FHSA Alberta: First Home Savings Account 2026

Tax-free savings up to $40K for first-time home buyers in Alberta

As of the end of 2023, about 739,000 Canadians had already opened a First Home Savings Account — but most don’t know that a single Alberta earner on a $90,000 salary saves $2,440 in income tax every year they max it out (Canada Revenue Agency, 2025). That’s the kind of number that changes how fast you can actually afford your first Edmonton or Calgary home.

If you’re an Alberta first-time buyer who’s heard of the FHSA but isn’t sure how the rules actually work in 2026, this guide walks through every number, threshold, and deadline that matters — from contribution limits to the exact six-condition checklist for a tax-free withdrawal.

Key Takeaways

– The FHSA lets first-time buyers contribute $8,000/year up to $40,000 lifetime, with contributions deductible on the way in and withdrawals tax-free on the way out (Canada Revenue Agency, 2026).

– An Alberta household earning $90,000 saves roughly $2,440 per year in combined federal + provincial tax by maxing the annual contribution (TaxTips.ca, 2025).

– FHSA and the RRSP Home Buyers’ Plan are stackable — an Alberta couple can access up to $200,000 of tax-advantaged down payment funds by combining them (CIBC, 2025).

– If you never buy a home, FHSA savings roll tax-free into your RRSP without using a dollar of your existing RRSP contribution room (Canada Revenue Agency, 2026).

What Is the FHSA and Who Qualifies in Alberta?

The First Home Savings Account is a federally registered plan that launched April 1, 2023, combining the tax deduction of an RRSP with the tax-free withdrawal of a TFSA — and by the end of 2023, 739,000 Canadians had opened one, holding $2.79 billion in tax-sheltered savings (Canada Revenue Agency, 2025). For Alberta first-time buyers, it’s the single most powerful tool on the down-payment checklist.

To open an FHSA in Alberta, you need to meet three CRA conditions (Canada Revenue Agency, 2026):

- Be at least 18 and no older than 71 (Alberta’s age of majority is 18)

- Be a Canadian resident with a valid SIN

- Qualify as a first-time home buyer — meaning you did not live in a home that you (or your current spouse) owned in the current year or any of the previous 4 calendar years

That last point catches a lot of Alberta buyers off guard. If you sold a condo in 2020 and have rented since, you’re a first-time buyer again for FHSA purposes — the 4-year clock already reset. The CRA’s definition is about recent ownership, not whether you’ve ever owned before.

Who Doesn’t Qualify

You can’t open an FHSA if you or your spouse owned and lived in a home in the past 4 years, if you’re over 71, or if you aren’t a Canadian tax resident. Non-residents can’t open an FHSA even if they plan to immigrate and buy a home later.

How Much Can You Contribute in 2026?

