Private Mortgages in Edmonton

Alternative lending solutions when traditional bank financing isn’t an option

Last updated: April 28, 2026

Private mortgages funded roughly $32 billion in Ontario alone during the most recent FSRA reporting cycle — about 15.8% of that province’s total mortgage market — and Alberta’s share is growing even faster as tighter bank qualification rules push more borrowers toward alternative channels (FSRA, 2025; CMHC, 2025). With the Bank of Canada’s overnight rate holding at 2.25%, held again at the Bank’s June 2026 rate announcement, A-lender qualification is technically easier than it was two years ago — yet thousands of Albertans still can’t get past the stress test, the income documentation rules, or the credit score floor (Bank of Canada, 2026).

That’s where private mortgages come in. After eight years arranging alternative and private deals across Edmonton, I’ve seen private lending save purchases, prevent foreclosures, and bridge the gap between “where you are now” and “where a bank will take you in 12 months.” This guide covers everything you need to know before considering one.

Key Takeaways

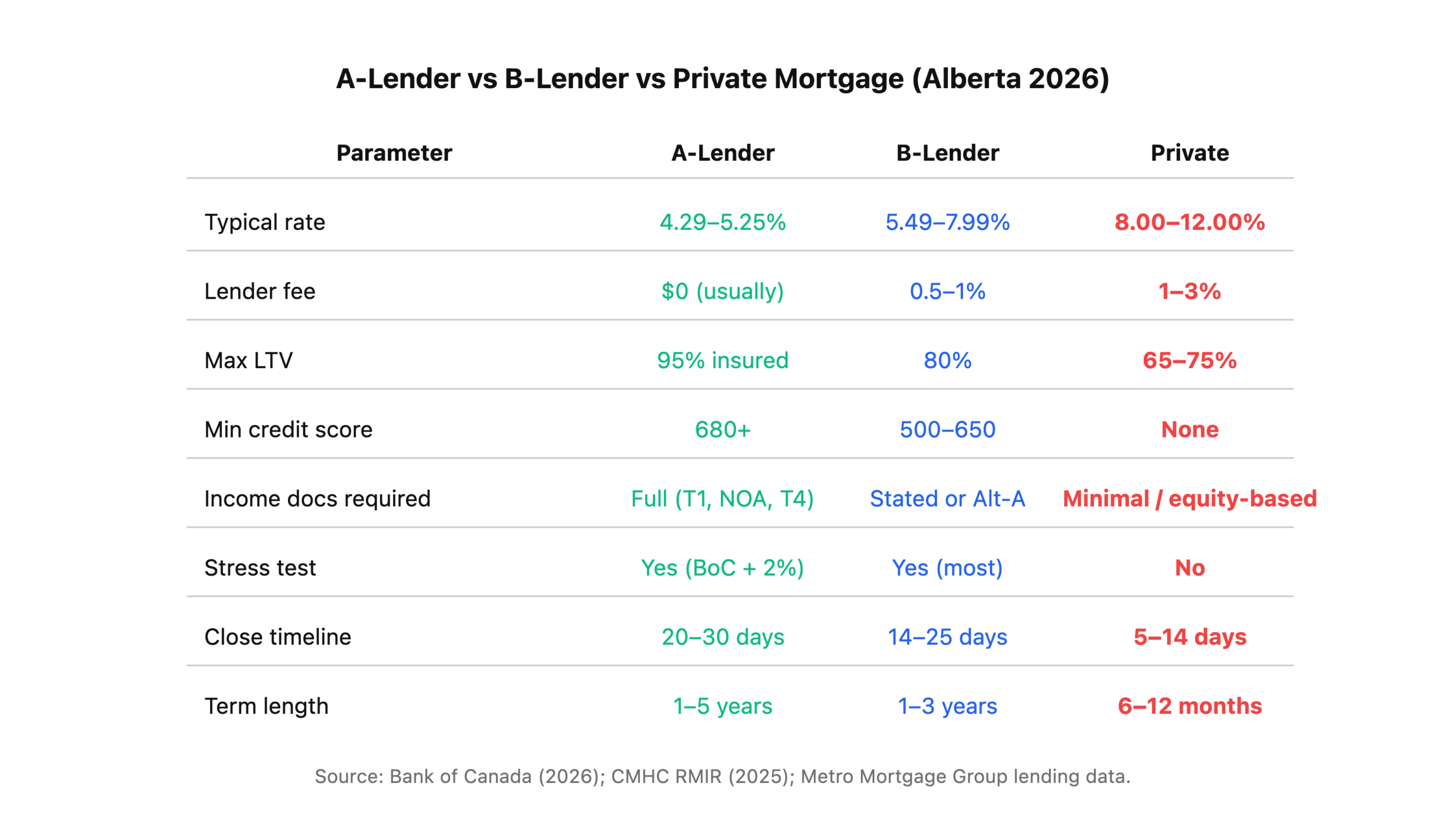

– Private mortgage rates in Alberta typically range from 8–12% on first mortgages and 10–15% on seconds, with 1–3% lender fees on top (WOWA, 2025).

– Maximum LTV is usually 65–75% on urban residential, compared to 80% uninsured or 95% insured at an A-lender.

– Private mortgages close in 5–14 days versus 20–30 days at a bank — the speed is often the entire point.

– All private mortgage arrangements in Alberta must be facilitated by a RECA-licensed mortgage broker unless the lender is lending their own funds directly (RECA, 2025).

– Every private mortgage should have a written exit strategy — how you’ll refinance back to an A- or B-lender within 12–24 months.

What Is a Private Mortgage and How Does It Differ From Bank Financing?

A private mortgage is any real estate loan funded by a non-institutional source — an individual investor, a syndicate, or a Mortgage Investment Corporation (MIC) — rather than a chartered bank, credit union, or monoline lender (CMHC, 2025). The collateral is still real property registered on title at Alberta Land Titles, the mortgage still gets a legal charge, and foreclosure still runs through Alberta Court of King’s Bench. What changes is who’s writing the cheque and how they decide to write it.

