Commercial Mortgages in Edmonton

Multi-family, construction, mixed-use, and refinance financing across Alberta

Edmonton’s commercial mortgage market moves on a completely different set of rails than residential — different lenders, different ratios, different documents, different timelines. In May 2026, a well-structured multi-family deal in Edmonton prices around 5.45% on a 5-year term through an A-bank, while a bridge loan on a vacant downtown retail building can run 9-11% through a private lender (Bank of Canada, 2026; CMLS Financial, 2026). After co-leading Metro Mortgage Group’s commercial division for years across Edmonton-area multi-family, retail, industrial, and mixed-use financing, I can tell you the gap between a good deal and a great one almost always comes down to how the file is packaged before it hits a lender’s desk.

This is the complete 2026 playbook for commercial mortgages in Edmonton — every major property type, every lender tier, every document a Canadian commercial lender will ask for.

Key Takeaways

– Edmonton commercial mortgage rates in May 2026 range from 5.45% on A-bank multi-family to 9-11% on private bridge, roughly 100-200 bps over residential equivalents (Bank of Canada, 2026).

– Down payments run 25-35% for multi-family (5+ units) and 35-50% for special-purpose assets like hotels, gas stations, and self-storage.

– Most Alberta commercial lenders require a Debt Service Coverage Ratio (DSCR) of 1.20-1.30+ on stabilized income properties.

– Amortizations typically cap at 20-25 years versus 25-30 for residential, with CMHC MLI Select pushing multi-family up to 50 years.

– Close timelines run 45-90 days on conventional, 10-21 days on private bridge.

What Is a Commercial Mortgage in Alberta?

A commercial mortgage in Alberta is any real estate loan where the underlying security is a property held for business or income-producing purposes rather than owner-occupied residential use (Government of Alberta, 2025). The CMHC and every major Canadian lender draw the line at five or more residential units — a fourplex is residential, a fiveplex is commercial, and that single-door difference changes everything about how the deal is financed.

In practical terms, commercial covers six major categories in the Edmonton market:

- Multi-family residential — apartment buildings, 5-unit up to 300+ unit complexes

- Retail — strip malls, standalone restaurants, service-retail on Jasper Ave, Whyte Ave, St. Albert Trail

- Office — downtown towers, suburban low-rise, medical and professional buildings

- Industrial — warehouses, flex space, manufacturing in west end and Nisku

- Mixed-use — ground-floor retail with apartments above, common along Edmonton’s main corridors

- Special purpose — hotels, gas stations, self-storage, car washes, daycares, restaurants

Each category has its own lender appetite, LTV cap, and underwriting template — see our multi-family mortgage guide for the 5+ unit financing details.

Citation capsule: CMHC and Canadian commercial lenders define commercial real estate as any property with 5+ residential units or any non-residential income-producing use, including retail, office, industrial, mixed-use, and special-purpose assets (Government of Alberta, 2025).

