First-Time Home Buyer in Edmonton: The Complete 2026 Guide

By Metro Mortgage Group · Updated April 2026 · 35 min read

Video transcript

If you’re trying to buy your first home in Edmonton, you’ve probably heard a hundred confusing things about down payments, rates, and the stress test.

I’m Daniel De Sousa, co-owner of Metro Mortgage Group. In under three minutes, I’ll walk you through exactly what it takes — no jargon, just the numbers that matter.

First — how much do you really need? In Canada the minimum down payment is 5% on the first $500,000 of the price, and 10% on anything above that. On a typical Edmonton home around $455,000, that’s roughly $22,750 to get in the door.

Put down less than 20% and you’ll add mortgage default insurance — but here’s the part people miss: that insurance actually unlocks some of the lowest rates available.

Next, use the tax-free help built for first-time buyers. The First Home Savings Account lets you save up to $8,000 a year — $40,000 total — deductible going in, and tax-free coming out. Stack it with the RRSP Home Buyers’ Plan, where you can pull up to $60,000, and a couple can put over $100,000 toward a down payment. There’s also a $1,500 federal tax credit just for buying your first home.

Before you shop, get pre-approved — a lender confirms what you qualify for and locks a rate for up to 120 days. But watch the stress test: you have to prove you could afford your mortgage at your contract rate plus 2%, or 5.25% — whichever is higher. That’s why the rate you qualify at isn’t the rate you pay. We run that math for you, usually within 24 hours.

Then there’s closing — legal fees, a home inspection, title insurance, prepaid property taxes — usually 1.5 to 4% of the price. The good news for us? Alberta has no land transfer tax. On the same purchase that saves you thousands versus Ontario or British Columbia.

The biggest mistake I see? Walking into your own bank and taking the first rate offered. A bank quotes from one rate sheet. As brokers, we shop your file across 30-plus lenders so they compete for you — and it costs you nothing, because the lender pays us.

Buying your first home in Edmonton doesn’t have to be overwhelming — you just need someone who does this every day in your corner. When you’re ready, book a free, no-pressure pre-approval chat with Metro. Let’s get you home.

Edmonton just became one of the most approachable major housing markets in Canada for first-time buyers. The benchmark price sits at $426,000 as of March 2026 (REALTORS Association of Edmonton, 2026) — less than half of what the same money buys in Toronto or Vancouver. Add Alberta’s zero land transfer tax and the federal mortgage reforms that took effect December 15, 2024, and 2026 might be the best year yet for a first home in this city.

This guide walks you through every rule, number, and decision point. No fluff. Just what a first-time buyer needs to know before getting pre-approved, shopping, and closing on a home in Edmonton.

Key Takeaways

– Edmonton’s average residential price hit $470,819 in March 2026 — still roughly half the cost of Toronto or Vancouver (REALTORS Association of Edmonton, 2026).

– The federal insured mortgage cap rose to $1.5 million on December 15, 2024, unlocking 5%-down financing on homes that used to require 20% (Department of Finance Canada, 2024).

– First-time buyers can now withdraw $60,000 from an RRSP under the Home Buyers’ Plan — plus another $40,000 lifetime through the FHSA (Canada Revenue Agency, 2024).

– Alberta charges no land transfer tax. Closing on a $470K Edmonton home costs about $970 in registration fees versus $12,950 on the same home in Toronto (Government of Alberta, 2024).