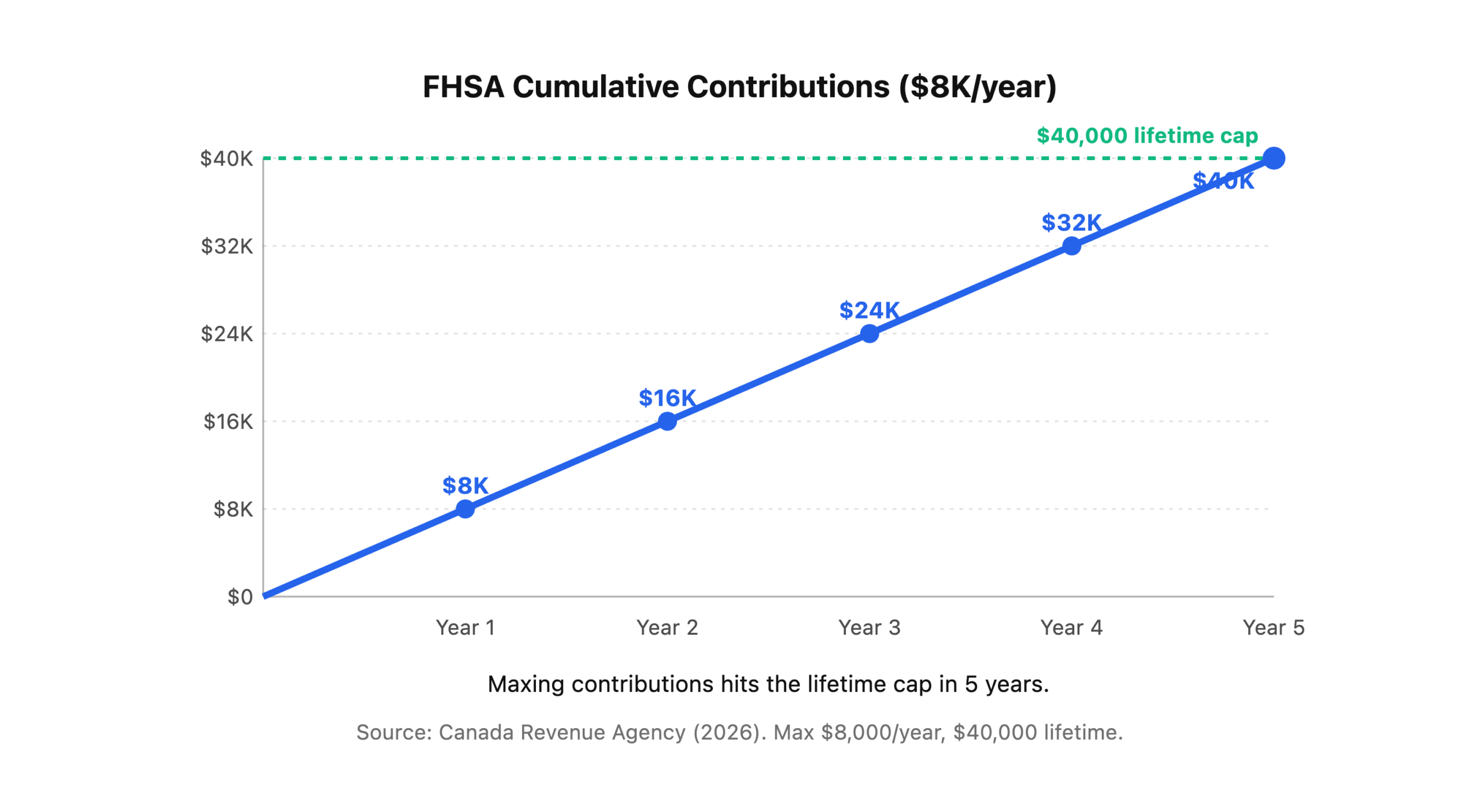

You can contribute up to $8,000 per year with a $40,000 lifetime maximum (Canada Revenue Agency, 2026). Contribution room only starts accumulating once the account is open, which means the single most important FHSA move for any Alberta pre-buyer is opening the account today — even with a zero-dollar deposit.

Unused contribution room carries forward, but with a ceiling. If you contribute only $3,000 in year one, the remaining $5,000 of room carries into year two — but you can never contribute more than $16,000 in any single calendar year (current year $8,000 + maximum $8,000 of carry-forward). That’s the cap regardless of how much room you’ve accumulated.

Here’s how a steady-contributor path looks if you open the account in 2026 and max it each year:

One overlooked benefit: the FHSA tax deduction is never lost if you don’t claim it right away. You can carry deductions forward to a future year when you’re in a higher bracket — useful if you’re a new graduate expecting to earn more in 2027 than 2026.

How Much Can Alberta First-Time Buyers Save in Taxes?