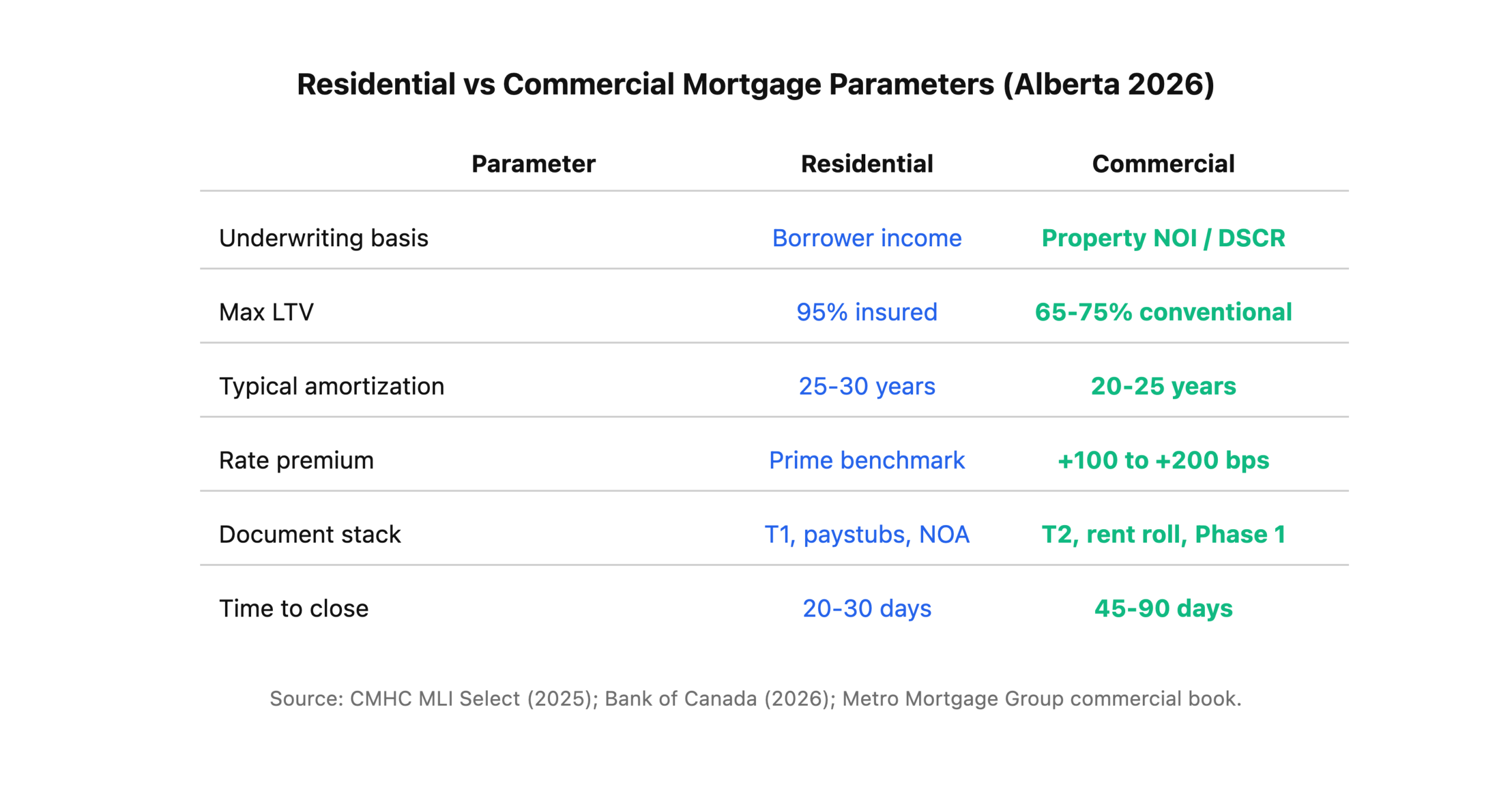

How Are Commercial Mortgages Different From Residential?

Commercial mortgages are underwritten on the property’s income, not the borrower’s paystub — and that single shift cascades through every other parameter of the deal (CMHC, 2025). A residential lender asks “can this person afford the payment?” A commercial lender asks “can this building afford the payment, even if the borrower disappears?”

Here’s how the major parameters compare side by side:

Commercial deals also carry personal guarantees on anything smaller than roughly $5M, environmental liability sits with the borrower, and default remedies move through a different track in the Alberta Court of King’s Bench. None of that should scare anyone off, but it does mean the file has to be right the first time.

What Property Types Qualify for Commercial Financing in Edmonton?

Roughly 85% of Edmonton commercial mortgage volume flows into four property types: multi-family, retail, office, and industrial, with multi-family alone representing more than 40% of all Alberta commercial originations in 2025 (CMLS Financial, 2026). Each type has its own Edmonton-specific lender appetite and pricing.

Multi-Family (5+ Units)

The deepest, most competitive commercial market in Edmonton. Every A-bank, credit union, CMHC MLI Select lender, and most MICs will quote on a clean multi-family deal. Hot submarkets: Oliver, Garneau, Strathearn, Bonnie Doon, and the north-central rental corridor along 97 Street. Cap rates in 2026 run 5.25-6.25% on stabilized assets (Avison Young, 2026).

Retail and Mixed-Use

Strong lender appetite on grocery-anchored, pharmacy-anchored, or daycare-anchored retail. Softer appetite on unanchored strip malls and tertiary-location standalone. Jasper Ave and Whyte Ave mixed-use remains a preferred asset class for Alberta credit unions.