Banks underwrite the borrower — income, credit score, debt ratios, stress test. Private lenders underwrite the property — equity, location, condition, marketability. That single shift is why someone with a 520 credit score can get a private first mortgage on a Calgary bungalow with 40% equity, while that same person can’t get a credit card from their bank.

Here’s how the three lending tiers compare:

The key takeaway? Private mortgages aren’t cheaper. They’re faster, more flexible, and equity-focused. You pay a premium for those three things, and the goal is always to use them temporarily.

Citation capsule: Private mortgages in Canada are funded by non-institutional sources — individual investors, syndicates, or Mortgage Investment Corporations — and are underwritten primarily on property equity rather than borrower income, with typical rates of 8–12% and terms of 6–12 months (CMHC, 2025).

When Does a Private Mortgage Make Sense?

Private lending solves five categories of problems that banks either can’t or won’t touch — and in every case, the borrower should be using private as a bridge to somewhere better, not as a permanent home for their mortgage.

1. Bridge Financing

You’ve sold your current home, bought the next one, but the closing dates don’t line up. Your bank won’t bridge the gap because the new purchase closes 60 days before the sale. A private bridge loan, secured against the departing property’s equity, covers the down payment on the new one for 30–90 days. Cost? Typically 10–12% annualized plus a 1% lender fee — but you only hold it for a couple of months, so the dollar cost is manageable.

2. Credit Rebuilding

A consumer proposal discharged 14 months ago. A bankruptcy from three years back. Medical collections that tanked a score from 720 to 490. Banks need a minimum of two years post-discharge and a rebuilt score above 680 to consider an application. Private lenders look at the equity. If you own a home in Edmonton worth $550,000 with $200,000 owing, that’s 64% LTV — within range for most MICs. You hold the private mortgage for 12–18 months while rebuilding credit, then refinance to a B-lender or A-lender.