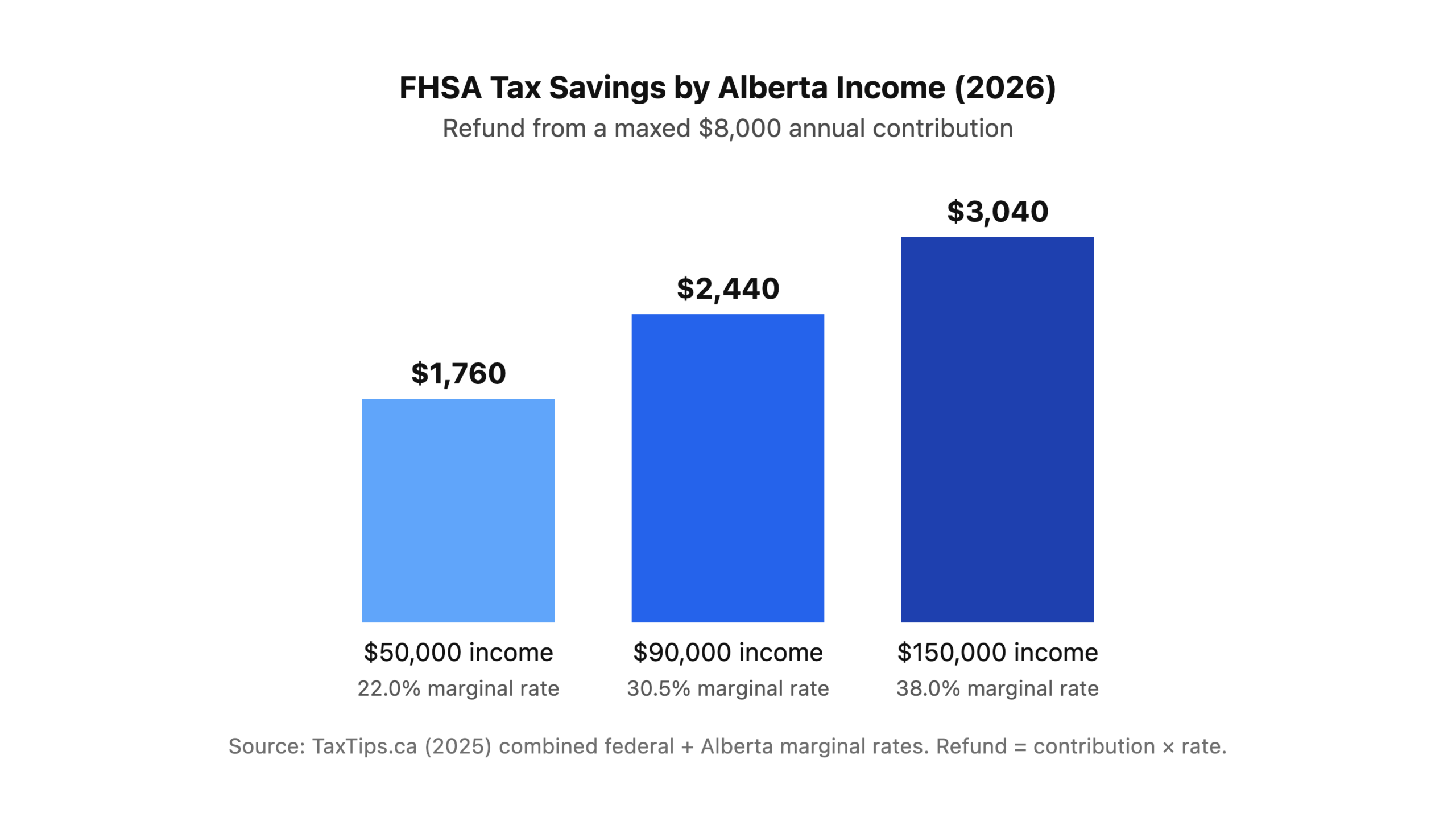

Every dollar contributed to an FHSA reduces your taxable income, so your savings depend on your combined federal plus Alberta marginal tax rate. On a maxed-out $8,000 contribution, a $50,000 earner saves about $1,760, a $90,000 earner saves $2,440, and a $150,000 earner saves $3,040 in reduced taxes that same year (TaxTips.ca, 2025).

Those are real dollars back into your down payment fund — effectively a government top-up you only get if you use the account.

Over the full five-year contribution path to the $40,000 lifetime cap, the math compounds. Based on Metro’s own illustrative calculation, a $90,000 Alberta earner who maxes out every year from 2026 through 2030 would save roughly $12,200 in total income tax — more than enough to cover closing costs on an average Edmonton home. That’s the government paying you to save for a down payment.

FHSA vs RRSP Home Buyers’ Plan — Which One Should You Use?