Office

The toughest segment in 2026. Post-hybrid-work vacancy in downtown Edmonton Class B office still sits above 18% per Q1 2026 broker reports, and A-bank appetite is thin. Most office deals above 30% vacancy route to credit unions or MICs at meaningfully higher rates (CBRE, 2026).

Industrial

Warehouse and flex space in Nisku, Acheson, and Edmonton’s west end remain the most lender-favoured asset class in Alberta. Vacancy is sub-4%, rental growth has averaged 6-8% annually since 2022, and A-banks routinely stretch to 70% LTV on clean industrial (CBRE, 2026).

Special Purpose

Hotels, gas stations, car washes, self-storage, daycares, restaurants. Financeable, but nearly always through a specialist lender or private MIC, with 35-50% down and a premium of another 100-150 bps over standard commercial.

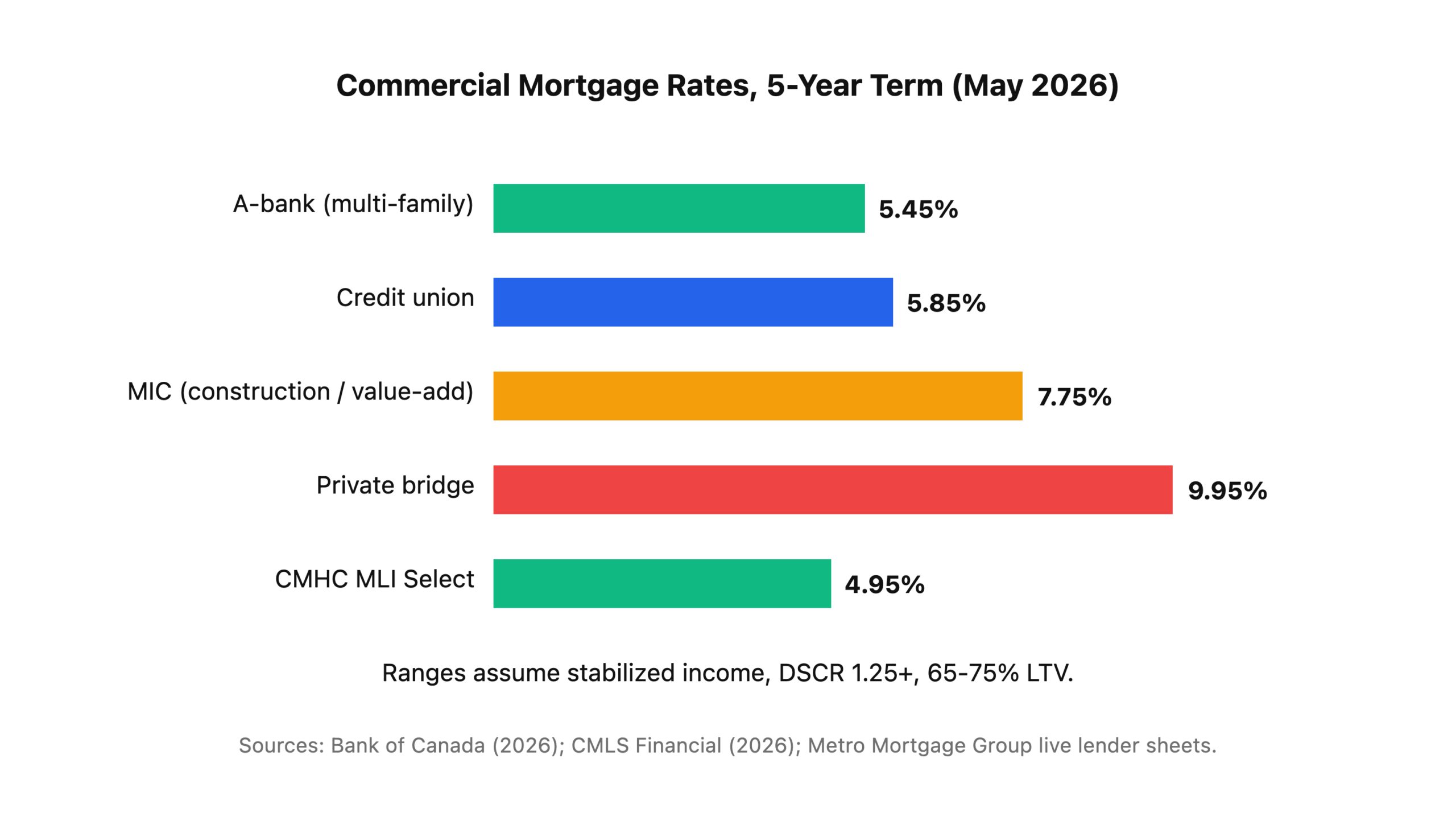

What Are 2026 Commercial Mortgage Rates in Alberta?