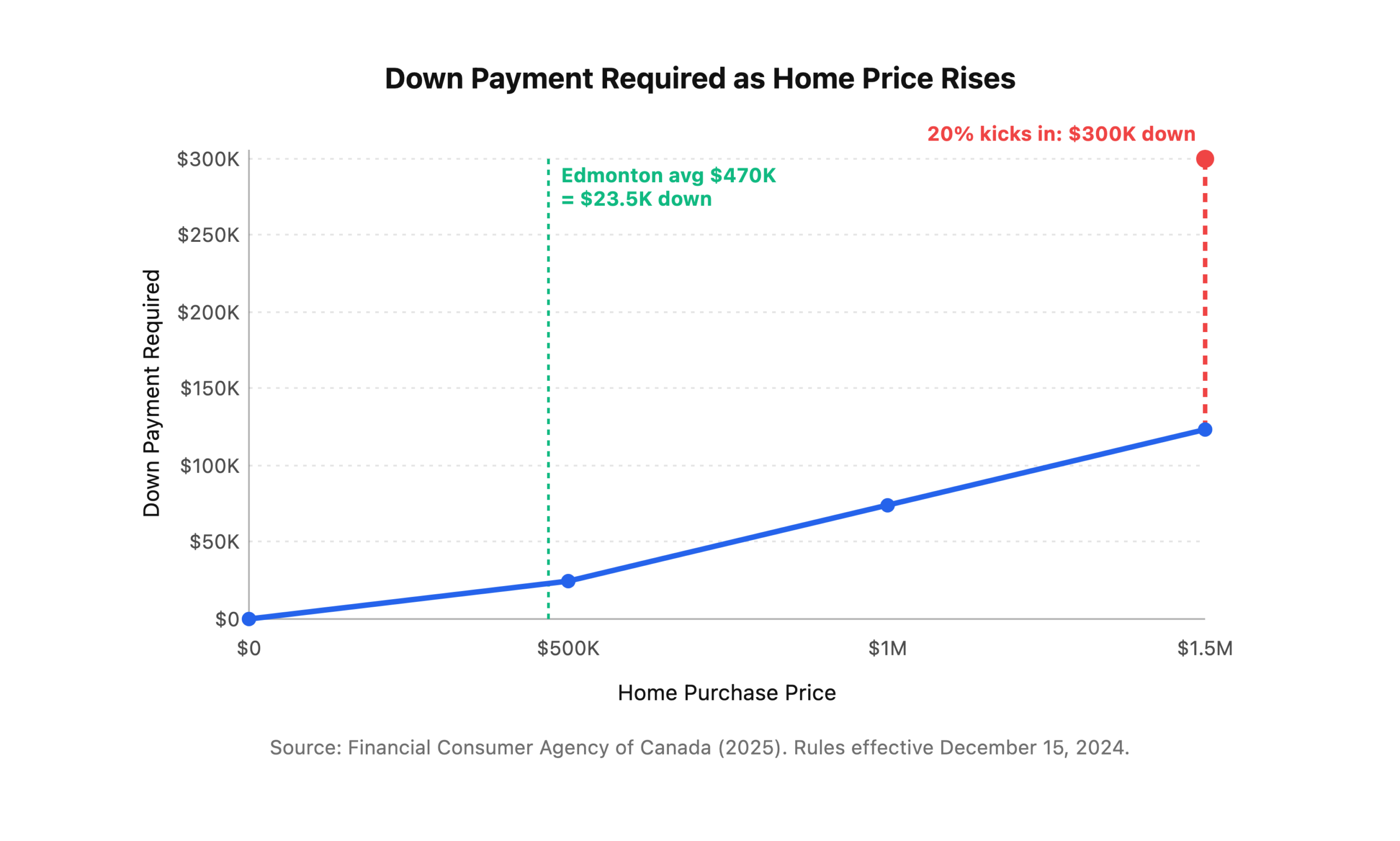

How Much Do You Actually Need to Buy a Home in Edmonton in 2026?

On a $470,000 Edmonton home — the city’s March 2026 average — you need $23,500 in down payment plus roughly $3,500-$5,500 in closing costs to get the keys (REALTORS Association of Edmonton, 2026). That’s under $30,000 total cash-to-close. A buyer in Vancouver needs that much just for their Property Transfer Tax.

Canada’s minimum down payment rules scale with the purchase price. Since December 15, 2024, the tiers look like this (Financial Consumer Agency of Canada, 2025):

- Homes under $500,000 — 5% of the purchase price

- Homes $500,000 to $1,500,000 — 5% on the first $500K, 10% on the portion above

- Homes over $1,500,000 — 20% minimum (no default insurance available)

The sweet spot for Edmonton is obvious once you see the math. The entire detached segment averaged $590,162 in March 2026 (REALTORS Association of Edmonton, 2026), which fits squarely in Tier 2 — meaning about $34,000 in down payment buys you an average Edmonton detached house. That’s a number most dual-income Edmonton households can hit in 18-24 months of focused saving, especially if you’re stacking the FHSA and RRSP HBP.

Here’s what trips most first-time buyers up. They assume they need 20% down to buy at all. They don’t. The 20% threshold only matters if you want to avoid paying mortgage default insurance. Below 20%, you pay a CMHC premium (between 2.80% and 4.00% of your loan), but you can roll that premium into your mortgage balance rather than paying it upfront (CMHC, 2025). For most Edmonton first-time buyers, the tradeoff is worth it — you get into the market three to five years sooner.

