Closing Costs in Alberta: 2026 Breakdown

Land transfer, legal, inspection, and adjustment costs for Alberta buyers

On Edmonton’s $470,819 March 2026 average home, total closing costs land around $4,700 — dramatically lower than the $14,000+ an Ontario buyer pays on the same home in Toronto (Government of Alberta, 2024; REALTORS Association of Edmonton, 2026). Alberta’s zero land transfer tax is the single largest cost advantage first-time buyers have anywhere in Canada. It saves the average Edmonton buyer the equivalent of a used car at the closing table.

Here’s every closing cost line item you’ll face buying a home in Alberta in 2026, with exact 2026 numbers, real Edmonton examples, and the total budget you should actually plan for.

Key Takeaways

– Total Alberta closing costs run $3,500-$5,500 on a typical Edmonton home — roughly 1-2% of purchase price (Government of Alberta, 2024).

– Alberta has zero land transfer tax — only Land Titles Office registration fees of $50 + $5/$5,000 of value for transfer and mortgage.

– An Edmonton buyer saves $7,000-$12,000 at closing versus Toronto or Vancouver on the same purchase price.

– Budget for closing costs the day you start saving for your down payment — not the week before possession.

How Much Are Closing Costs in Alberta in 2026?

Total closing costs in Alberta typically run 1% to 2% of the purchase price as a general Alberta market estimate — roughly $3,500 to $5,500 on an average Edmonton home in the $400K-$500K range. That’s dramatically lower than Ontario’s 4% or BC’s 3% on comparable properties, thanks to Alberta’s zero land transfer tax policy.

Here’s the line-by-line breakdown for a typical $470,000 Edmonton home with a $447,000 insured mortgage:

Alberta’s closing cost structure is the cheapest in Canada for one reason: no land transfer tax. Ontario, BC, and most other provinces charge a percentage-based land transfer tax that scales with the home price. Alberta charges only flat Land Titles Office registration fees — a structural advantage that dates back to the 1970s and has never been revoked despite multiple provincial budget pressures.

What Are Alberta Land Titles Office Fees in 2026?

Alberta Land Titles Office (LTO) fees were updated on October 20, 2024, doubling the variable rate from $2 per $5,000 to $5 per $5,000 for both title transfers and mortgage registrations (Government of Alberta, 2024). The new fee structure looks like this:

- Title transfer — $50 base + $5 per $5,000 of purchase price

- Mortgage registration — $50 base + $5 per $5,000 of mortgage principal

Run the math on a $470,000 Edmonton home with a $447,000 mortgage:

- Title transfer = $50 + ($470,000 ÷ $5,000 × $5) = $520

- Mortgage registration = $50 + ($447,000 ÷ $5,000 × $5) = $497

- Total LTO fees = $1,017

For a cleaner round number, most Alberta real estate lawyers quote approximately $970-$1,020 in LTO fees on a typical Edmonton transaction. That’s it. No hidden land transfer tax, no percentage-based surcharge, no municipal land transfer tax like Toronto has.