3. Self-Employed and Non-Traditional Income

Business owners who pay themselves dividends, contractors paid in lump sums, gig workers with inconsistent deposit patterns — the stress test assumes stable T4 employment income, and these borrowers don’t have it. A B-lender might work with stated income, but if the tax returns are too aggressive on write-offs, even B-lenders say no. Private fills the gap.

4. New-to-Canada Buyers

Newcomers with strong assets but no Canadian credit history, no two-year Canadian income track record, and no CMHC-insurable file. Private lending lets them purchase immediately, build credit, and establish income — then refinance within 12–24 months.

5. Time-Sensitive Closings

A builder won’t extend the completion deadline. A judicial foreclosure sale requires closing within 30 days. An investment property in a hot submarket won’t wait for a 25-day bank approval. When speed is the primary requirement, private lending’s 5–14 day close timeline is the solution.

Citation capsule: Private mortgages are commonly used in Canada as short-term bridge financing for misaligned closing dates, credit rebuilding after insolvency, self-employed borrowers with non-standard income, newcomers without Canadian credit history, and time-sensitive transactions requiring closes under 14 days (CMHC, 2025).

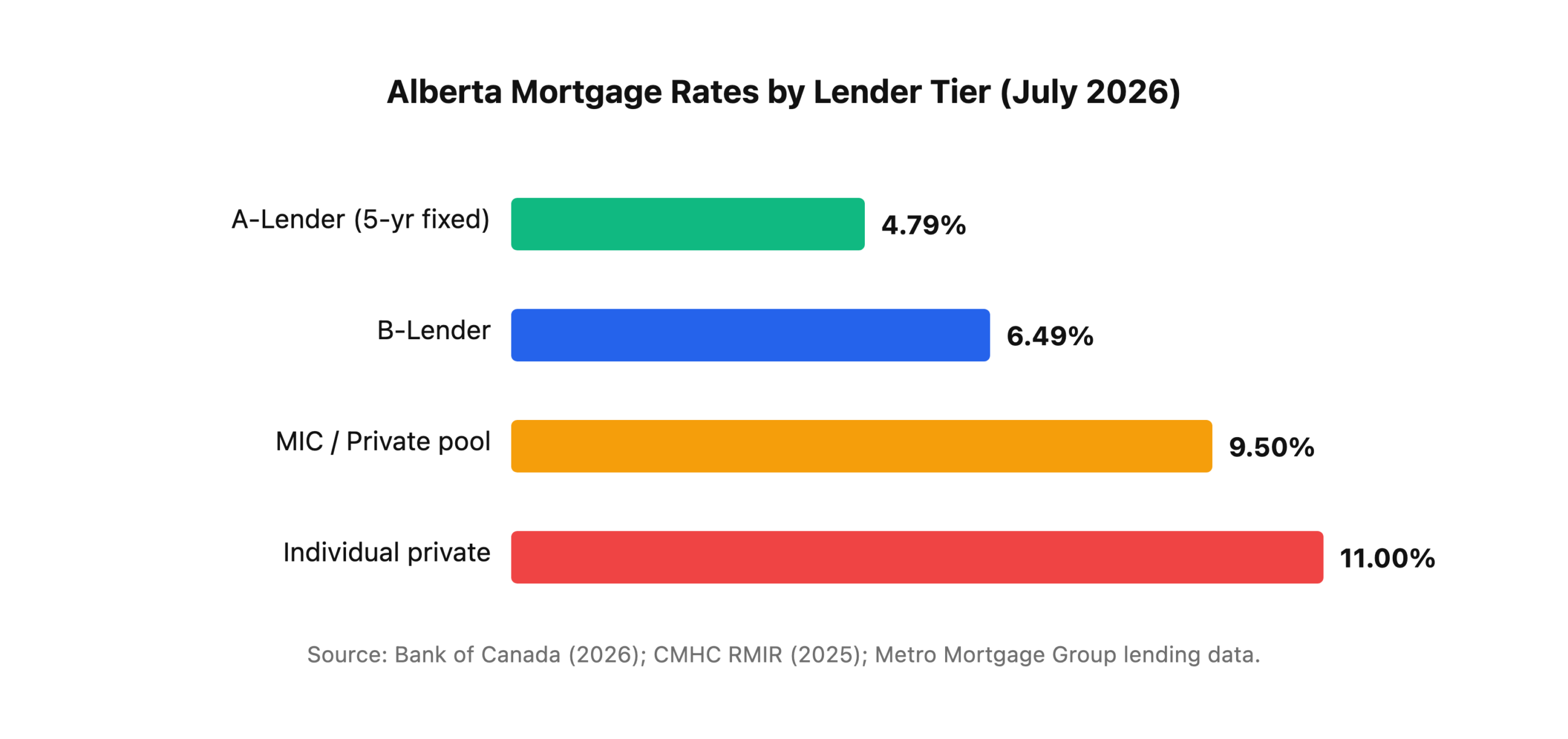

What Do Private Mortgage Rates and Fees Look Like in Alberta?

Expect to pay 8–12% on a first mortgage and 10–15% on a second mortgage through a private lender in Alberta, plus 1–3% in lender fees and 1–2% in broker fees — making the effective annual cost significantly higher than the posted rate (WOWA, 2025; Best Rates, 2026).

Here’s what a typical private first mortgage looks like in real dollars:

Example: $400,000 private first mortgage at 10%, 1-year term, interest-only

- Monthly interest payment: $3,333

- Lender fee (2%): $8,000 (deducted from advance)

- Broker fee (1.5%): $6,000 (deducted from advance)

- Legal fees: $2,000–$2,500

- Appraisal: $350–$500

- Total cost over 12 months: ~$56,500 on a $400,000 loan

That works out to roughly 14.1% effective annual cost when you factor in the upfront fees. It’s expensive. No one disputes that. But if the alternative is losing a $60,000 deposit on a property or watching a judicial foreclosure consume $150,000 in equity, the math works in the borrower’s favour.