Need the full walk-through with dollar-by-dollar examples? See our complete breakdown of down payment requirements in Alberta.

What Government Programs Help Alberta First-Time Buyers in 2026?

First-time Alberta buyers have access to three major tax-advantaged programs worth a combined $100,000+ in tax-sheltered savings capacity per person: the First Home Savings Account ($40,000 lifetime), the RRSP Home Buyers’ Plan ($60,000), and the GST New Housing Rebate (Canada Revenue Agency, 2026). A couple who both qualify as first-time buyers can stack up to $200,000 of tax-free savings toward their first home.

FHSA: The Best Account Most People Still Don’t Understand

The First Home Savings Account launched April 1, 2023, and it’s become the most powerful tool in the first-time buyer toolkit. You can contribute up to $8,000 per year to a $40,000 lifetime maximum (Canada Revenue Agency, 2026). Contributions are tax-deductible going in (like an RRSP), but qualifying withdrawals come out tax-free (like a TFSA). It’s the only Canadian account that lets you deduct on the way in and pull the money out tax-free.

One quirk worth knowing. If you don’t max out the $8,000 in a year, unused room carries forward — but only after you’ve opened the account. If you’re planning to buy in 2027 or 2028, opening an FHSA today (even with a $0 deposit) starts the clock on your carry-forward room. That’s a free move nearly every pre-buyer in Edmonton should make today.

RRSP Home Buyers’ Plan: Now $60,000 Per Person

The federal government raised the RRSP Home Buyers’ Plan withdrawal limit from $35,000 to $60,000 effective April 16, 2024 (Canada Revenue Agency, 2024). A couple who both qualify as first-time buyers can pull $120,000 out of their RRSPs tax-free toward a home purchase. Repayment happens over 15 years, with installments normally starting in year two.

There’s one timing detail worth flagging. If you made your HBP withdrawal between January 1, 2022 and December 31, 2025, repayment doesn’t start until year five instead of year two — a three-year grace period the CRA added to help buyers who drained their RRSPs during the peak-rate years. That means a 2024 withdrawal doesn’t start its repayment schedule until 2029.

