Alberta Mortgage Rates: 2026 Guide

Fixed vs variable, rate holds, prepayment, and current market trends

Last updated: July 7, 2026

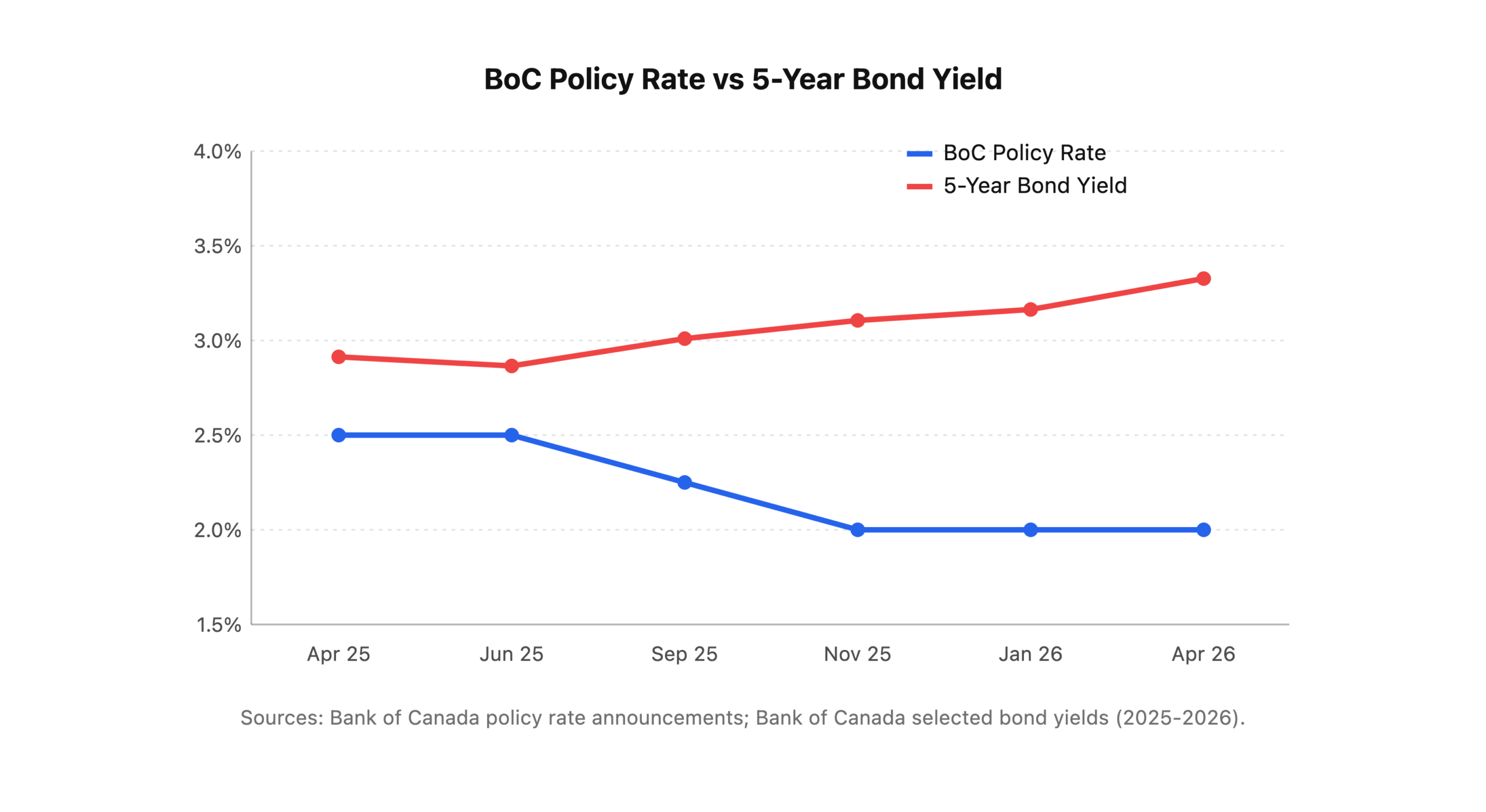

Alberta mortgage rates have dropped significantly from their 2023 peak — but 2026 isn’t delivering the straight-down trajectory many buyers were hoping for. The Bank of Canada’s policy rate sits at 2.25% after three consecutive holds (Bank of Canada, 2026), while 5-year fixed rates hover near 3.75% and variable rates trade around 3.30% (WOWA, April 2026). With bond yields climbing on global uncertainty and the next rate decision scheduled for July 15, 2026 (following the June 10, 2026 hold), Alberta borrowers need a clear picture of what’s moving rates and what to expect for the rest of the year.