Rates vary widely depending on LTV, property location (Edmonton urban vs. rural Alberta), property condition, and the borrower’s overall story. A clean first mortgage at 55% LTV on a well-maintained Windermere bungalow might come in at 8.5%. A messy second mortgage on a rural acreage at 80% combined LTV could push 14–15%.

MIC Lending vs Individual Private Lenders: What’s the Difference?

Mortgage Investment Corporations are the fastest-growing segment of Canada’s mortgage industry — MIC assets jumped 268% between 2007 and 2021, from under $10 billion to over $36.5 billion nationally (WOWA, 2025). Understanding the difference between a MIC and an individual private lender matters because it affects your rate, your terms, and your protections.

Mortgage Investment Corporations (MICs)

A MIC is a pooled investment fund regulated under Section 130.1 of the Income Tax Act that collects money from investors and lends it out as mortgages (Income Tax Act, R.S.C. 1985). MICs must have at least 20 shareholders, hold at least 50% of their assets in residential mortgages, and distribute all taxable income to shareholders annually.

For borrowers, MICs tend to offer:

- Lower rates (8–10% vs. 10–13% individual)

- More standardized terms with clearer documentation

- Professional underwriting by licensed mortgage brokers

- Larger loan amounts (some Alberta MICs lend up to $2–3M)

- More predictable renewals — the fund is ongoing, not dependent on one person’s circumstances

Individual Private Lenders

An individual private lender is a person investing their own money — sometimes RRSP or TFSA funds — directly into a mortgage on your property. They’re lending on one deal at a time, and their terms reflect their personal risk tolerance.

Individual lenders tend to offer:

- Higher rates (10–15%) to compensate for concentration risk

- Shorter terms (6 months is common)

- Less standardized documentation and renewal processes

- More negotiation room on unusual deals banks and MICs won’t touch

- Faster decision-making — sometimes same-day approval

At Metro, we work with both MIC pools and a network of individual private investors. For most residential private deals in Edmonton, we start with MIC pricing because it’s typically the best rate. Individual lenders fill the gap on unusual properties, higher LTVs, or situations where a MIC’s underwriting guidelines don’t quite fit.