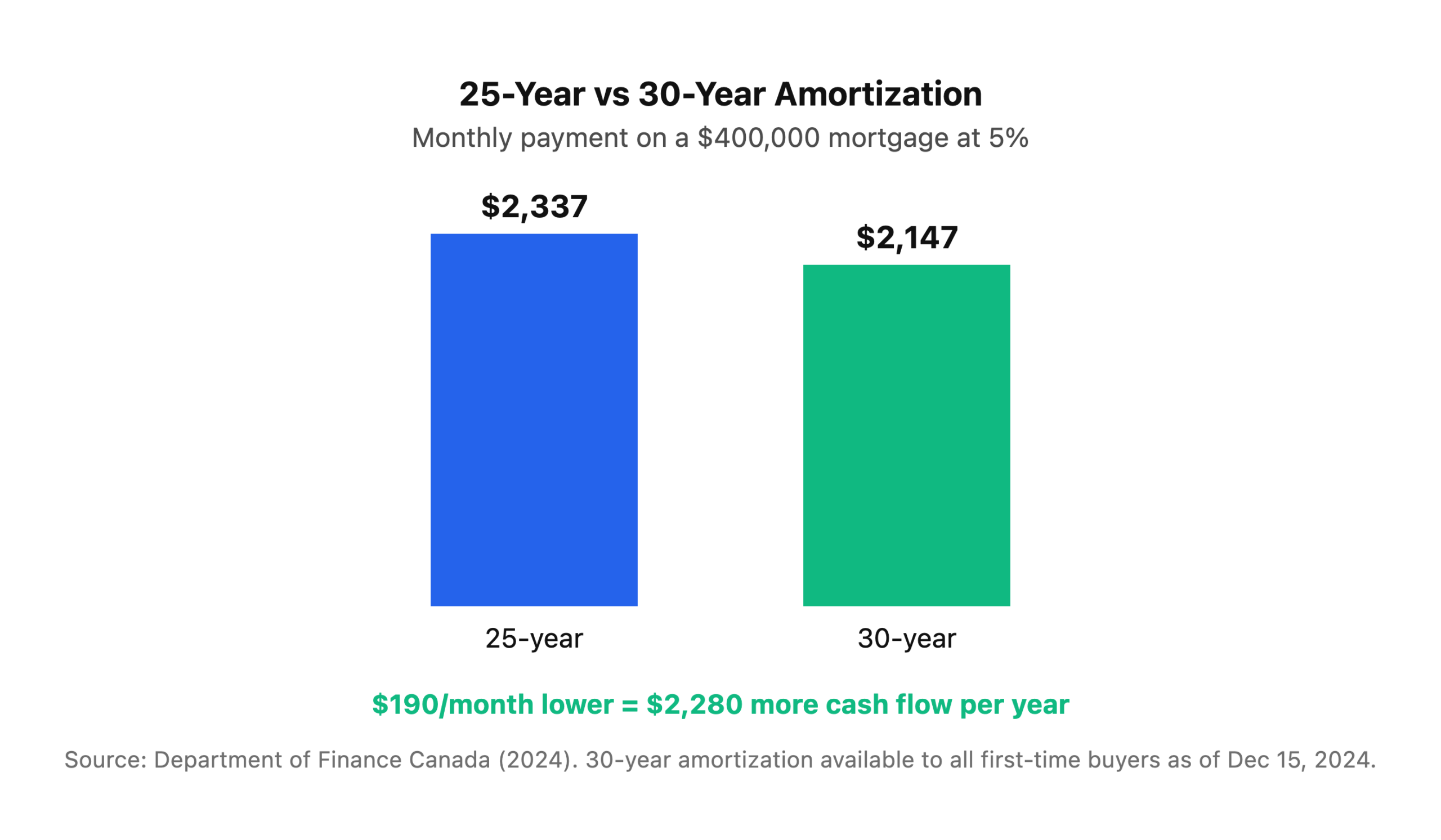

30-Year Amortizations Are Back for First-Time Buyers

Since December 15, 2024, all first-time buyers and all buyers of newly constructed homes can now access 30-year insured mortgage amortizations (Department of Finance Canada, 2024). On a $400,000 mortgage at 5%, stretching from 25 to 30 years drops your monthly payment by about $190. That’s real cash flow for a first-time buyer still furnishing an empty living room.

Our take: The 30-year amortization is a real gift for cash flow, but treat it as a tool, not free money. You will pay more in lifetime interest. Imagine a first-time buyer who uses the 30-year to ease into ownership, then prepays aggressively in years 3-5 once career income catches up. Many lenders allow 15-20% annual prepayment without penalty.

Want the deeper dive on each program? Read our FHSA Alberta complete guide and the RRSP Home Buyers Plan walkthrough for Alberta buyers.

How Do Mortgage Pre-Approval and the Stress Test Actually Work?

Every federally-regulated Canadian lender must qualify you at the greater of your contract mortgage rate plus 2% or a 5.25% floor — that’s the federal stress test (Office of the Superintendent of Financial Institutions, 2026). If your actual 5-year fixed offer is 4.79%, you’ll be qualified at 6.79% on paper, even though you only pay 4.79% in real life. The stress test doesn’t change what you pay — it changes how much the lender will lend you.

Here’s why it matters for Edmonton buyers. On a $90,000 combined household income, the stress test typically caps mortgage eligibility around $380,000-$410,000 depending on other debts. That’s enough for a starter condo or townhouse in most Edmonton neighborhoods, but tight on a detached home. Knowing your real stress-tested ceiling before you shop saves weeks of heartbreak.

Credit score minimums are less scary than most buyers fear. CMHC requires just 600 for at least one borrower on an insured mortgage (CMHC, 2025). Most big-bank lenders want to see 680+ for their best rates, but a broker with B-lender access (like us) can often place a 600-660 borrower on competitive terms.

Pre-approvals hold your rate for 90 to 120 days at most Canadian lenders. That’s your shopping window. If you haven’t found a home in that time, you re-submit and re-qualify — and if rates have moved, your borrowing ceiling moves with them. Want to know what documents you actually need? The list is short:

- Two years of T4s or a Notice of Assessment (NOA) — whichever shows stable income

- 30-90 days of recent pay stubs

- 90 days of bank statements showing your down payment savings

- Photo ID (driver’s license plus one secondary)

- Self-employed buyers add 2 years of business financials + CRA Statement of Account

For the full document list and a step-by-step pre-approval flow, see our Edmonton pre-approval checklist. For the math behind OSFI’s qualifying rule, read the stress test explained for 2026.