Edmonton commercial mortgage rates in May 2026 range from 5.45% for A-bank multi-family on a 5-year fixed to 9.00-11.00% for private bridge financing on transitional assets, with the Bank of Canada’s overnight rate holding at 2.25% since the June 10, 2026 announcement, with the next scheduled decision on July 15, 2026 (Bank of Canada, 2026). The all-in rate on any given file depends far more on lender tier, asset quality, and DSCR than on the headline BoC number.

Indicative May 2026 pricing by lender tier:

The CMHC MLI Select program remains the single best-priced commercial money in Canada for multi-family borrowers who can hit the energy, accessibility, or affordability thresholds — sometimes printing rates 50-100 bps inside a conventional A-bank quote. It’s also the most paperwork-intensive. We’ll walk any client through whether MLI Select is worth the extra 60-90 days.

For the latest residential benchmark context, see our current rate benchmarks.

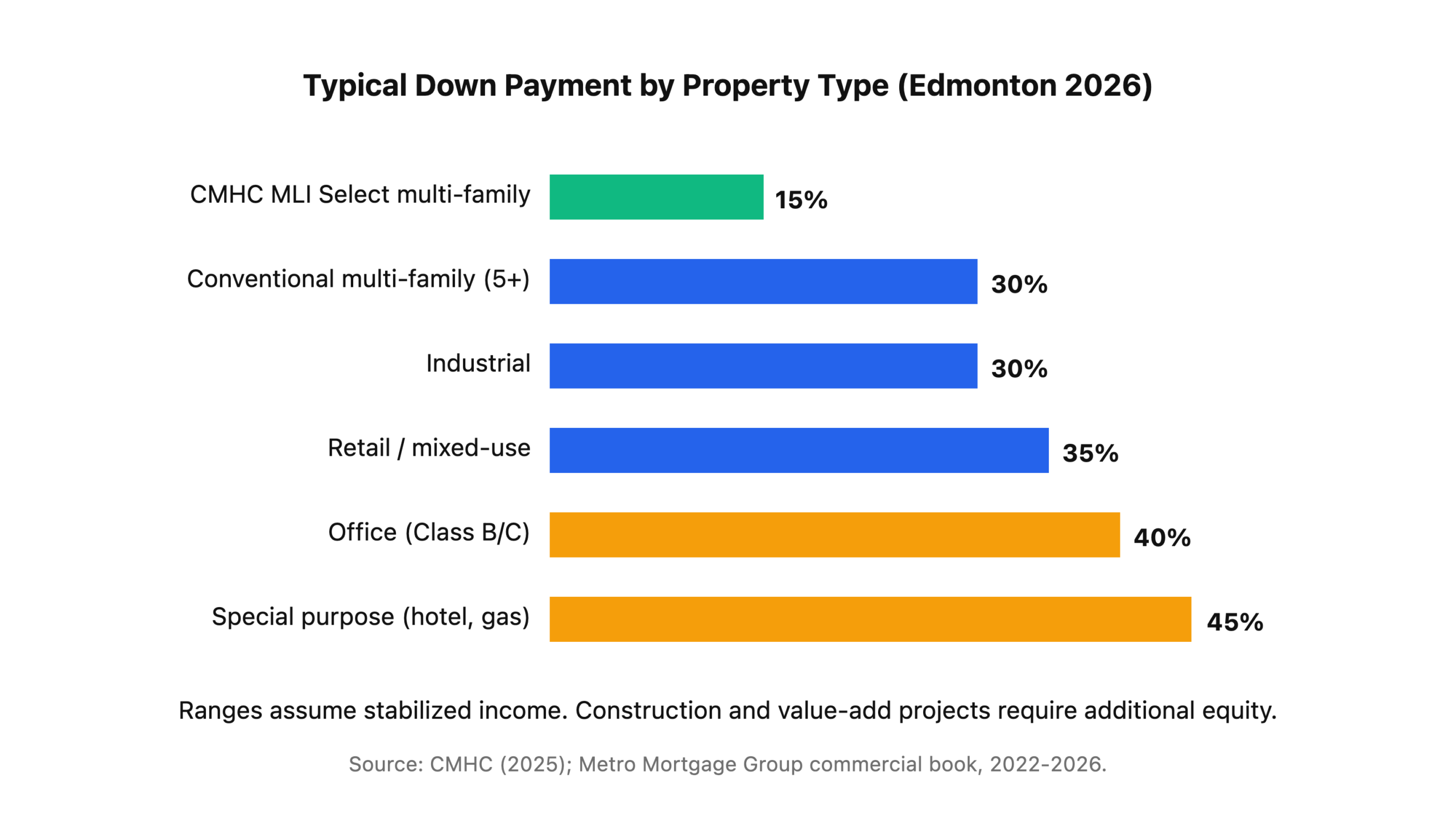

How Much Down Payment Is Required for Commercial in Edmonton?

Commercial down payments in Edmonton range from 15% on CMHC MLI Select multi-family at the absolute low end, to 50% or more on special-purpose assets like gas stations or rural hotels (CMHC, 2025). Conventional multi-family (uninsured) runs 25-35% down, retail and office 30-40%, industrial 25-35%.

Typical equity requirements by asset type:

Down payment on a commercial deal has to be real equity — not borrowed, not a VTB wrapping the entire stack, not a second charge behind the purchase. Lenders will verify source of funds 90 days back the same way residential underwriting does, and on larger deals they’ll want to see your full corporate net worth statement, not just the purchase-specific equity. The cleanest commercial files I’ve placed in 2026 had the equity sitting in a separate corporate account for 60+ days before submission.

What Lenders Fund Commercial Mortgages in Alberta?