Citation capsule: Mortgage Investment Corporations (MICs) are pooled investment funds regulated under Section 130.1 of Canada’s Income Tax Act, requiring at least 20 shareholders and 50% residential mortgage assets, with industry assets growing 268% from $10B to $36.5B between 2007 and 2021 (WOWA, 2025; Income Tax Act, R.S.C. 1985).

How Does RECA Regulate Private Lending in Alberta?

Alberta’s private lending market is regulated by the Real Estate Council of Alberta (RECA) under the Real Estate Act — and as of 2025, RECA has made private lending a mandatory education topic for every licensed mortgage broker and associate in the province (RECA, 2025).

Here’s what the regulatory framework means for borrowers:

Who Needs a Licence?

Any person who arranges mortgages on behalf of another for compensation must hold a RECA mortgage broker licence. However, individuals lending their own money directly (not through a broker) are exempt from licensing requirements. In practice, most private mortgage transactions in Alberta involve a licensed broker because borrowers rarely find private lenders on their own.

Broker Obligations on Private Deals

When a RECA-licensed broker places you with a private lender, they’re required to:

- Disclose all fees — broker fees, lender fees, legal costs — in writing before commitment

- Confirm suitability — document why private lending is appropriate given your circumstances

- Present the exit strategy — explain how and when you’ll transition to institutional financing

- Disclose the lender relationship — if the broker or brokerage has a financial interest in the lending entity (e.g., they own shares in the MIC), that must be disclosed upfront

- Maintain trust account compliance — all funds flow through designated trust accounts

The 2025 Private Lending Relicensing Mandate

RECA’s Mortgage Broker Industry Council mandated that all licensed mortgage professionals in Alberta complete a Private Lending relicensing course in 2025 — a recognition that private lending volumes are growing and that consumer protection standards needed strengthening (RECA, 2025). This is a positive development for borrowers because it means every Alberta mortgage professional should now understand the risks, suitability requirements, and disclosure obligations specific to private deals.

Citation capsule: In Alberta, mortgage brokers arranging private mortgage transactions must be licensed by the Real Estate Council of Alberta (RECA) under the Real Estate Act, with mandatory disclosure of all fees, suitability confirmation, exit strategy documentation, and related-party lender relationships (RECA, 2025).

What Are the Risks — and How Do You Protect Yourself?

Private mortgages carry real risks that institutional mortgages don’t, and anyone considering this path should understand them clearly before signing a commitment letter.

The Risks

Higher total cost. A private mortgage at 10% with 2% in fees on a $400,000 loan costs roughly $56,500 per year. The same amount at a typical A-lender rate costs thousands less per year — often tens of thousands less over the loan’s term.

Renewal uncertainty. When the 12-month term expires, the private lender isn’t obligated to renew. If your exit plan hasn’t materialized — credit score hasn’t recovered, income hasn’t stabilized, property value dropped — you could face a forced sale or judicial foreclosure through the Court of King’s Bench.

Equity erosion. The lender fee, broker fee, legal costs, and interest payments all reduce your net equity. On a short-term deal, this is manageable. On a private mortgage that gets renewed three or four times because the exit strategy keeps failing, the borrower can lose significant equity.

Predatory lending. Not all private lenders operate ethically. Some charge excessive fees, bury prepayment penalties in fine print, or structure deals designed to fail so they can acquire the property. Working with a RECA-licensed broker is the primary protection against this.

The Protections

- Always use a RECA-licensed mortgage broker — they have fiduciary-adjacent duties and regulatory accountability

- Get an independent legal opinion — your lawyer reviews the commitment letter before you sign, separate from the lender’s lawyer

- Insist on a written exit strategy — documented plan showing how you’ll refinance to a B-lender or A-lender, with realistic timelines and benchmarks

- Request an independent appraisal — don’t rely on the lender’s valuation; get your own AACI-designated appraiser

- Understand every fee — lender fee, broker fee, discharge fee, renewal fee, prepayment penalty, legal fee — all in writing before commitment

Citation capsule: Private mortgage risks in Canada include higher total borrowing costs (effective rates of 14%+ including fees), renewal uncertainty at term end, equity erosion from compounding fees, and potential predatory lending practices, mitigated by using RECA-licensed brokers, independent legal counsel, and written exit strategies (RECA, 2025; FSRA, 2025).

