construction financing? See our commercial mortgages guide.

Why a Broker Beats the Bank: Edmonton Rate Comparison

Edmonton borrowers who use a mortgage broker save an average of 0.25-0.50% on their interest rate compared to posted big-bank rates (Ratehub.ca, 2026). On a $500,000 mortgage amortized over 25 years, that translates to $6,000-$12,000+ in interest savings over a single 5-year term. Over the life of the mortgage, the gap compounds.

But rate isn’t the whole story. A broker also negotiates on prepayment privileges, portability, penalty calculations (IRD vs. three-month interest), and blend-and-extend options at renewal. These terms don’t show up in rate comparison tables, but they can cost or save you thousands if your plans change mid-term.

Citation Capsule: The lowest available 5-year fixed mortgage rate in Canada sits at 4.04% through broker channels as of April 2026, compared to 4.29% posted at major chartered banks — a spread that saves borrowers $6,000-$12,000+ per $500,000 over five years. — Ratehub.ca, 2026

Not sure what you can afford? Try our mortgage calculator or see how much mortgage you can afford.

Meet the Metro Mortgage Group Team

Metro Mortgage Group was founded in 2011 and has spent 15+ years building relationships with lenders that a single bank branch simply can’t replicate. Our 7-broker team holds a collective 5.0-star rating across 229 Google reviews — a track record that speaks louder than any marketing claim.

Nelson Sousa (Co-Owner) — 9+ years in the construction industry before moving into mortgage brokering. That background means Nelson understands construction draws, builder delays, and renovation budgets at a technical level most brokers don’t.

Daniel De Sousa (Co-Owner) — Manages commercial, multi-family, and complex residential files. Daniel’s lender relationships span A-banks, credit unions, MICs, and private pools.

Ariell Laszchuk — Specializes in first-time buyer programs and government incentives including the FHSA and RRSP Home Buyers’ Plan.

Nathan Danzo — Focused on refinance strategy and debt consolidation across the Edmonton metro.

Miguel Cunha — Handles purchase and renewal files with a focus on Edmonton’s south-side communities.

Colin Topolnitsky — Works with self-employed borrowers and non-traditional income documentation.

Sandra Forscutt — Experienced across all residential categories with deep lender product knowledge.

Every broker on the team is licensed through the Real Estate Council of Alberta (RECA) and operates under Alberta’s mortgage brokerage regulations. Your file is handled by a licenced professional, not a call centre.

Edmonton Neighbourhoods We Serve

Edmonton is a city of distinct communities, each with its own price range, housing stock, and buyer profile. Metro Mortgage Group serves every corner of the metro, but here’s where we see the most activity:

West Edmonton

From the established streets near West Edmonton Mall to newer developments in Lewis Estates, Rosenthal, and Secord, west-side buyers tend toward single-family homes in the $450,000-$600,000 range. Strong school catchments and proximity to the Whitemud Freeway make this corridor popular with young families.

South Edmonton & Windermere

South Edmonton — including Windermere, Keswick, Summerside, and the Heritage Valley area — is the city’s fastest-growing residential zone. New construction dominates, and Nelson’s construction background is especially valuable here for clients building custom or semi-custom homes.

Downtown & Oliver

The condo market centred around Jasper Avenue and the Ice District has softened, with median condo prices at $191,200 (REALTORS Association of Edmonton, 2026). That creates opportunity for first-time buyers and investors.

North Edmonton & Castle Downs

Mature neighbourhoods like Castle Downs, Lake District, and the newer Cy Becker and Crystallina Nera communities offer some of Edmonton’s best value in single-family homes. Semi-detached and townhouse options sit well below the city-wide median.

St. Albert, Sherwood Park & Surrounding Communities

The broader Edmonton metro — St. Albert, Sherwood Park, Spruce Grove, Stony Plain, Leduc, Beaumont, and Fort Saskatchewan — all fall within our service area. Each satellite community has its own pricing dynamics, and lender appetite can vary by postal code.

Have a property outside these areas? We fund deals across all of Alberta.

The Edmonton Market in Context: Why Timing and Terms Matter Now

Edmonton’s average residential price rose 6.3% in 2025, climbing from $431,994 to $459,179 (WOWA.ca, 2026). RE/MAX forecasts another 4% gain in 2026, which would push the average past $477,000 (RE/MAX, 2026).

Meanwhile, the Bank of Canada holds its policy rate at 2.25%, and fixed rates are no longer expected to drop further in 2026 due to bond market volatility and global trade uncertainty (Bank of Canada, 2026). Variable rates remain stable around 3.35%.