Alberta’s commercial lender universe breaks into four distinct tiers, and a good broker will shop a file across at least two tiers to force a fair price (CMLS Financial, 2026). In 2025, Alberta commercial originations were dominated by A-banks (roughly 55% of volume), followed by credit unions (20%), CMHC-insured (15%), and alternative/private lenders (10%).

Tier 1: A-Banks (Schedule I)

The big six plus a few smaller charter banks. ATB Financial is the dominant Alberta player. Scotiabank, RBC, BMO, TD, CIBC, and National Bank all have Edmonton commercial teams. Best pricing, tightest credit box, longest timelines. Prefer multi-family, industrial, and grocery-anchored retail.

Tier 2: Credit Unions

Servus Credit Union is the Alberta heavyweight, with Canadian Western Bank (CWB) sitting alongside the credit union tier for most commercial purposes. Credit unions often win on files the A-banks won’t touch (slightly older buildings, Class B retail, borrowers without perfect corporate history) and price 20-50 bps wider than A-banks.

Tier 3: MICs and Non-Bank Lenders

Mortgage Investment Corporations like Romspen, Trez Capital, CMLS Financial, First National (on the non-bank conventional side), Peoples Trust, and dozens of regional players. Preferred for construction, value-add, bridge, and mid-market deals under $20M. Rates typically 7.00-9.50%.

Tier 4: Private Lenders

Short-term bridge, VTB structures, land-and-hold, distressed acquisitions. Rates 9-13%, terms 6-18 months, fees 1-3 points. Expensive, but they close in 10-21 days when a deal needs to move. On a number of Metro commercial files, we’ll use a private lender as a bridge specifically to hit a seller’s deadline, then refinance to an A-bank at month 6-9 once the building is stabilized.

What Documents Do You Need to Apply?

A complete commercial mortgage application package runs 25-50 documents across borrower, property, and corporate disclosure — roughly 5x the paperwork of a standard residential deal (CMHC, 2025). The right documents at submission make the difference between a 45-day close and a 90-day slog.