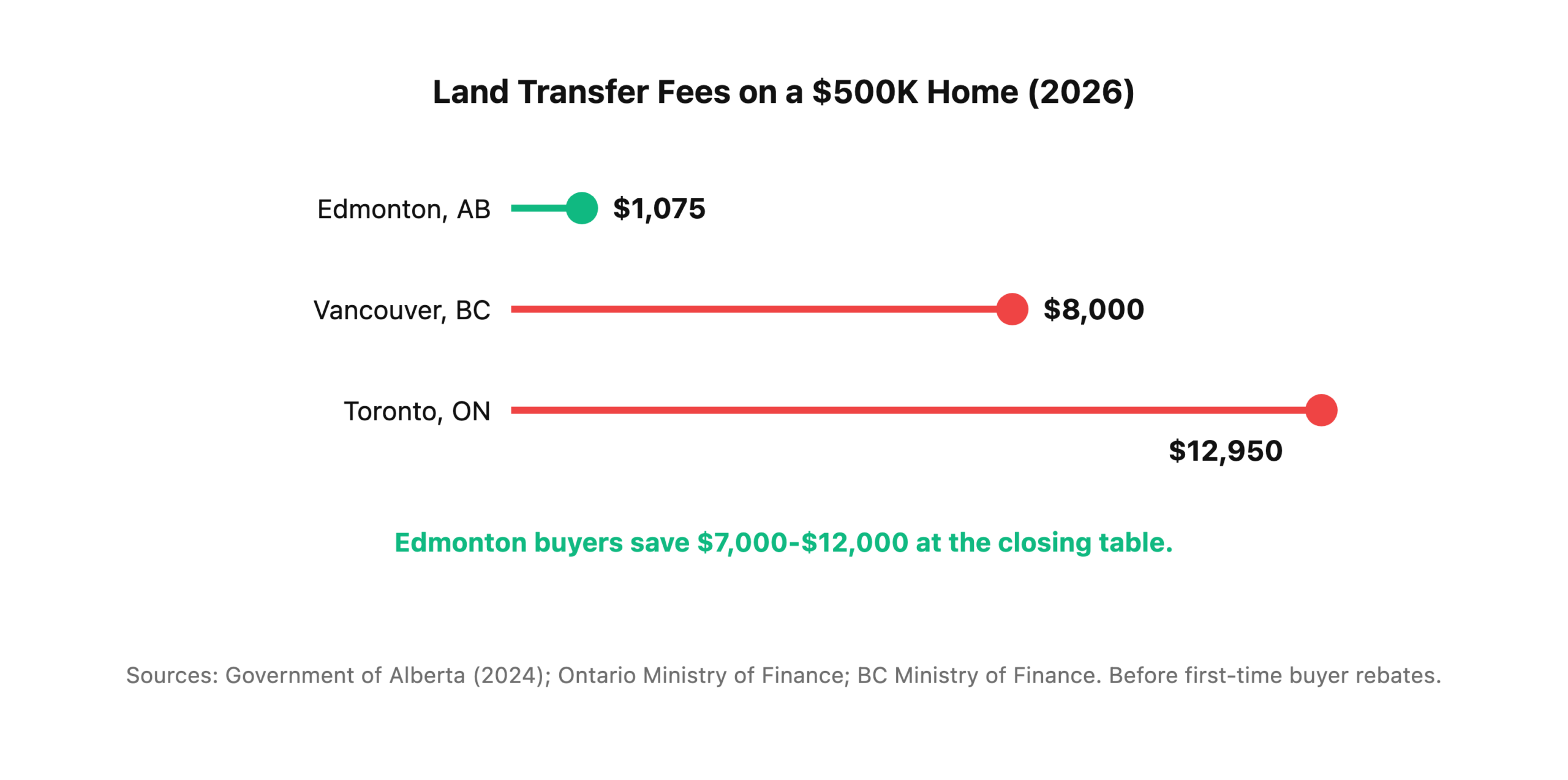

How This Compares to Other Canadian Cities

On an identical $500,000 home purchase:

Even after applying first-time buyer rebates in Ontario and BC, Alberta still comes out $4,000-$8,000 cheaper at the closing table. And Alberta gives this advantage to every buyer, not just first-timers.

What Other Closing Costs Should Alberta Buyers Plan For?

Beyond the Land Titles fees, Alberta buyers need to budget for six additional closing cost categories that typically total $2,500-$4,500 on a standard Edmonton transaction, based on typical Alberta market estimates. These are the same categories buyers face everywhere in Canada, but the amounts in Alberta are generally middle-of-pack compared to other provinces.

1. Legal Fees ($1,000-$1,800)

Every Alberta real estate purchase requires a licensed real estate lawyer to handle the closing. Legal fees on a standard Edmonton purchase typically run $1,000-$1,800 including disbursements. That covers title search, document preparation, registration at the Land Titles Office, trust account handling, and closing-day coordination with the seller’s lawyer and your lender.

Don’t choose a lawyer on price alone. The cheapest $800 flat-fee lawyer in Edmonton will often delay your closing by 2-3 days because they’re overbooked. Pay the $1,400-$1,600 for a reputable firm and you’ll close on time.

2. Home Inspection ($450-$700)

A certified home inspection on a typical Edmonton home costs $450-$700 depending on square footage and property age. For older homes in mature neighborhoods like Westmount, Bonnie Doon, or Riverdale, expect to pay the higher end because the inspector has more systems to check. Never skip this, regardless of what listing agents tell you in hot markets.

3. Title Insurance ($250-$350)

Title insurance is a one-time premium paid at closing that protects you against unknown defects in the title (forged documents, undiscovered liens, etc.). Most Alberta real estate lawyers bundle title insurance into their closing package and quote $250-$350 on a standard purchase. Worth every dollar.

4. Property Tax Adjustments ($500-$1,500)

If the seller has already paid the property tax for the year, you’ll reimburse them for the portion of the year after your possession date. On a $470K Edmonton home with typical annual property tax of $3,500-$4,000, if you close in May, you’ll owe the seller roughly $2,300-$2,600 in prorated tax. If you close in November, you might be refunded $500-$700 from the seller’s prior year prepayment. Timing matters.