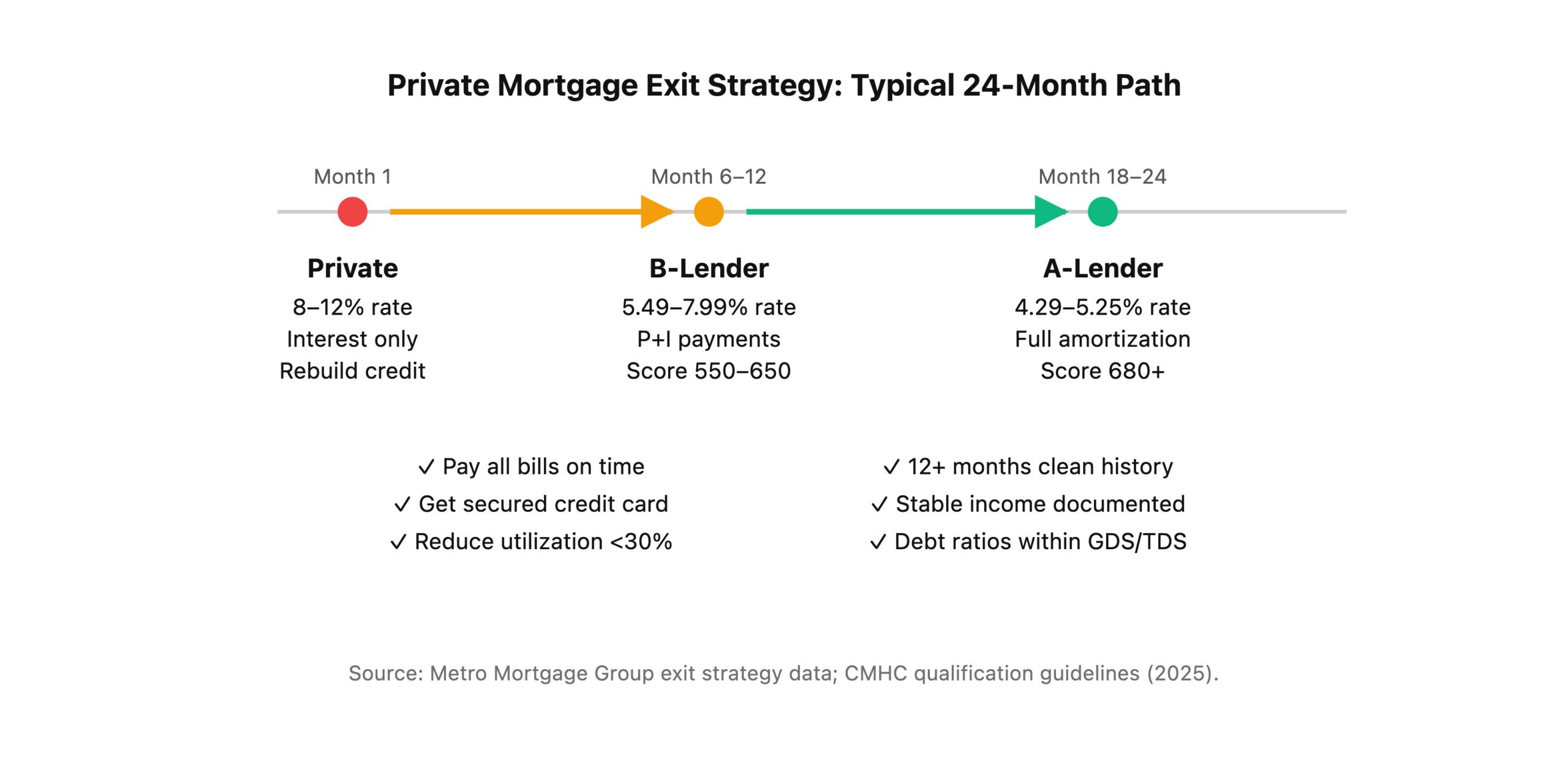

How Do You Exit a Private Mortgage?