Borrower and Corporate Documents

- T1 Generals for each guarantor, 2 most recent years

- Notice of Assessment for each guarantor, 2 most recent years

- T2 corporate tax returns for the borrowing entity, 2 years minimum

- Year-end financial statements (Notice to Reader minimum, Review-engagement preferred)

- Personal Net Worth Statement for each guarantor

- Corporate structure chart and articles of incorporation

- Certificate of Incumbency or director resolutions

Property-Level Documents

- Current rent roll with tenant names, unit numbers, rents, lease start/end dates, deposits

- T776 Statement of Real Estate Rentals for the subject property, 2 years (if held in personal name)

- Trailing 12-month operating statements (T12) and 3 years of historical ops

- Signed purchase and sale agreement

- Current lease copies for all commercial tenants

- Property tax bill (most recent)

- Utility bills (12 months)

- Insurance certificate

- Appraisal (AACI-designated, commissioned by the lender)

- Phase 1 Environmental Site Assessment (required by nearly all lenders on any commercial or mixed-use deal)

- Building Condition Assessment / Property Condition Report

- Zoning confirmation letter

- Title search and existing mortgage payout statement

The single most common document gap on Edmonton commercial files in 2026 is the Phase 1 ESA. Sellers often don’t have one, and buyers assume their lawyer will handle it. By the time anyone orders one (7-14 days lead time, $2,500-$4,500), the financing condition window is half gone. Order the Phase 1 the day after you have a signed PSA.

How Does Loan-to-Value (LTV) Work on Edmonton Commercial?

LTV on an Edmonton commercial deal is the lesser of purchase price or appraised value, and lenders will almost always lean on the lower of the two numbers if there’s any daylight between them (CMHC, 2025). Typical maximums: 75% on CMHC-insured multi-family, 65-75% on conventional multi-family, 65-70% on retail and industrial, 60-65% on office, and 50-65% on special purpose.

But LTV is only half the story. Every commercial lender will also run a Debt Service Coverage Ratio (DSCR) test, and most deals are DSCR-constrained rather than LTV-constrained. DSCR is calculated as:

DSCR = Net Operating Income / Annual Debt Service

Most Alberta commercial lenders require a minimum DSCR of 1.20 on multi-family and 1.25-1.30 on commercial-commercial (retail, office, industrial). On a deal where the building only throws off enough NOI to hit 1.20 at 60% LTV, you don’t get 70% LTV no matter what the appraisal says. That’s the part newer commercial investors miss most often.

Worked Example: $5M Edmonton 24-Unit Apartment

- Purchase price: $5,000,000

- Appraised value: $5,050,000

- Annual gross rent: $420,000

- Operating expenses (35%): $147,000

- Net Operating Income: $273,000

- Target DSCR: 1.25

- Maximum debt service: $273,000 / 1.25 = $218,400/year

- At 5.75% rate, 25-year amortization, that supports roughly $3.1M in debt

- Result: 62% LTV constrained by DSCR, not 75% LTV allowed by policy

On this deal, the borrower needs $1.9M in equity (38%) to get the maximum debt the building can service, even though the lender would theoretically lend to 75%.

How Long Does a Commercial Mortgage Take to Close?

Conventional commercial mortgages in Alberta typically close in 45-90 days from signed purchase agreement to funding, with CMHC MLI Select deals running 90-150 days and private bridge deals closing in as little as 10-21 days (CMHC, 2025). Every timeline assumes the document package is complete at submission, which it almost never is.

A realistic Edmonton conventional commercial timeline:

- Week 1-2: PSA signed, broker engagement, initial term sheet from 2-3 lenders

- Week 2-4: Lender selection, commitment letter issued subject to conditions

- Week 3-6: Appraisal ordered and delivered (2-4 week turnaround in Alberta)

- Week 4-7: Phase 1 ESA ordered and delivered

- Week 5-8: Building Condition Assessment, legal docs drafted

- Week 8-10: Conditions cleared, instructions to lawyer, funding

Negotiate a minimum 60-day financing condition on any Edmonton commercial deal under $10M. Ninety days is safer. I’ve watched too many buyers sign 30-day conditions because they’re used to residential timelines, then burn their deposit when the appraisal slips.

When Should You Use a Broker vs Going Direct?

In Metro’s experience, brokered commercial deals in Canada tend to print tighter on rate and higher on leverage versus direct-to-bank placements, on average across stabilized income deals. The savings are meaningful on anything above roughly $2M in loan size, and the structuring advantage is meaningful at any size.