This guide breaks it all down. No jargon. No predictions dressed up as certainties. Just the numbers, the mechanics, and the decisions that’ll determine what you actually pay on your Alberta mortgage in 2026.

Key Takeaways

– Bank of Canada policy rate: 2.25% since October 2025 — three straight holds, with markets pricing in one possible cut later in 2026 (Bank of Canada, 2026).

– Best 5-year fixed insured rates in Alberta: ~3.75%-3.89% through brokers; ~4.19%+ at big banks (Ratehub, April 2026).

– Best 5-year variable rates: ~3.30% through broker channel vs 3.65%+ at major banks (WOWA, April 2026).

– The 5-year Government of Canada bond yield hit 3.12% in early April 2026 — up 42 bps year-over-year, which puts upward pressure on fixed rates (Bank of Canada, 2026).

– Using a mortgage broker can meaningfully reduce your rate compared to walking into a big bank — the exact savings depend on your credit profile, down payment, and the lenders competing for your file.

Where Do Alberta Mortgage Rates Actually Sit Right Now?

As of spring 2026, Alberta mortgage rates are lower than the 2023-2024 peaks but haven’t reached the sub-3% levels some borrowers expected. Here’s the current picture for insured mortgages (Ratehub, April 2026; WOWA, April 2026):

| Term | Broker Best Rate | Big Bank Posted | Spread |

|---|---|---|---|

| 5-year fixed | 3.75% | 4.19%-4.49% | 0.44-0.74% |

| 3-year fixed | 3.89% | 4.34% | 0.45% |

| 5-year variable | 3.30% | 3.65% | 0.35% |

| 2-year fixed | 4.09% | 4.54% | 0.45% |

Why the gap? Brokers access 30+ lenders competing for your file. A big bank quotes from one rate sheet. That structural difference puts thousands of dollars in your pocket over a 5-year term.

Rates vary slightly across Alberta. Edmonton borrowers and Calgary borrowers see nearly identical pricing because Canada’s mortgage market is national, not regional. What affects your rate more than your postal code? Your down payment size, credit score, and whether you go insured or conventional.

Want to see how these rates translate to monthly payments? Our mortgage affordability calculator shows what you’d qualify for at today’s rates.

For the latest numbers, check back for our monthly rate updates.

Fixed vs Variable: Which Rate Type Wins in 2026?

The fixed-vs-variable decision is the most consequential rate choice you’ll make on your mortgage — and the right answer changes depending on the year. In 2026, the spread between the two has narrowed to roughly 45 basis points, making this a closer call than it’s been in years (Ratehub, April 2026).

Here’s how the two options compare on a $450,000 mortgage with a 25-year amortization:

When fixed makes sense in 2026: You’re risk-averse, your budget has no room for a payment increase, or you believe bond yields will keep climbing on geopolitical uncertainty. Fixed also wins if you plan to stay past the 5-year term and want renewal predictability.

When variable makes sense: You can absorb a potential $100-200/month increase, you believe the Bank of Canada will cut again later in 2026, or you want the penalty advantage (3 months’ interest on variable vs an interest rate differential on fixed — which can cost tens of thousands on early breaks).

Historically, variable-rate borrowers have paid less than fixed-rate borrowers roughly 85-90% of the time, according to a widely cited 2001 study by York University finance professor Moshe Milevsky (York University). But 2022-2023 was a painful exception. History favours variable — but it doesn’t guarantee it.

Deep dive: Fixed vs. variable breaks down the penalty math, break-even scenarios, and which choice our Metro clients have been making most in 2026.

How Are Canadian Mortgage Rates Actually Set?

Most Albertans think the Bank of Canada sets their mortgage rate. That’s only half true. The Bank’s policy rate directly controls variable mortgage rates but has limited influence over fixed rates. Understanding the two pricing engines helps you time your rate decisions better.

Variable Rates Follow the Bank of Canada

Your variable-rate mortgage is priced as prime rate minus a discount (or plus a premium). The Bank of Canada’s overnight rate currently sits at 2.25%, which puts the bank prime rate at 4.45% (Bank of Canada, 2026). A typical broker-channel variable rate of prime minus 1.15% gives you 3.30%.