5. Home Insurance Binder ($100-$150)

Your lender requires home insurance in effect on possession day. Most Alberta insurers collect the first monthly premium (~$100-$150) at the start of the policy. Don’t forget to shop for home insurance 2-3 weeks before closing — your lender will ask for the binder 5 days before funding.

6. Appraisal Fee ($400-$600, Often Waived)

On standard insured mortgages, your lender may order a third-party appraisal to confirm the home’s market value. Appraisals typically cost $400-$600, but on most insured deals under $1M the lender waives this fee or absorbs it. On uninsured or higher-value mortgages, the buyer pays.

Closing Cost Examples for Different Edmonton Price Points

Here’s what total closing costs look like at three common Edmonton purchase prices, informed by 500+ first-time buyer files Metro Mortgage Group has closed since 2010. These are grounded in real Alberta transaction patterns, not theoretical estimates.

Example 1: $320,000 Edmonton Condo

- Legal fees: $1,200

- LTO fees: $390 (title) + $365 (mortgage) = $755

- Property tax adjustment: $400

- Home inspection: $500

- Title insurance: $275

- Insurance binder: $100

- Total: ~$3,230 (about 1.01% of purchase price)

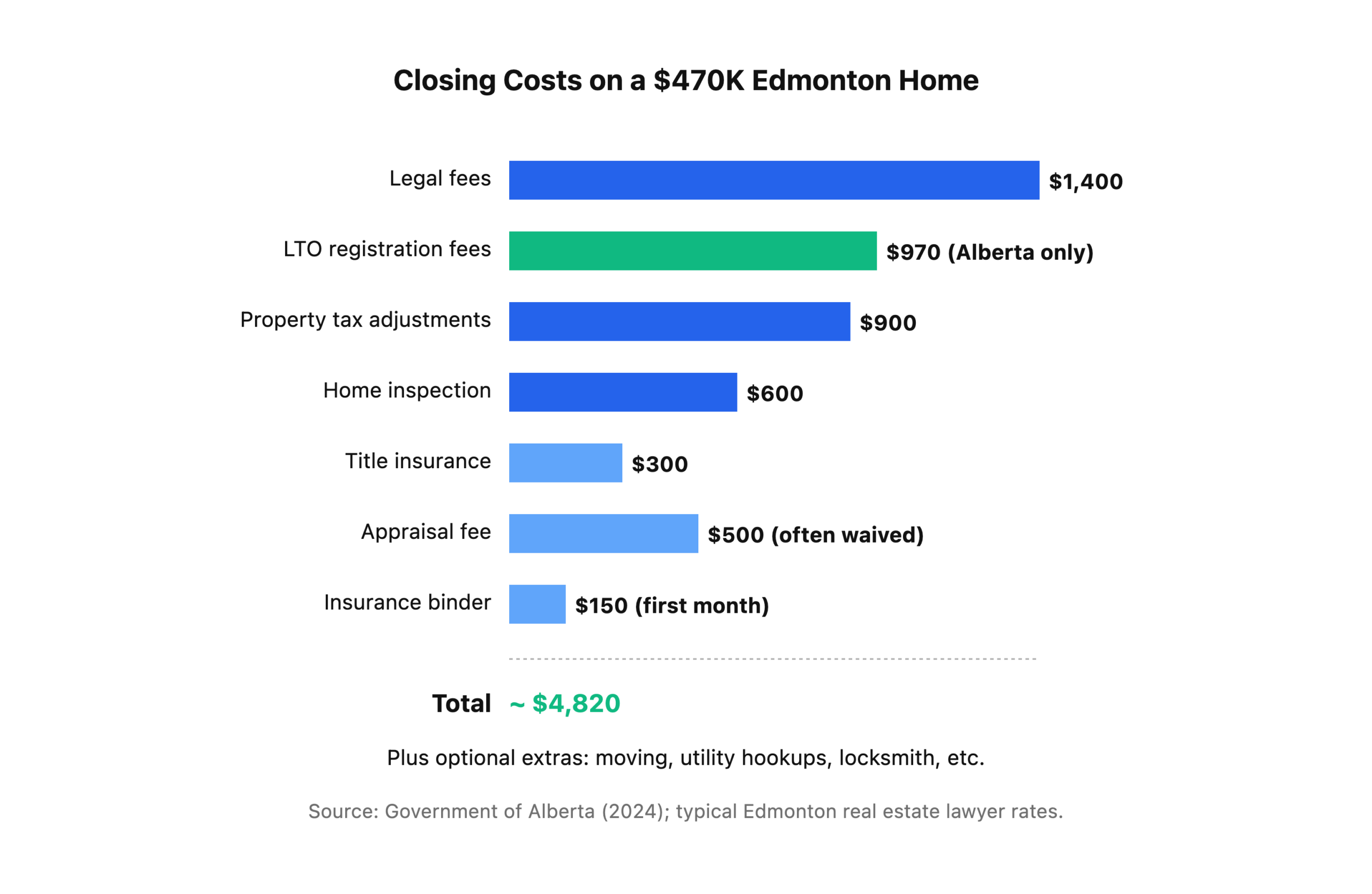

Example 2: $470,000 Edmonton Starter Detached

- Legal fees: $1,400

- LTO fees: $520 (title) + $497 (mortgage) = $1,017

- Property tax adjustment: $900

- Home inspection: $600

- Title insurance: $300

- Insurance binder: $125

- Total: ~$4,342 (about 0.92% of purchase price)

Example 3: $650,000 Edmonton Established Detached

- Legal fees: $1,600

- LTO fees: $700 (title) + $667 (mortgage) = $1,367

- Property tax adjustment: $1,400

- Home inspection: $700

- Title insurance: $350

- Insurance binder: $150

- Appraisal fee: $500

- Total: ~$6,067 (about 0.93% of purchase price)

Notice the pattern: Alberta closing costs stay remarkably flat as a percentage of purchase price — roughly 0.9-1.0% across the entire first-time buyer range. That’s a much more predictable number than Ontario or BC, where closing costs scale dramatically with land transfer tax tiers.

When Do You Actually Pay Closing Costs?

Most Alberta closing costs come due on or immediately before possession day — the day you get the keys and title transfers into your name (Government of Alberta, 2024). Your real estate lawyer will send you a Statement of Adjustments about 5-7 days before possession showing every line item and the exact amount you need to wire to their trust account.

The payment timeline looks like this:

- 2-3 weeks before closing — Home inspection fee paid directly to the inspector

- 5-7 days before closing — Statement of Adjustments arrives from lawyer; home insurance binder issued

- 1-3 days before closing — You wire the closing cost balance to your lawyer’s trust account

- Possession day — Lawyer disburses funds; you get the keys

