How Much Down Payment Do You Need in Alberta?

Down payment requirements, FHSA strategy, and 5%-20% breakdowns for Alberta buyers

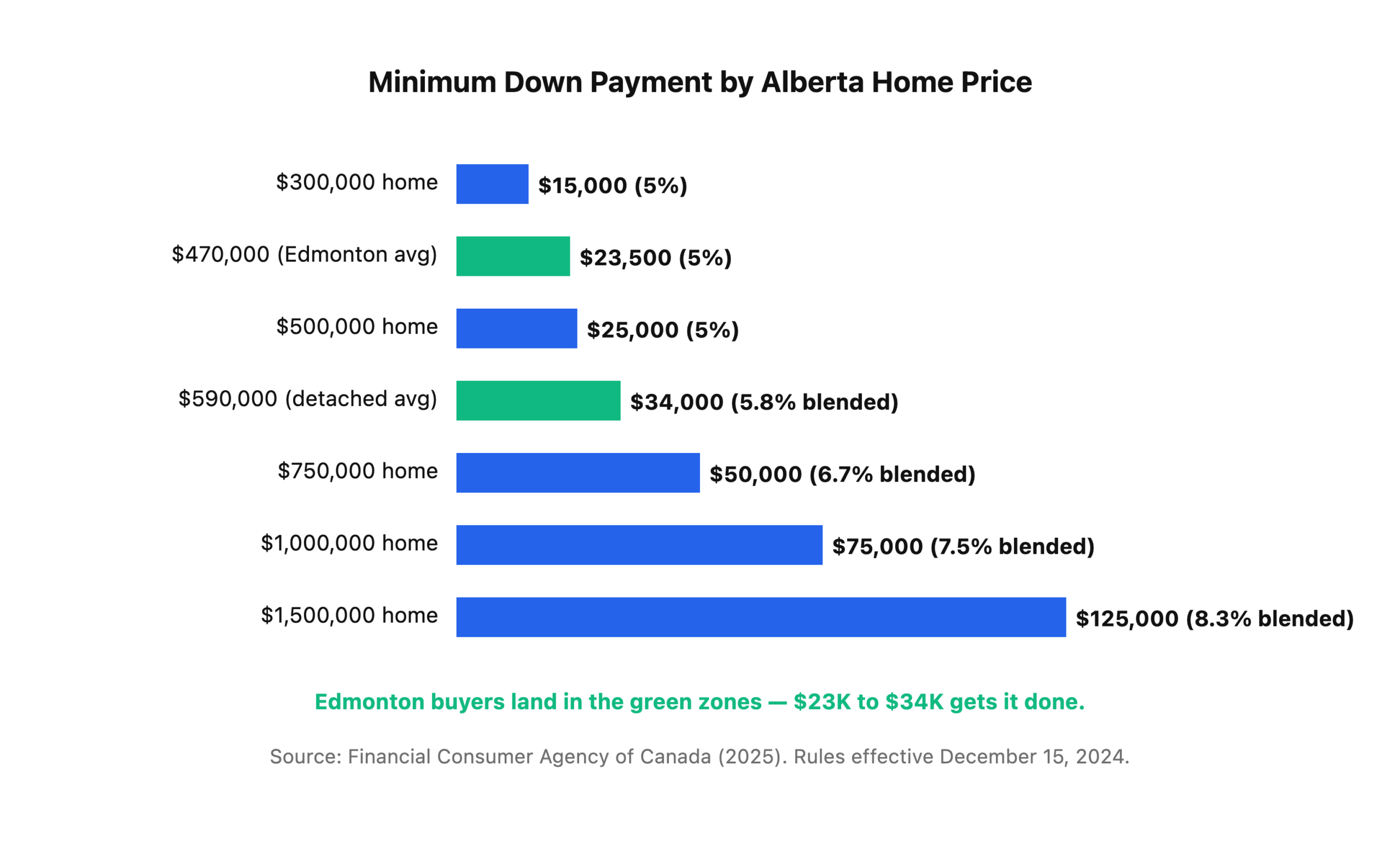

On Edmonton’s $470,819 March 2026 average home, you need just $23,500 down — that’s 5% — to legally buy it with an insured mortgage (REALTORS Association of Edmonton, 2026). Not the $94,000 that the “20% down” myth says you need. Not even close. This is the single most misunderstood number in Alberta home buying, and getting it right can shave 3-5 years off your timeline to homeownership.