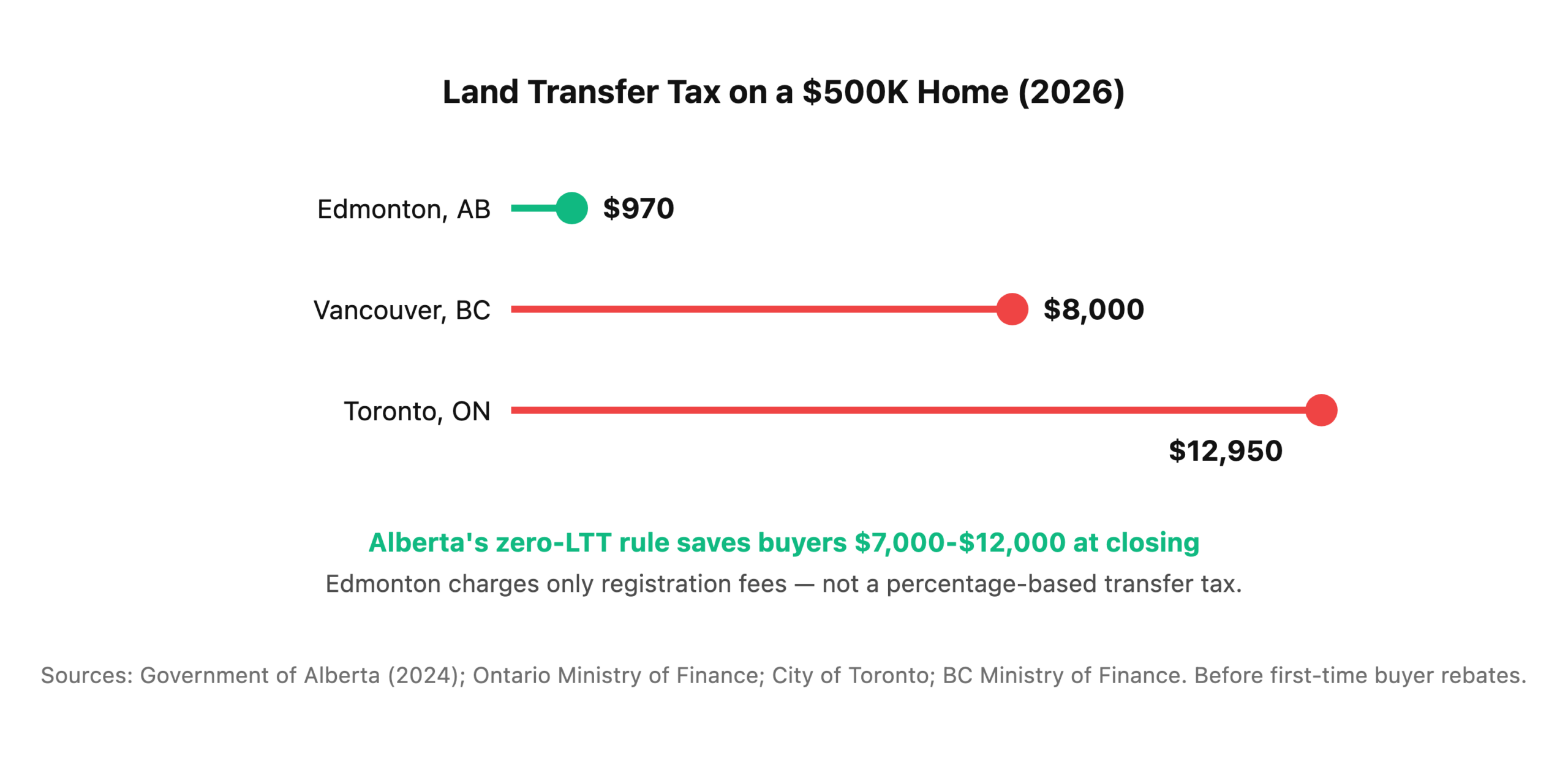

What Does It Actually Cost to Close a Home in Alberta?