When the Bank of Canada cuts by 25 bps, prime drops 25 bps, and your variable payment drops immediately (on an adjustable-rate mortgage) or your amortization shortens (on a variable with fixed payments). It’s that direct.

Fixed Rates Follow the Bond Market

Five-year fixed mortgage rates track the 5-year Government of Canada bond yield — not the Bank of Canada rate. As of early April 2026, that bond yield sits at 3.12%, up from 2.70% a year ago (Bank of Canada, 2026). Lenders add a spread (typically 0.60-0.80%) to cover risk and profit, which is how you get to the 3.75% range on insured fixed mortgages.

This is why fixed rates can rise even when the Bank of Canada cuts. In fact, that’s exactly what happened in late 2025 — the Bank cut by 75 bps, but bond yields climbed on Middle East uncertainty and tariff fears, keeping fixed rates stubbornly elevated.

The takeaway? Don’t wait for the Bank of Canada to “drop rates” if you’re shopping for a fixed mortgage. Watch the bond market instead. And if you’re watching for variable rate relief, the Bank’s next announcement on July 15, 2026 is the one to mark.

What’s the Alberta Mortgage Rate Forecast for the Rest of 2026?

Nobody knows with certainty where rates are going — and anyone who tells you otherwise is selling something. But here’s what the major forecasters are saying as of spring 2026:

Bank of Canada policy rate: Most major banks (RBC, TD, BMO) expect the overnight rate to hold at 2.25% through most of 2026, with a possible 25 bps cut in Q4 if the economy weakens further (RBC Economics, 2026). Scotiabank and National Bank are outliers — they see the potential for 0.25-0.50% in hikes if oil-driven inflation resurfaces.

Five-year fixed rates: With bond yields elevated at 3.12%, fixed rates are unlikely to drop below 3.50% in 2026 unless global uncertainty pushes investors into safe-haven Canadian bonds. The realistic range for insured 5-year fixed rates through year-end: 3.60%-4.10%.

Five-year variable rates: If the Bank holds at 2.25%, variable rates stay near 3.30%. One 25 bps cut would push them toward 3.05%. One hike would send them to 3.55%. The band is narrow.

Key Risks That Could Move Rates

- Upside risk (rates rise): Oil price spikes from Middle East tensions, tariff escalation pushing up import costs, or inflation rebounding above 2.5%.

- Downside risk (rates fall): Labour market deterioration (unemployment already 6.7% in February), GDP growth stalling below the Bank’s 1.1% forecast, or a global recession pulling bond yields down.

Alberta-specific factor: the province’s 2.7% GDP growth forecast for 2026 (ATB Financial, March 2026) outpaces the national average. Strong provincial growth supports housing demand but doesn’t directly drive mortgage rates, since those are set nationally.

Monthly check-ins: We publish rate updates every month so you’re never guessing about where things stand.

How Do You Get the Best Mortgage Rate in Alberta?