Here’s exactly how Canada’s down payment rules work in 2026, what they look like for Alberta homes at every price point, and the stacking strategy we use at Metro to get first-time buyers into their first home with the smallest realistic cash outlay.

Key Takeaways

– 5% is the minimum on homes under $500K; 5% on the first $500K + 10% above up to $1.5M; 20% above $1.5M (Financial Consumer Agency of Canada, 2025).

– On a $470K Edmonton home, the minimum down payment is $23,500 — on a $750K home it’s $50,000.

– Alberta first-time buyers can stack the FHSA ($40,000) and RRSP HBP ($60,000) for up to $100,000 in tax-advantaged down payment funds per person (Canada Revenue Agency, 2026).

– Below 20% down, CMHC default insurance kicks in — a 4.00% premium on the loan at the 5% down level (CMHC, 2025).

What Is the Minimum Down Payment in Alberta in 2026?

Canada’s minimum down payment scales with the home’s purchase price, and the federal rules updated on December 15, 2024 raised the insured mortgage cap to $1.5 million — making 5% down available on homes that previously required 20% (Department of Finance Canada, 2024). The tier structure looks like this:

- Homes under $500,000 — 5% of the purchase price

- Homes $500,000 to $1,500,000 — 5% on the first $500K + 10% on the portion above $500K

- Homes over $1,500,000 — 20% minimum (no default insurance available)

Run the math on a few common Alberta price points:

The sweet spot for Alberta first-time buyers is obvious. The entire Edmonton detached market average ($590,162 in March 2026) still falls in the 5% tier for the first $500K plus 10% on the remaining $90K. That’s $34,000 in total down payment — a number most dual-income Edmonton households can hit in 18-24 months of focused saving with the FHSA and RRSP HBP stacked together.

How Does CMHC Mortgage Insurance Work Below 20%?

Any Alberta mortgage with less than 20% down triggers mandatory default insurance from CMHC, Sagen, or Canada Guaranty — typically charged as a percentage of the loan amount that you can roll directly into your mortgage balance rather than pay upfront (CMHC, 2025). The premium scales with your loan-to-value ratio.

Here are the current CMHC premium rates:

- 90.01% – 95% LTV (5% down) — 4.00% of loan amount

- 85.01% – 90% LTV — 3.10%

- 80.01% – 85% LTV — 2.80%

- 75.01% – 80% LTV — 2.40%

- 80% or less LTV — varies, typically no insurance required

- 30-year amortization add-on — +0.20%

On a $447,000 insured mortgage (5% down on Edmonton’s $470K average), the CMHC premium works out to $17,880 — which most buyers add to the mortgage rather than paying upfront. Stretched over a 30-year amortization at April 2026 rates (around 3.80% insured), that adds roughly $80/month to the payment. Not free, but nowhere near a dealbreaker for most first-time buyers.

The 20% Threshold: When Is It Worth It?

At Metro, we almost never recommend Edmonton first-time buyers wait until they have 20% down. Here’s why: Edmonton home prices have moved only modestly over the past year. If it takes you an extra two years to save the full 20% ($94K vs $23,500), you’ve spent 2 years paying rent instead of building equity, and you’re chasing a moving target — the house that cost $470K today will likely cost more by the time you’ve saved the extra $70K. The FHSA’s tax savings alone (up to $2,440/year for a $90K Alberta earner) offset most of the CMHC premium, making the math even clearer.

Read our FHSA Alberta guide for the full tax-advantage breakdown.

Where Does the Down Payment Actually Come From?

Alberta first-time buyers have access to four tax-advantaged buckets that can fund most or all of their down payment: the FHSA ($40,000 lifetime), the RRSP Home Buyers’ Plan ($60,000), tax-free savings in a TFSA, and gifted funds from immediate family (Canada Revenue Agency, 2026). A single first-time Alberta buyer can access $100,000 in combined FHSA + HBP room. A couple who both qualify can access $200,000.