Alberta is one of only two Canadian provinces with no land transfer tax. Closing on a $500,000 Edmonton home costs about $970 in Land Titles Office registration fees — not the $12,950 an Ontario buyer pays on the same home in Toronto (Government of Alberta, 2024). That single rule saves Alberta first-time buyers the equivalent of a used car at the closing table.

Here’s how Alberta’s registration fees actually break down as of the October 20, 2024 update:

- Title transfer — $50 base + $5 per $5,000 of purchase price

- Mortgage registration — $50 base + $5 per $5,000 of mortgage principal

Run the math on a $500,000 home with a $475,000 mortgage:

- Title transfer = $50 + ($500,000 ÷ $5,000 × $5) = $550

- Mortgage registration = $50 + ($475,000 ÷ $5,000 × $5) = $525

- Total LTO fees = about $1,075

For an Edmonton buyer used to hearing the horror stories from friends in Toronto or Vancouver, that’s the kind of number that feels like a mistake. It isn’t.

What Else Does a First-Time Buyer Pay at Closing?

Beyond the Land Titles fees, plan for:

- Legal fees — $1,000 to $1,800 for a real estate lawyer in Edmonton

- Home inspection — $450 to $700 (non-negotiable; never skip this)

- Title insurance — $250 to $350 one-time

- Property tax adjustments — prorated to the closing date

- Home insurance binder — roughly $100-$150/month, first month due at closing

- Appraisal fee — $400-$600 (often waived by the lender on standard deals)

Total closing costs for a typical first-time Edmonton buyer land at $3,500 to $5,500 above the down payment. Add that to your savings target early so you aren’t scrambling the week before possession.

Our take: The biggest closing-day disaster to watch for isn’t about money. Imagine a buyer who forgets to transfer utilities into their name before possession day and shows up to the new house with no power, no water, and a moving truck in the driveway. Book your utility transfers the day your condition removal is signed. It takes 15 minutes and saves a very long afternoon.

For every line item — legal, inspection, title insurance, and adjustments — see our complete Alberta closing cost breakdown.

What’s Happening in the Edmonton Housing Market Right Now?

