5 First-Time Homebuyer Mistakes We See Every Month in Edmonton

After 500+ first-time closings across Edmonton, Calgary, and greater Alberta, the same five mistakes show up every single month — and four of them cost buyers five figures or more ([Metro Mortgage Group closing data, 2025-2026]). If you recognize yourself in any of these, the good news is every one of them is fixable. The bad news? They’ll also sink your deal or your budget if you don’t catch them before closing day.

Here’s the full list, ranked by how often we see them and how expensive they get when buyers don’t catch them in time.

Key Takeaways

– Shopping for a home before pre-approval wastes 4-8 weeks and roughly 1 in 3 Edmonton first-time buyers fall into this trap ([Metro Mortgage Group closing data, 2025-2026]).

– Forgetting closing costs means arriving $3,500-$5,500 short on possession day (Government of Alberta, 2024).

– Taking the first bank rate offered costs the average Edmonton buyer $4,800 over a 5-year term on a $400K mortgage (WOWA, 2026).

– Skipping the home inspection to win a bidding war has cost Metro clients up to $22,000 in surprise repairs within the first year.

Mistake #1: Shopping for a Home Before Getting Pre-Approved

How often we see it: About 1 in 3 Edmonton first-time buyers who first contact us. What it costs: 4-8 weeks of wasted time plus emotional damage from losing houses to better-prepared buyers.

Every week we meet buyers who fell in love with a place in Terwillegar or Summerside only to find out their real stress-tested budget was $40,000-$80,000 short of the list price. The fix is embarrassingly easy: a broker pre-approval takes 48 hours, costs nothing, and gives you a rock-solid shopping ceiling. Always do this first. Every realtor in Edmonton will ask for it before they show you a property anyway.

How to Avoid It

- Get a broker pre-approval at least 60-90 days before you start shopping

- Ask for your exact stress-tested maximum, not just a “comfortable” number

- Keep the pre-approval document on your phone — listing agents will ask for it

- Re-check your numbers monthly; Bank of Canada rate changes shift your ceiling

On Edmonton’s $470,819 March 2026 average home, the stress-tested income requirement is roughly $90,000-$100,000 household depending on other debts (REALTORS Association of Edmonton, 2026). Knowing that number before you shop prevents 90% of first-timer disappointment.