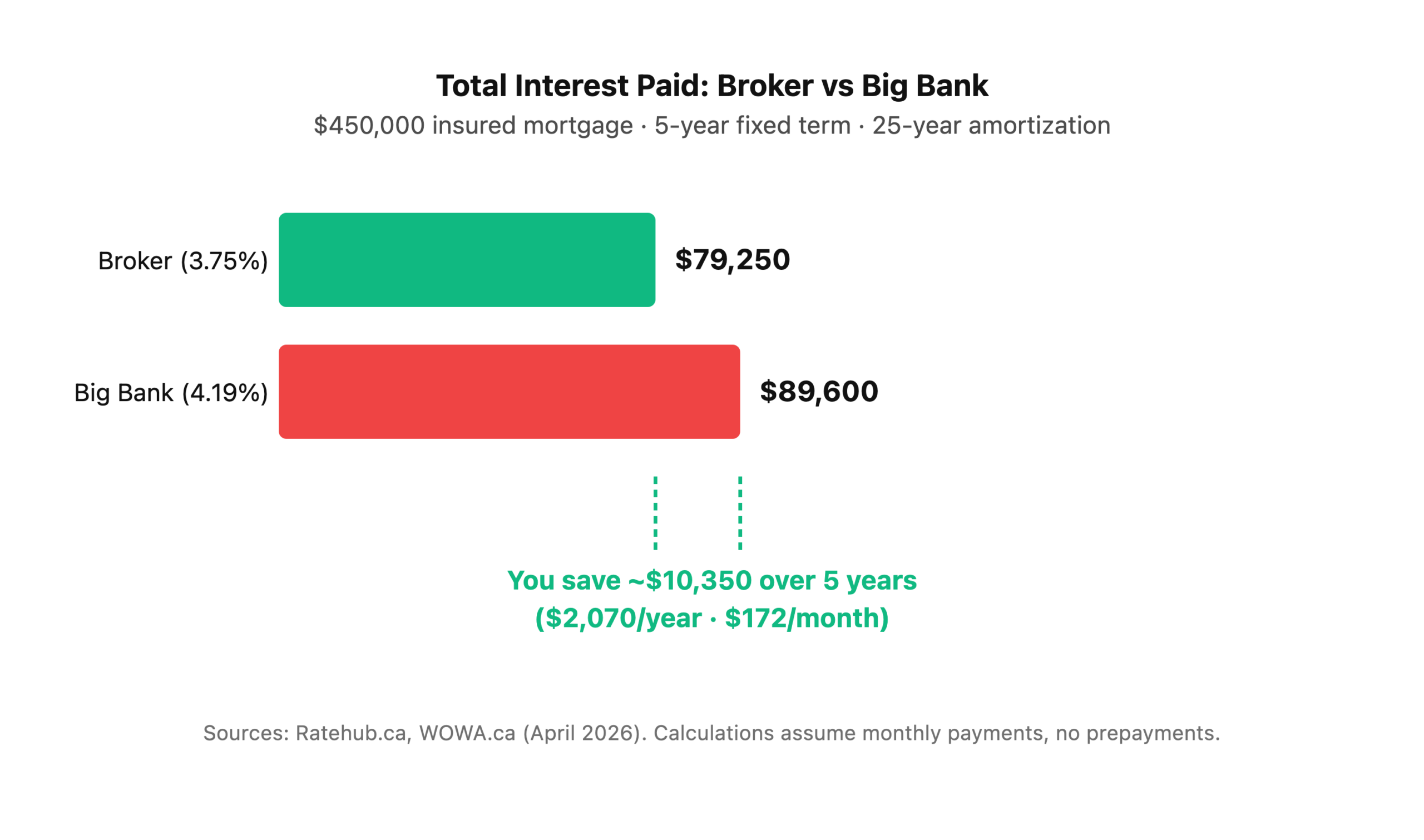

The difference between a good rate and a great rate on a $450,000 mortgage is $8,000-$14,000 over a 5-year term. Here’s what actually moves the needle.

1. Use a Mortgage Broker (Not Just Your Bank)

Brokers access 30+ lenders and can shop your file across all of them. The average broker-vs-bank spread in early 2026 is 0.30-0.50% on 5-year fixed rates (Ratehub, April 2026). On a $450,000 mortgage, that spread saves roughly $700-$1,100 per year in interest.

And here’s the part people miss: brokers don’t cost you anything. Lenders pay the broker’s commission when your mortgage funds. You get better rates and someone negotiating on your behalf — for free.

2. Get Insured If You Can

Counterintuitively, putting less than 20% down often gets you a lower interest rate. Why? CMHC-insured mortgages carry no default risk for the lender, so they offer better pricing. The insurance premium (2.80%-4.00% of the loan, depending on your down payment) gets added to your mortgage balance (CMHC, 2026). On a $450K purchase with 5% down, the rate advantage usually more than offsets the premium cost.

3. Lock a Rate Hold Early

Most lenders offer 90-120 day rate holds at no cost. If rates drop before closing, you get the lower rate. If rates rise, you’re protected. There’s no downside to locking early — and plenty of upside.

How holds work: Rate holds explained covers the mechanics, the fine print, and when to ask for an extension.

4. Optimize Your Credit Before Applying

A credit score above 680 qualifies you for the best rates. Above 750, you unlock the absolute lowest pricing from the most aggressive lenders. Below 680, you’re looking at B-lender territory with rates 1-2% higher.

Quick wins: pay credit card balances below 30% utilization, dispute any errors on your bureau, and avoid opening new credit in the 6 months before your application.

5. Negotiate Prepayment Privileges

Rate isn’t the only number that matters. A mortgage with 20/20 prepayment privileges (20% lump sum annually + 20% payment increase) versus 10/10 can save you years and tens of thousands in interest if you use it.