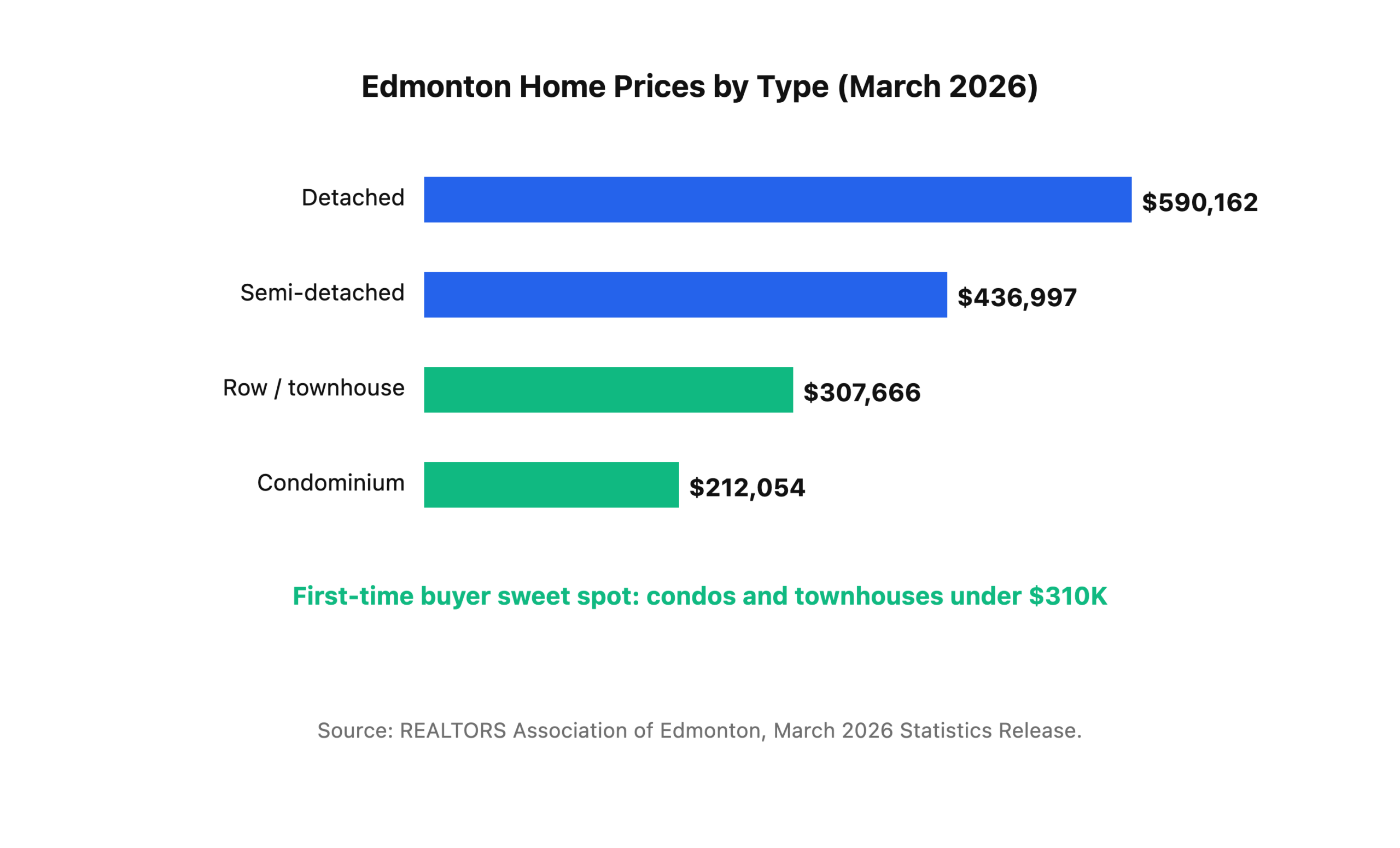

Edmonton recorded 2,133 residential sales and 3,809 new listings in March 2026, with the MLS HPI composite benchmark at $426,000 — a year-over-year drop of 2.9% that signals a market cooling from its 2024-2025 peak (REALTORS Association of Edmonton, April 2026). Inventory is climbing. Sellers are sharpening their pencils. For first-time buyers who waited out the 2023-2024 rate shock, the negotiating window is wider than it’s been in three years.

Here’s what the March 2026 data tells first-time buyers about the current market:

- Detached homes averaged $590,162 — up 2.5% year-over-year. Still the strongest and tightest segment.

- Semi-detached averaged $436,997 — up 1.6%. The underrated middle ground.

- Row and townhouses averaged $307,666 — down 2.2%. The relief valve for buyers under $350K.

- Condominiums averaged $212,054 — down 2.8%. Back to 2019 pricing in real terms.

Translation for first-time buyers: the condo segment is on sale, and that’s where many Edmonton first-timers should be looking in 2026. A $250,000 condo with 5% down ($12,500) and a 30-year amortization at today’s rates lands a mortgage payment around $1,350/month. Add condo fees, property tax, and insurance, and total carrying costs land near $1,800/month — not far above what the same unit rents for in most Edmonton neighborhoods, and you’re building equity with every payment.

What Are the Biggest Mistakes Edmonton First-Time Buyers Make?

Across Edmonton, Calgary, and greater Alberta, the same five mistakes show up over and over among first-time buyers — and four of them cost buyers five figures or more. If you recognize yourself in any of these, it’s fixable.

1. Shopping for a Home Before Getting Pre-Approved

Every week we meet buyers who fell in love with a house in Terwillegar or Summerside, only to find out their real budget was $50K short of the list price. A pre-approval takes 48 hours and costs nothing. Always do it first.

2. Forgetting the Full Closing Cost Budget

Buyers save diligently for the down payment and forget about legal fees, inspection, insurance, title insurance, and property tax adjustments. Then they can’t close. Add $3,500-$5,500 to your savings target on day one.

3. Switching Jobs or Buying a Car Mid-Deal

Your lender re-verifies employment and debt the week of closing. A surprise car payment — even a modest one — can sink a tight pre-approval. Hold off on any significant financial moves until your possession day is in the rearview mirror.

4. Taking the First Rate a Bank Offers

Your own bank has exactly one rate sheet. A mortgage broker has 30+ lenders competing for the same deal. On a $400,000 mortgage, a 0.25% rate difference over a 5-year term works out to around $4,800 — real money for a first-time buyer.

5. Skipping the Home Inspection to Win a Bidding War

It feels like a competitive edge in a hot market. It isn’t. Imagine skipping a $600 inspection and inheriting a $22,000 furnace replacement a few months later — it happens more often than buyers expect. Never waive the inspection condition, even when the listing agent pressures you. A good realtor will tell you the same thing.