What does this mean practically? If you’re buying, refinancing, or coming up for renewal in Edmonton this year, the rate you lock in today is likely as good as it gets for a while. And whether that rate is 4.04% or 4.29% depends entirely on whether you’re working with a broker or walking into your bank branch.

Citation Capsule: Edmonton home prices rose 6.3% in 2025, and RE/MAX forecasts an additional 4% gain in 2026 as the city’s population growth sustains demand in a market that remains more affordable than Toronto, Vancouver, or even Calgary. — RE/MAX Canada, 2026

See our current rate benchmarks for where things stand today.

How the Metro Mortgage Process Works

Getting pre-approved or funded through Metro follows a straightforward process. Here’s what to expect:

Step 1: Free Consultation (15-30 minutes)

Call us at 780-974-1270 or email info@MetroMortgageGroup.ca. We’ll discuss your goals, timeline, income situation, and any concerns. No obligation, no pressure.

Step 2: Document Collection

We’ll send you a checklist. For most employed borrowers, that’s T4s, pay stubs, a credit authorization, and a government-issued ID. Self-employed? We’ll outline BFS program requirements tailored to your income type.

Step 3: Lender Shopping

This is where the broker advantage kicks in. We submit your file to the lenders best suited to your profile — not just one bank, but as many as needed to get the best rate and terms. You sit back; we do the legwork.

Step 4: Approval & Conditions

Once approved, we walk you through the commitment letter, explain every condition, and coordinate with your realtor and lawyer to keep the deal on track.

Step 5: Funding

Your mortgage funds on closing day. We stay available after closing for questions about your first payment, property tax setup, or anything else that comes up.

The entire process, from first call to funding, typically takes 3-5 weeks for a standard residential purchase. Refinances and renewals often close faster.

Planning your budget? See our closing costs Alberta guide and our credit score and mortgage guide.

Frequently Asked Questions

How much does it cost to use a mortgage broker in Edmonton?

Nothing. Mortgage brokers in Alberta are compensated by the lender when your deal funds, not by you. Metro Mortgage Group never charges borrower fees on standard residential transactions. You get access to 30+ lenders and competitive rate shopping at zero out-of-pocket cost — a service model regulated by RECA.

What credit score do I need to qualify for a mortgage in Edmonton?

CMHC-insured mortgages require a minimum credit score of 600 for at least one borrower (CMHC, 2025). Most A-lenders prefer to see scores above 680 for their best rates. Metro also works with B-lenders and alternative channels that approve borrowers with scores as low as 500-550. The terms will differ, but options exist.

Are mortgage rates in Edmonton different from the rest of Alberta?

Rates themselves are set nationally by most lenders, so Edmonton and Calgary typically see the same pricing. However, property values, rental market strength, and neighbourhood risk profiles can affect approval terms, especially for investment and commercial properties. A local Edmonton broker understands these nuances.

Should I get pre-approved before house hunting?

Absolutely. A pre-approval locks in your rate (typically for 90-120 days), tells you exactly what you can afford, and signals to sellers that you’re a qualified buyer. In Edmonton’s balanced market, a pre-approval letter can be the difference between a smooth offer and a missed property.

How are Metro’s 229 reviews verified?

Every review sits on Google Business Profile and is tied to a verified Google account. We don’t incentivize reviews or use review-gating software. Our 5.0-star average across 229 reviews reflects 15+ years of client outcomes across first-time buyers, investors, commercial borrowers, and renewal clients.

Ready to Talk? Here’s How to Reach Us

Metro Mortgage Group Inc.

10706 120 St NW #200, Edmonton, AB T5H 0W7

- Phone: 780-974-1270

- Email: info@MetroMortgageGroup.ca

- Google Reviews: 5.0 stars / 229 reviews

Whether you’re buying your first home, refinancing to pull equity, renewing a term, or financing a multi-family project, we’d like to hear from you. The consultation is free, the rate shopping is free, and you’ll know within 24 hours where you stand.

First-time buyer? See our FHSA guide and our down payment Alberta guide.

About the Author: Nelson Sousa is co-owner of Metro Mortgage Group Inc. and a licenced mortgage broker in Edmonton, Alberta. With 9+ years in the construction industry and over a decade in mortgage brokering, Nelson specializes in residential purchase, construction, and renovation financing across the Edmonton metro. Reach him directly at info@MetroMortgageGroup.ca.

Last updated: May 5, 2026