Comparison guide: Prepayment privileges compared ranks lender prepayment terms in Canada.

Broker vs Bank: What’s the Real Difference on Rates?

This isn’t just a Metro sales pitch — the numbers speak for themselves. Here’s a side-by-side on a $450,000 insured mortgage at 25-year amortization as of April 2026:

Why don’t more people use brokers? Familiarity bias. Most Canadians walk into whichever bank they’ve used since they were eighteen. That loyalty costs them thousands. A broker’s job is to make lenders compete for your business — and competition drives rates down.

At Metro Mortgage Group, we work with 30+ lenders across Canada. We’re not tied to one rate sheet. We shop your file, find the best rate, and handle the paperwork. That’s why our clients consistently land rates below what the big banks post.

How Do CMHC Rules and the FHSA Affect Your Rate in 2026?

Two federal programs significantly impact what Alberta borrowers pay in 2026. Neither one changes your interest rate directly — but both change the total cost of borrowing.

CMHC Mortgage Insurance: Higher Rates or Lower Rates?

If your down payment is below 20%, you’ll pay a CMHC insurance premium ranging from 2.80% to 4.00% of your mortgage amount (CMHC, 2026). On a $450,000 mortgage with 5% down ($427,500 loan), that’s roughly $17,100 added to your balance.

But here’s the upside most people don’t know: insured mortgages qualify for lower interest rates — typically 0.10-0.20% below conventional (uninsured) rates. Why? The lender carries zero default risk on insured loans. Over a 5-year term, that rate discount often recovers a significant chunk of the insurance cost.

Since December 15, 2024, the insured mortgage cap sits at $1.5 million — up from the previous $1 million limit (Department of Finance Canada, 2024). For most Alberta buyers, this means every property on the market qualifies for insured financing. Edmonton’s average home price of $454,801 and Calgary’s $641,844 (WOWA, WOWA, 2026) both sit well within the insured threshold.

The FHSA Doesn’t Change Your Rate — But It Changes What You Can Afford

The First Home Savings Account lets first-time buyers save up to $40,000 tax-free toward a down payment (Canada Revenue Agency, 2026). Combined with the $60,000 RRSP Home Buyers’ Plan, a couple can shelter up to $200,000 in tax-advantaged down payment savings.

A larger down payment doesn’t directly lower your interest rate (insured buyers often get better rates). But it reduces your mortgage balance, which means less total interest paid regardless of rate. And if you cross the 20% threshold, you avoid the CMHC premium entirely — though you’ll likely get a slightly higher rate.

The math isn’t always intuitive. That’s why talking to a broker before choosing your down payment strategy is worth the phone call.

First-time buyer? Read our complete first-time buyer guide and the deep dive on FHSA and RRSP stacking strategies.

What About Rate Locks and Timing Your Purchase?

One of the most common questions we get at Metro: “Should I wait for rates to drop?” The honest answer? Probably not. Here’s why.

The Cost of Waiting

If you wait 12 months hoping for a 0.25% rate drop, but Alberta home prices rise even 3% (well below their recent growth rate), you’re paying $13,500 more on a $450,000 home. The 0.25% rate drop saves you roughly $2,800 over a 5-year term. You’d lose $10,700 net by waiting.

Does that mean you should rush? No. It means you should separate the rate decision from the purchase decision. Buy when you find the right home at a price you can afford. Then use a rate hold to protect yourself while you close.

How Rate Holds Work

When you get pre-approved, your lender locks your rate for 90-120 days. If rates rise before closing, your locked rate sticks. If rates fall, most lenders let you take the lower rate. It’s a free one-way bet in your favour.

Full breakdown: Rate holds explained covers hold periods, how to request extensions, and the fine print to watch for.

And if you’re debating whether to lock now or float: when to lock your mortgage rate walks through the scenarios where locking early wins and where patience pays off.

Alberta-Specific Rate Considerations

Alberta borrowers have a few unique advantages — and a few unique risks — compared to the rest of Canada.

No Land Transfer Tax

Alberta doesn’t charge a land transfer tax. On a $450,000 Edmonton purchase, you’d pay roughly $970 in land title registration fees. The same home in Toronto triggers about $5,800 in provincial land transfer tax, plus potentially another $5,800 in municipal tax (Government of Alberta, 2024). That’s $10,000+ that Alberta buyers keep in their pocket — money that could go toward a larger down payment or prepayments.