Here’s the down payment source stack we recommend in order of efficiency:

1. FHSA — The Best Dollar

Contributions are tax-deductible on the way in AND withdrawals are tax-free on the way out. A $90,000 Alberta earner saves $2,440 in taxes for every year they max the $8,000 contribution. That’s essentially free money the federal government is handing you to save for your first home. Open the account today even with a zero-dollar deposit — it starts the clock on contribution room.

2. RRSP Home Buyers’ Plan

Up to $60,000 withdrawal per person from existing RRSP balances, tax-free. Repayment happens over 15 years starting year 2 (or year 5 for 2022-2025 withdrawals under the current grace period). Best if you already have significant RRSP savings built up.

3. TFSA and Regular Savings

Tax-free in the TFSA, taxable but flexible in regular savings. Good for covering the gap between FHSA/HBP and your total target.

4. Gifted Funds

Down payment gifts from parents, grandparents, siblings, or spouse are allowed by every Canadian lender — but they require a signed gift letter confirming the money is a gift with no repayment expected. Most Alberta lenders want to see the gifted funds sitting in your account for 30 days before closing.

How Much Down Payment Should You Actually Put Down?

The right down payment isn’t always the minimum — it’s the amount that minimizes your monthly payment stress while preserving emergency savings for the first two years of homeownership (Bank of Canada, 2026). Most Metro clients land somewhere between 5% and 10% on their first home, keeping a 3-6 month emergency fund untouched and letting the CMHC premium get rolled into the mortgage.

Three scenarios for a $500,000 Edmonton home at 3.80% fixed over 30 years:

- 5% down ($25,000) — $475K mortgage + $19,000 CMHC premium = $494K financed → $2,310/month

- 10% down ($50,000) — $450K mortgage + $13,950 CMHC premium = $463,950 financed → $2,170/month

- 20% down ($100,000) — $400K mortgage, no CMHC premium = $400K financed → $1,870/month

The “extra” $75,000 you’d save waiting to hit 20% down only saves you $440/month. At a $90K household income, that’s roughly 12 months of extra saving for about 2 years of rent. The math rarely favors waiting.

Our take: The right down payment is the one that lets you close AND still have $10,000-$15,000 left in savings the day after possession. Imagine a buyer who drains every last dollar into the down payment — it’s a common regret by month two, when the furnace needs a repair.

Frequently Asked Questions

Can I use gifted money for my Alberta down payment?

Yes. Canadian lenders accept gifted funds from immediate family members (parents, grandparents, siblings, spouse) as down payment, confirmed by a signed gift letter and typically held in your account for 30 days before closing (CMHC, 2025). No repayment can be expected or documented — it must be a true gift.

What counts as “minimum down payment” for an Alberta detached home over $500K?

On a $600,000 Edmonton detached home, you need 5% of the first $500,000 ($25,000) plus 10% of the remaining $100,000 ($10,000) for a total of $35,000 (Financial Consumer Agency of Canada, 2025). That’s a 5.83% blended rate. The formula scales cleanly up to the $1.5M cap.

Do I need 20% down to avoid CMHC insurance in Alberta?

Yes. Any insured mortgage with less than 20% down requires default insurance through CMHC, Sagen, or Canada Guaranty (CMHC, 2025). Premiums range from 4.00% at 5% down to 2.40% at 19% down, and most Alberta borrowers roll the premium into the mortgage rather than paying it upfront.

Can I stack the FHSA and RRSP Home Buyers’ Plan together?

Yes — they’re stackable under current CRA rules. A single first-time buyer can access up to $100,000 tax-advantaged ($40K FHSA + $60K HBP), and a qualifying Alberta couple can combine for $200,000 (Canada Revenue Agency, 2026). That’s enough to cover a 20%+ down payment on a $1M detached Edmonton home without any non-registered savings.

Ready to Figure Out Your Alberta Down Payment Plan?

The right down payment for you depends on your income, timeline, existing savings, and which of the four funding buckets you’ve already started using. Metro’s first-time buyer team builds these plans every week for Edmonton and Calgary buyers — free, no pressure, no commitment. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full first-time buyer roadmap, start with our complete Edmonton first-time home buyer guide. Then read the FHSA Alberta walkthrough for the tax math that changes everything about down payment timing.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 13, 2026