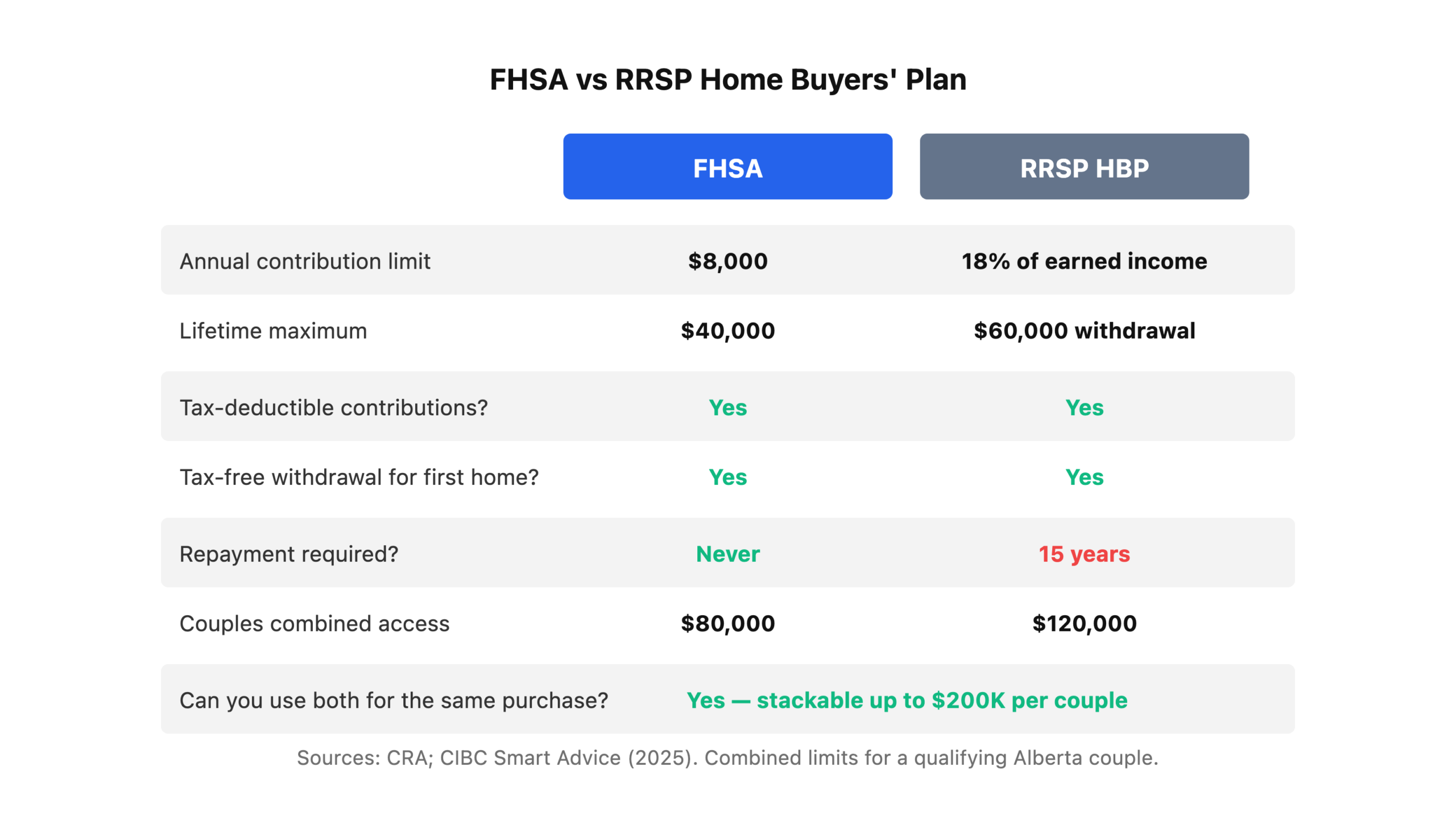

An Alberta couple who both qualify as first-time buyers can combine the two programs to access up to $200,000 in tax-advantaged down payment funds — $80,000 from FHSAs (no repayment ever required) plus $120,000 from the RRSP Home Buyers’ Plan (repayable over 15 years) (CIBC, 2025). The short answer to “which should you use?” is almost always both.

The two programs work very differently under the hood:

The biggest real-world advantage of the FHSA is the no-repayment rule. Under the RRSP HBP, you have to pay back every withdrawn dollar over 15 years (or face tax penalties on missed payments). The FHSA has no such clawback — once you withdraw for a qualifying first home, the money is yours, and the tax deduction you already claimed stays claimed.

In our day-to-day work at Metro, we usually recommend Alberta clients max the FHSA first because of this exact reason. The HBP is still valuable — especially for buyers with large existing RRSPs — but the repayment obligation cuts into the monthly cash flow of a brand-new homeowner who’s already stretched. Drain the FHSA first, then dip into the HBP only as much as you need to hit your target down payment.

Where Can Alberta Buyers Open an FHSA?

Every Big 5 Canadian bank offers an FHSA, and Alberta’s two largest local institutions — ATB Financial and Servus Credit Union — both offer FHSA products alongside their regular investment lineups (ATB Financial, 2026; Servus Credit Union, 2026). That’s important for Alberta-resident buyers who prefer banking with locally-owned institutions.