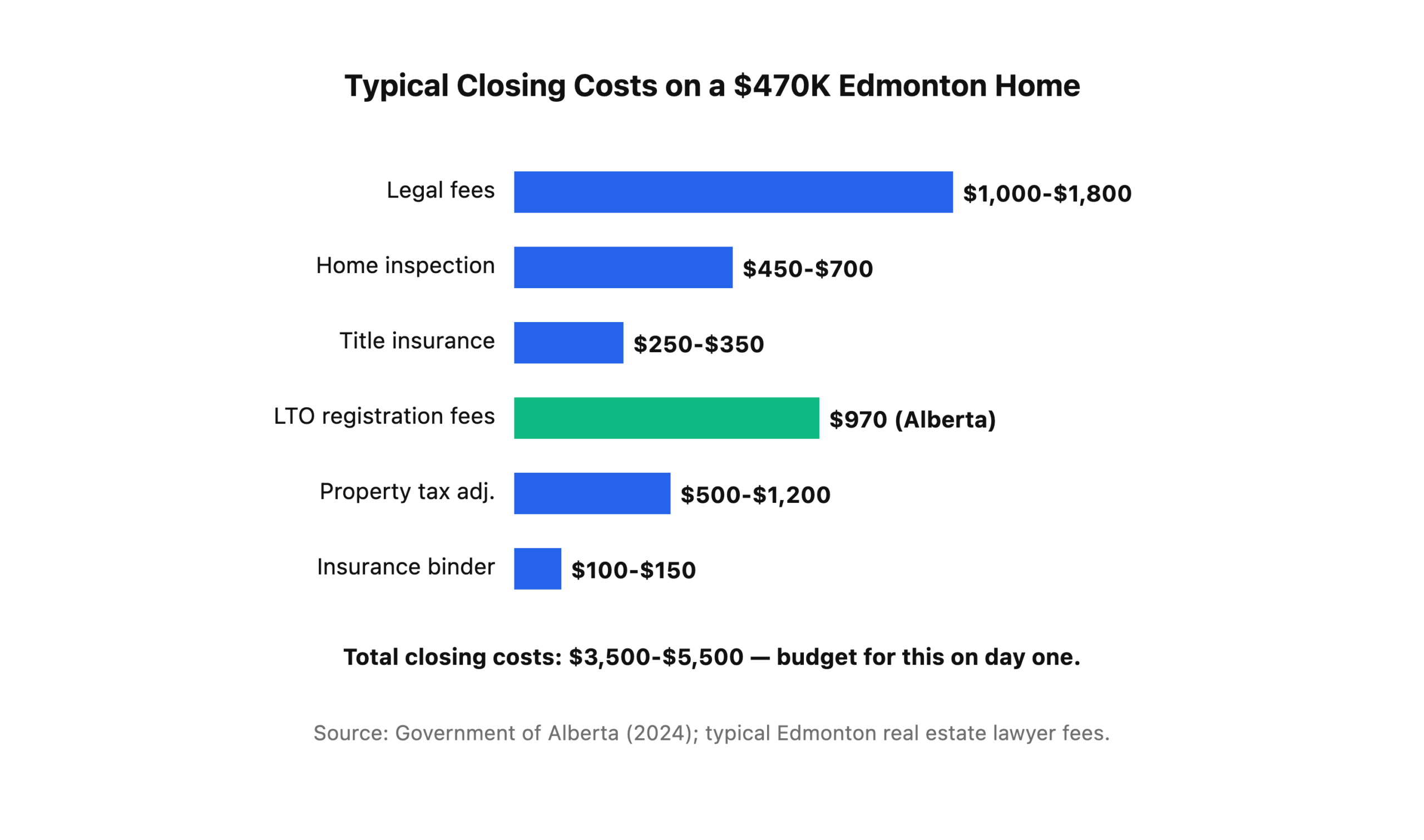

Mistake #2: Forgetting the Full Closing Cost Budget

How often we see it: About 1 in 4 first-time buyers. What it costs: $3,500-$5,500 in unplanned cash needed on possession day.

Alberta first-time buyers obsess over the down payment and forget that closing costs are a completely separate line item. On Edmonton’s average $470,819 home, you need roughly $23,500 in down payment plus $3,500-$5,500 for closing costs — legal fees, home inspection, title insurance, property tax adjustments, and the first month of home insurance (Government of Alberta, 2024). Land Titles Office fees in Alberta are small ($970 on a typical Edmonton home), but the rest adds up fast.

How to Avoid It

Add $5,000 to your savings target on day one of the home buying journey. Don’t touch it. That’s your closing cost buffer. Buyers who treat the down payment and closing costs as one combined target almost always end up scrambling.

Mistake #3: Switching Jobs or Taking On Debt Mid-Deal

How often we see it: Roughly 1 in 8 buyers. What it costs: A sunk deal, lost deposit, and the emotional damage of losing the house.

Your lender re-verifies your employment and debt load the week of closing — not just at the initial pre-approval. Any of the following can sink a tight pre-approval between offer and possession:

- A new car payment (even $400/month can blow your debt-service ratio)

- Switching employers, even for a better-paying job (lenders want 90 days in your current role)

- Taking on any new credit — furniture financing, a credit line, a new credit card

- Co-signing a loan for a family member

- A large unexplained deposit into your account (triggers AML review)

We had a Metro client last fall lose a $520K Edmonton detached deal at the final funding stage because she traded in her 2018 Civic for a new 2025 CR-V two weeks before possession. The $560/month car payment pushed her total debt service ratio above 44%, and the lender pulled the funding. She lost her deposit and the house. The CR-V could have waited six weeks.