Most first-time buyers underestimate how much cash they need on possession day. In addition to the closing costs listed above, you also need your down payment in the lawyer’s trust account, minus any deposit already held by the listing brokerage. On a $470K home with 5% down, that’s roughly $23,500 down payment + $4,700 closing costs = $28,200 total cash required on or before possession day.

Frequently Asked Questions

Does Alberta charge a land transfer tax?

No. Alberta is one of only a few Canadian provinces with zero land transfer tax, charging only flat Land Titles Office registration fees of $50 + $5 per $5,000 of value (Government of Alberta, 2024). On a typical Edmonton home, LTO fees total about $970-$1,020 — compared to $12,950+ in Toronto on the same purchase price.

Can I add closing costs to my mortgage?

Generally no — closing costs must be paid in cash on or before possession day, separate from your down payment (CMHC, 2025). The one exception is CMHC mortgage default insurance, which can be rolled into your mortgage balance. Standard closing costs (legal, inspection, etc.) cannot.

How much should I budget for closing costs on my first Alberta home?

Budget $5,000 as a safe round number for most first-time Alberta buyers, or use the 1-2% of purchase price rule of thumb as a general Alberta market estimate. On a $400K home that’s $4,000-$8,000; on a $600K home that’s $6,000-$12,000. Err on the high side so you arrive at possession day with cash to spare.

What if I can’t afford both the down payment and closing costs?

The simplest fix is to reduce your down payment target slightly (staying above the 5% minimum) and keep the difference as closing cost reserve (Financial Consumer Agency of Canada, 2025). On a $470K home, the difference between 5% and 6% down payment is $4,700 — which happens to be your exact closing cost budget. It’s a clean trade-off.

Are there any first-time buyer closing cost rebates in Alberta?

Alberta itself has no first-time buyer closing cost rebate — because it already has no land transfer tax to rebate from. The federal First-Time Home Buyers’ Tax Credit of up to $1,500 can be claimed on your income tax return in the year you buy, which effectively offsets a meaningful portion of your Alberta closing costs (Canada Revenue Agency, 2026).

Ready to Plan Your Total Alberta Closing Budget?

The biggest budgeting mistake first-time Alberta buyers make is treating closing costs as an afterthought. Build the $3,500-$5,500 buffer into your savings target from day one — not week one before possession. Metro’s first-time buyer team runs full budget scenarios for Edmonton and Calgary clients every week, free of charge. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full first-time buyer playbook, start with our complete Edmonton first-time home buyer guide. To plan your down payment side of the equation, read how much down payment you actually need in Alberta.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 20, 2026