Alberta Housing Is Still Affordable Relative to the Rate Environment

Even at 3.75% fixed, an Edmonton buyer purchasing at the city’s $454,801 average price with 10% down faces a monthly payment of roughly $2,150 on a 25-year amortization. In Calgary, the higher $641,844 average pushes that to about $3,050 (WOWA, WOWA, 2026). Both remain significantly more manageable than the $4,000+ monthly payments common in Toronto and Vancouver.

Energy Sector Exposure

Alberta’s economy tracks oil prices more closely than other provinces. Rising oil prices tend to support provincial employment and housing demand but can also push inflation higher nationally — which means higher rates. It’s a double-edged sword for Alberta borrowers: stronger economy, but potentially higher borrowing costs.

Frequently Asked Questions

What’s the best mortgage rate in Alberta right now?

As of April 2026, the best 5-year fixed insured rate in Alberta is approximately 3.75%, and the best 5-year variable is around 3.30% — both available through the broker channel (Ratehub, April 2026). Big bank rates run 0.30-0.50% higher. Rates change daily, so contact a broker for your specific scenario.

Will mortgage rates go down in 2026 in Alberta?

The Bank of Canada’s policy rate may see one more 0.25% cut later in 2026 if the economy weakens, which would lower variable rates (RBC Economics, 2026). Fixed rates depend on bond yields, which have been rising — so fixed rates could stay flat or even increase in the near term.

Are Edmonton mortgage rates different from Calgary rates?

No. Canadian mortgage rates are set nationally by lenders, not regionally. An Edmonton buyer and a Calgary buyer with the same credit profile, down payment, and loan type will receive the same rate from the same lender. What differs between the two cities is home prices — Edmonton averages $454,801 versus Calgary’s $641,844 (WOWA, WOWA, 2026) — which affects your total borrowing cost.

Should I choose fixed or variable in 2026?

It depends on your risk tolerance and financial flexibility. Variable rates (around 3.30%) are lower than fixed (around 3.75%) and carry smaller early-break penalties. But variable rates move with every Bank of Canada decision. If you can handle potential payment increases and want lower penalties, variable may save you money. If you need payment certainty, fixed is the safer choice. See our fixed vs. variable comparison for the full analysis.

How much does a mortgage broker save on rates vs a bank?

On average, 0.30-0.50% on a 5-year fixed rate in early 2026 (Ratehub, April 2026). On a $450,000 mortgage, that translates to roughly $10,000 in interest savings over a 5-year term. Brokers are free to use — lenders pay their commission.

Ready to Find Your Best Alberta Mortgage Rate?

Every quarter-point counts on a mortgage. On a $450,000 loan, the difference between 4.19% at a big bank and 3.75% through a broker is over $10,000 in interest over five years. That’s not a rounding error — it’s a vacation, a renovation, or a year’s worth of property taxes.

At Metro Mortgage Group, we’ve been helping Edmonton and Alberta borrowers find the best rates for over 15 years. Our team of 7 brokers works with 30+ lenders to make sure you’re not leaving money on the table. With 229 five-star Google reviews, our clients consistently tell us the same thing: “I had no idea I was overpaying at my bank.”

Get started today:

– Call: 780-974-1270

– Email: info@MetroMortgageGroup.ca

– Apply online: metromortgagegroup.ca

More in the Rate Education Series

This guide is your hub. For deeper dives into specific rate topics, explore the full series:

- 5-Year Fixed Mortgage Rates in Alberta — Current rates, historical trends, and when fixed is the smart play

- Variable vs Fixed Mortgage — Side-by-side comparison with penalty math and break-even analysis

- When to Lock Your Mortgage Rate — Timing strategies for purchases and renewals

- How Rate Holds Work — Mechanics, hold periods, and extension tactics

- Prepayment Privileges Compared — Ranked comparison of lender prepayment terms across Canada

Nelson Sousa is the co-owner of Metro Mortgage Group Inc., an Edmonton-based mortgage brokerage founded in 2011. With over 15 years of experience in Alberta’s mortgage market, Nelson has helped thousands of borrowers navigate rate environments from record lows to the post-pandemic highs and back down again. He holds an active Alberta mortgage broker licence and contributes regular rate commentary for Metro’s clients and community. Reach Nelson at info@MetroMortgageGroup.ca or 780-974-1270.