Want the full list with fixes for each? Read the five first-time buyer mistakes we see every month in Edmonton.

Should You Work With a Bank or a Mortgage Broker?

A Canadian mortgage broker has access to 30+ lenders — banks, credit unions, monolines, B-lenders, and private pools — while your bank has access to exactly one: itself (Alberta Mortgage Brokers Association, 2025). That’s the core difference, and it matters more for first-time buyers than for anyone else. A broker can find options a bank won’t or can’t offer, often at a better rate than the bank would have quoted its own walk-in customer.

Metro Mortgage Group is an independent Edmonton brokerage with 7 brokers and 229 five-star Google reviews across 15 years of serving Alberta buyers. Each broker specializes. Daniel De Sousa and Ariell Laszchuk focus on first-time buyers. Nelson Sousa brings 9+ years of construction-company experience to new-build and construction mortgages. Miguel Cunha handles the private and B-lender deals for borrowers the big banks turn down. When you call us, you get matched with the person who actually closes deals like yours every week.

The broker doesn’t cost you anything on a standard residential mortgage. Lenders pay the broker commission after funding, and broker rates are typically the same or better than walking into the bank directly. There’s no downside for a first-time buyer to get a second opinion from a broker before signing with a bank — and there’s often thousands of dollars upside.

Frequently Asked Questions

How much income do I need to buy a house in Edmonton in 2026?

For Edmonton’s $426,000 benchmark home with 5% down, you typically need a household income of $90,000-$100,000 to pass the federal stress test (OSFI, 2026). Higher if you carry car payments, student loans, or credit card balances. Lower if you’re putting down more than 5% or targeting a condo under $250,000.

Can I use both the FHSA and the RRSP Home Buyers’ Plan?

Yes — and you should. The FHSA ($40,000 lifetime) and the RRSP Home Buyers’ Plan ($60,000) are stackable under current CRA rules (Canada Revenue Agency, 2026). A single first-time buyer can access $100,000 tax-free toward a down payment. A couple who both qualify can access $200,000 combined.

What credit score do I need for a mortgage in Alberta?

CMHC requires a minimum credit score of 600 for at least one borrower on an insured mortgage, though most lenders prefer 680+ for the best interest rates (CMHC, 2025). Below 600, you’ll be looking at alternative (B-lender) options — still possible, typically at a 1-2% rate premium.

Do I have to pay CMHC insurance if I put 5% down?

Yes. Any mortgage with less than 20% down in Canada requires default insurance from CMHC, Sagen, or Canada Guaranty. At 5% down, the premium is 4.00% of the loan amount (CMHC, 2025). Most buyers add the premium to their mortgage balance rather than paying it upfront.

How long does a mortgage pre-approval last in Canada?

Most Canadian lender pre-approvals are valid for 90 to 120 days, with the contract rate held during that window. If you haven’t bought by the expiry date, you re-submit and re-qualify — and your new rate will reflect whatever the market is doing at the time of renewal.

Is it a good time to buy in Edmonton in 2026?

Edmonton’s MLS HPI benchmark dropped 2.9% year-over-year in March 2026 while inventory climbed, giving first-time buyers their best negotiating position in three years (REALTORS Association of Edmonton, April 2026). Whether it’s the right time for you depends on job stability, stress-test qualification, and how long you plan to stay. Run the numbers before you commit.

Ready to Start the Pre-Approval Conversation?

Edmonton is one of the most affordable major Canadian housing markets for first-time buyers in 2026. Between the rebuilt federal programs, the no-land-transfer-tax advantage, and a cooling local market, the conditions for a first purchase are the best they’ve been since 2021. But the window matters. Rates shift. Federal rules evolve. And the difference between getting pre-approved today versus next quarter can mean tens of thousands of dollars in borrowing power.

If you’re within 3-12 months of wanting to buy your first Edmonton home, book a free 20-minute pre-approval conversation with our first-time buyer team. We’ll walk through your numbers, your eligible programs, and your realistic shopping ceiling — no pressure, no commitment, no cost. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

Prefer to meet in person first? Visit our Edmonton mortgage broker service page for office details, team bios, and neighborhood expertise.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews across 7 brokers.

Last updated: April 7, 2026