Every private mortgage should have an exit strategy documented before the first dollar is advanced — and that exit strategy should be realistic, not aspirational. Here’s the typical timeline for transitioning back to institutional financing:

The Typical Exit Path

Months 1–6 (Private): You’re paying interest only at 8–12%. During this period, you’re actively rebuilding credit — paying every bill on time, getting a secured credit card with a $1,000–$2,000 limit, and keeping utilization below 30%. If the private mortgage was for bridge financing, you exit as soon as the departing property sells — usually within 60–90 days.

Months 6–12 (B-Lender transition): Once your credit score crosses the 550–600 threshold and you have 6+ months of clean payment history, a B-lender can usually take the file. Rates drop to 5.49–7.99%, payments shift to principal and interest, and you’re on a 1–3 year term.

Months 18–24 (A-Lender refinance): With 18–24 months of clean history, a score above 680, and stable documented income, most A-lenders will qualify the refinance. You’re now at 4.29–5.25% on a 5-year term with a 25-year amortization. Mission accomplished.

Not every borrower completes this path in 24 months. Some take 36 months. Some get stuck at the B-lender stage because they can’t pass the stress test. The point is to have the roadmap documented, with realistic benchmarks, so everyone — borrower, broker, and lender — knows the plan.

What Does Metro’s Private Lending Process Look Like?

Metro Mortgage Group has been arranging private mortgages in Edmonton since 2011, and our process is designed to get you funded quickly while protecting you from the risks outlined above.

Step 1: Initial Consultation (Same Day)

We review your situation — why you need private, what went wrong with A/B-lender applications, and what your 12–24 month outlook looks like. We need to understand the exit strategy before we even discuss the mortgage.

Step 2: Property and Equity Assessment (Day 1–2)

We order an appraisal (or use a recent one if available), pull title, and confirm the equity position. Private lending is equity-first, so this step determines what’s possible.

Step 3: Lender Matching (Day 2–3)

With 30+ lenders in our network — including multiple Alberta MIC pools and individual private investors — we match your file to the lender offering the best rate and terms for your specific situation. MIC first, individual private second.

Step 4: Commitment Letter (Day 3–5)

You receive a written commitment outlining: rate, term, lender fees, broker fees, prepayment terms, and renewal conditions. We review every line with you before you sign.

Step 5: Legal and Funding (Day 5–14)

Your lawyer reviews the mortgage documents, the lender’s lawyer registers the charge on title, and funds are advanced. On a straightforward deal, this can happen as quickly as 5 business days from first contact.

Step 6: Exit Strategy Monitoring (Ongoing)

We don’t disappear after funding. At months 3, 6, and 9, we check in on credit rebuilding progress, income documentation, and market conditions so we can time the B-lender or A-lender transition optimally.

Illustrative Scenarios: How Private Mortgages Can Solve Real Problems

The three scenarios below are hypothetical, illustrative composites — not accounts of specific real clients — built from the types of deals private and alternative lenders arrange in the Edmonton market. Names, figures, and details are for illustration only.

Scenario 1: The Misaligned Closing (Illustrative Example)

Situation: A family in Summerside purchased their next home before their existing home sold. The new build’s completion date was firm — the builder wouldn’t extend. The old home was listed but hadn’t sold, and the bank wouldn’t provide bridge financing because the existing home’s sale wasn’t yet unconditional.

Solution: A private bridge loan of $180,000 at 10%, secured as a second mortgage on the departing property. The loan funded in 7 days. The old home sold six weeks later, and the private mortgage was discharged. Total cost: approximately $2,075 in interest plus $3,600 in fees.