How to Avoid It

From the day you sign your offer to the morning after possession day, don’t change anything financial. No new debt, no new jobs, no big purchases, no transfers between accounts. Your lender is watching your file the whole time — and they will check again 48 hours before funding.

Mistake #4: Taking the First Rate Your Bank Offers

How often we see it: About 1 in 2 buyers who came to us after talking to their own bank first. What it costs: $4,800 on average over a 5-year term on a $400,000 mortgage.

Here’s the math that every first-time Alberta buyer needs to understand. The best 5-year fixed insured rate in Canada as of April 2026 sits around 3.75% (WOWA, 2026). Your bank’s posted rate on the same product is typically around 4.29% — a 54 bps gap. On a $400,000 mortgage amortized over 30 years, that 0.54% difference works out to:

- ~$120/month in extra payment

- ~$7,200 in extra payments over a 5-year term

- ~$29,000 over the full 30-year amortization

Your bank will negotiate down if you push them. But “negotiating down” usually means they’ll match the mid-market rate — not the best market rate. A mortgage broker shops 30 to 50+ lenders simultaneously and competes them against each other (Alberta Mortgage Brokers Association, 2025). That’s a different tier of competition entirely.

How to Avoid It

Before you sign anything with any bank, get at least one broker quote. It’s free, takes 48 hours, and worst case you use the broker offer as ammunition to push your own bank lower. Most Metro clients save $5,000-$15,000 over a 5-year term just from the comparison alone.

Mistake #5: Skipping the Home Inspection to Win a Bidding War

How often we see it: About 1 in 6 buyers, rising in hot seller’s markets. What it costs: Up to $22,000 in surprise repairs in the first 12 months.

In a bidding war, realtors sometimes suggest waiving the inspection condition to make your offer more attractive. This is the single worst piece of advice a first-time buyer can take. We’ve had Metro clients skip a $600 inspection and inherit:

- A $22,000 furnace replacement (discovered January, 6 weeks after possession)

- A $14,000 foundation crack repair (discovered during spring snow melt)

- A $9,500 main stack plumbing replacement (discovered first week)

- $3,000-$7,000 in electrical panel upgrades required for home insurance

None of those are unusual. Alberta homes, especially older Edmonton stock from the 1970s-80s in mature neighborhoods like Westmount or Bonnie Doon, have real systems-level issues that only a certified inspector catches before possession.

How to Avoid It

Never waive the inspection condition. Ever. If a listing agent tells you “the seller won’t accept conditional offers,” that’s your signal to walk away or restructure — maybe a shortened condition period (48-72 hours) or a pre-offer inspection paid for by the seller. Any experienced Edmonton realtor will back you up on this. A good realtor will refuse to write an offer without an inspection condition regardless of the market.

The Bonus Mistake: Not Opening an FHSA Today

How often we see it: About 1 in 3 first-time buyers who are still 6+ months from purchase. What it costs: $1,760-$3,040 per year in missed tax savings plus delayed contribution room.

The First Home Savings Account is the single best tax-advantaged savings vehicle Canadians have ever had, and contribution room only starts accumulating once the account is open. A $90,000 Alberta earner who waits a year to open the FHSA loses $2,440 in tax savings for that year — permanently. It costs nothing to open an FHSA with zero dollars in it. Do it today. Fund it later.

Read our FHSA Alberta guide for the full tax math. Every Alberta first-time buyer should have an FHSA open before they even start shopping.

Ready to Avoid These Mistakes on Your First Edmonton Home?

Every mistake on this list is 100% avoidable with a 20-minute conversation before you start shopping. Metro’s first-time buyer team walks Edmonton and Calgary clients through all of this every week — free, no pressure, no commitment. Call 780-974-1270 or email info@MetroMortgageGroup.ca to book your free consultation.

For the complete first-time buyer playbook, start with our complete Edmonton first-time home buyer guide. If you’re still figuring out your savings target, read how much down payment you actually need in Alberta.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 17, 2026