Go Direct When

- You already have a deep, multi-year relationship with a specific commercial banker at ATB, Servus, or CWB

- Your deal is small (under $1.5M) and straightforward multi-family

- You want to keep all banking (operating, deposits, mortgage) under one roof

Use a Broker When

- You want to compare at least 3 lenders across tiers

- The deal is above $2M or has any complexity (value-add, mixed-use, non-standard guarantor, non-resident)

- You need to hit a tight closing deadline and want parallel underwriting

- You’re buying a property type where lender appetite varies wildly (office, special purpose, hospitality)

- You want to preserve your direct banker relationship for your next deal

In Metro’s experience, broker-negotiated commercial files consistently land a lower all-in rate and higher achievable leverage than client-reported direct quotes on the same type of deal — often enough interest savings over a 5-year term to justify the extra step of shopping the file.

To understand how personal credit affects a mortgage, see how it factors into commercial guarantor strength as well.

Frequently Asked Questions

What is the minimum commercial mortgage size in Edmonton?

Most Alberta A-banks set a soft floor at $500,000-$750,000 for commercial mortgages, with credit unions going as low as $250,000 on owner-occupied small-bay industrial or small multi-family (CMLS Financial, 2026). Below $250K, the deal usually gets routed to a residential investment product (for 1-4 unit rentals) or a small-business loan secured by real estate.

Can I get a commercial mortgage with bad personal credit?

Yes, but it changes which tier of lender will look at the file. A-banks typically want guarantors above 680 Beacon, credit unions will work to 640, and MIC/private lenders will lend on credit as low as 550-600 if the property and equity cover the risk (CMHC, 2025). Expect a 100-200 bps rate premium for sub-680 credit.

Do I need to incorporate to get a commercial mortgage in Alberta?

Not always. Residential-commercial properties (5-8 units) are routinely financed in personal name using T776 income. On anything above 10 units, or any non-residential commercial, nearly every Alberta lender will require a single-purpose corporation (SPC) as the borrower, with personal guarantees from the shareholders (Government of Alberta, 2025). Set the SPC up before you submit.

What is DSCR and why do lenders care?

DSCR (Debt Service Coverage Ratio) measures how many times the building’s net operating income covers its annual mortgage payment. A DSCR of 1.25 means the building generates $1.25 of NOI for every $1 of debt service, leaving a 25% cushion (CMHC, 2025). Alberta commercial lenders require minimum DSCR of 1.20-1.30+, and the DSCR test often caps leverage well below the LTV ceiling.

Are commercial mortgage rates fixed or variable in Canada?

Both, but the Canadian commercial market overwhelmingly prefers 5-year fixed. In Metro’s own Alberta commercial pipeline, the large majority of files close on 5-year fixed terms, with the balance split between 3-year fixed, variable, 10-year fixed, or bridge structures. Variable pricing currently sits at Prime + 50 to 125 bps depending on asset and borrower strength.

How much does a commercial appraisal cost in Edmonton?

An AACI-designated commercial appraisal on a standard Edmonton income property typically runs $3,500-$7,500 depending on asset type and complexity (CMLS Financial, 2026). Hotels, self-storage, and special-purpose assets can run $10,000-$15,000. The borrower pays regardless of whether the deal funds, and the appraisal must be commissioned by the lender, not the borrower, to be acceptable.

Ready to Structure Your Edmonton Commercial Deal?

Every commercial mortgage in Edmonton lives or dies on how the file is packaged before it ever reaches a lender. Metro Mortgage Group’s commercial team places significant Edmonton-area commercial funding every year across multi-family, retail, industrial, and mixed-use. I personally underwrite every commercial file that comes through the door. Call 780-974-1270 or email info@MetroMortgageGroup.ca to book a no-cost commercial strategy call.

For adjacent reading, start with the complete first-time home buyer guide for personal residential context, or read our current rate benchmarks for current pricing. If you’re specifically buying a 5+ unit apartment building, our multi-family mortgage Edmonton guide goes deeper on CMHC MLI Select. To understand how your personal credit affects guarantor strength, see how credit scores affect Alberta mortgages.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and co-leads the firm’s commercial division, specializing in multi-family, retail, and mixed-use financing across Edmonton, Calgary, and greater Alberta. Metro Mortgage Group has served Alberta since 2011 with 229 five-star Google reviews.

Last updated: May 18, 2026