Scenario 2: The Consumer Proposal (Illustrative Example)

Situation: A self-employed electrician in Sherwood Park had completed a consumer proposal 15 months earlier. His credit score was 510. He owned his home free and clear — worth $480,000 — but needed $120,000 to purchase equipment and hire two apprentices for a large commercial contract.

Solution: A private first mortgage at 9.5% (25% LTV — well within comfort for any MIC), 12-month term, interest only. At month 10, with his credit score rebuilt to 610 and the commercial contract generating documented income, we moved him to a B-lender at 6.75% on a 2-year term.

Scenario 3: The New-to-Canada Purchase (Illustrative Example)

Situation: A software engineer who’d arrived from India eight months earlier with $200,000 in verified savings wanted to purchase a $650,000 townhouse in Windermere. No Canadian credit history. Solid employment with a major tech employer, but only eight months of Canadian income — banks require two years for a conventional mortgage.

Solution: A MIC first mortgage at 8.75% (69% LTV), 12-month term. At month 14, with a Canadian credit score of 690 and 22 months of employment income, the file qualified for an A-lender refinance at 4.89%.

Frequently Asked Questions

Can I get a private mortgage on a rural property in Alberta?

Yes, but expect tighter LTV limits — usually 50–60% maximum versus 65–75% for urban Edmonton. Private lenders want properties they can sell quickly if they need to, and rural acreages take longer to move than a bungalow in Mill Woods. The rate will also be higher, typically 10–13%, reflecting the added risk.

How fast can a private mortgage actually close?

With clean title, a recent appraisal already in hand, and a motivated MIC lender, we’ve closed deals in as little as a few business days when circumstances allow. More realistically, plan for 7–10 business days for a straightforward residential first mortgage. Complex deals with title issues, shared wells, or non-standard property types can take 14–21 days.

Do I need a down payment for a private mortgage?

If you’re purchasing, yes — private lenders typically require 25–35% down (65–75% LTV). If you’re refinancing an existing property, no down payment is needed — you need sufficient equity in the property to stay within the lender’s LTV limits. For a second mortgage, the lender looks at your combined LTV (first mortgage plus the new second), which usually caps at 75–80%.

Will a private mortgage hurt my credit score?

Not directly — most private lenders and MICs don’t report to Equifax or TransUnion. However, if you miss payments and the lender initiates judicial foreclosure proceedings, that will appear on your credit report. The lack of reporting also means private mortgage payments don’t help rebuild your credit, which is why we recommend getting a secured credit card and small instalment loan alongside the mortgage.

What happens if I can’t refinance at the end of the term?

If your exit strategy hasn’t materialized — credit hasn’t recovered, income isn’t documented, property value has dropped — you have three options: renew with the same private lender (if they’re willing, usually at a higher rate), find a new private lender (your broker handles this), or sell the property to preserve whatever equity remains. The worst outcome is doing nothing and letting the lender initiate judicial foreclosure. Talk to your broker at least 90 days before maturity so there’s time to find a solution.

Ready to Explore Private Lending Options?

Private mortgages aren’t for everyone — but when they’re the right fit, they solve problems no bank will touch. The difference between a good outcome and a bad one almost always comes down to the broker’s lender network, the exit strategy, and the disclosure process.

At Metro Mortgage Group, we’ve been arranging private and alternative mortgages in Edmonton since 2011, with access to 30+ lenders including multiple Alberta MIC pools. We’ll tell you if private is the right move — and if it’s not, we’ll show you the alternatives.

Call Miguel Cunha at 780-974-1270 or book a free consultation online to discuss your situation. Every conversation starts with the exit strategy.

Miguel Cunha is a licensed mortgage broker with Metro Mortgage Group Inc. in Edmonton, Alberta, specialising in commercial, alternative, and private mortgage solutions. Metro Mortgage Group was founded in 2011 and maintains a 5.0-star rating across 229 Google reviews. RECA licence held under Metro Mortgage Group Inc.