Your main FHSA provider options break down into four buckets:

- Big 5 banks — RBC, TD, BMO, Scotiabank, CIBC all offer FHSA savings accounts, GICs, mutual funds, and self-directed brokerage options

- Alberta financial institutions — ATB Financial (Daily Interest, GICs, ATB Wealth managed portfolios) and Servus Credit Union (GICs, mutual funds, self-directed stocks via Aviso)

- Discount brokerages — Questrade and CIBC Investor’s Edge offer self-directed FHSAs for DIY investors who want to hold ETFs and stocks

- Robo-advisors and online banks — Wealthsimple, EQ Bank, and Tangerine all offer simple low-fee FHSA products

What to Actually Invest In

The account is a container. What you hold inside it matters far more than where you open it. For a first-time buyer on a 3-5 year purchase timeline, hold low-volatility assets — high-interest savings, GICs, or short-duration bond funds. The FHSA’s tax advantage works best when the principal is intact at withdrawal time. A stock-market correction in year four of your contribution path could easily wipe out three years of tax savings.

What Are the Rules for a Tax-Free FHSA Withdrawal?

To pull money out of your FHSA tax-free, the CRA requires you to satisfy six simultaneous conditions — and miss any one of them and the withdrawal becomes fully taxable income (Canada Revenue Agency, 2026).

This is the single most common FHSA mistake we see at Metro. A meaningful share of first-time buyer clients come in with either a paperwork error (no signed purchase agreement) or a timing mismatch (withdrawal made before an offer was accepted). Both sink the tax-free status.

The six conditions for a qualifying FHSA withdrawal are:

- First-time buyer status — you haven’t lived in a home you or your current spouse owned, in the current year or any of the prior 4 calendar years (except the 30 days immediately before withdrawal)

- Written agreement to buy or build — signed purchase contract with a closing date before October 1 of the year following your withdrawal

- 30-day rule — you can’t have acquired the qualifying home more than 30 days before the withdrawal

- Canadian residency — you must remain a Canadian resident from the withdrawal through closing (or death)

- Principal residence intent — you must intend to occupy the home as your principal residence within one year of buying or building

- Form RC725 — you must file Form RC725 with your FHSA issuer to authorize the qualifying withdrawal

The October 1 trap: If you withdraw from your FHSA in November 2026, the signed purchase agreement must have a closing date no later than October 1, 2027 — otherwise the withdrawal becomes taxable. That’s an 11-month window, not a full calendar year. Time the withdrawal to the offer, not the other way around.

Get this wrong and the tax consequences are severe. A non-qualifying FHSA withdrawal is taxed as regular income in the year you receive it, which could push an Alberta buyer into a higher marginal bracket and erase the original deduction benefit entirely.

Frequently Asked Questions

What happens to the FHSA if I never buy a home?

You can transfer the entire balance to your RRSP or RRIF tax-free, without using any RRSP contribution room, up to the maximum participation period (15 years from account opening, or by age 71, whichever comes first) (Canada Revenue Agency, 2026). Any amount not transferred is withdrawn as fully taxable income.

Can I have more than one FHSA?

Yes — you can hold multiple FHSAs at different institutions, but the $8,000 annual and $40,000 lifetime limits apply in aggregate across all your accounts combined (Canada Revenue Agency, 2026). Over-contributing triggers a 1% per month penalty tax until the excess is withdrawn.

How long does the FHSA account last?

Your FHSA ends on the earliest of three dates: the 15th anniversary of opening your first FHSA, the year you turn 71, or the year following your first qualifying withdrawal (TaxTips.ca, 2026). After that you must transfer the balance to an RRSP/RRIF or withdraw it as taxable income.

Does my spouse’s past home ownership disqualify me?

Yes — if you have a current spouse or common-law partner who lived in a home they owned in the current year or the previous 4 calendar years, you don’t qualify as a first-time buyer for FHSA purposes (Canada Revenue Agency, 2026). The rule is relationship-based: your partner’s ownership counts against you.

Can I use the FHSA and the First-Time Home Buyer Tax Credit together?

Yes, they’re completely independent programs. The FHSA reduces taxable income on contributions, while the First-Time Home Buyers’ Tax Credit is a non-refundable federal credit of up to $1,500 claimed in the year you buy a qualifying home (Canada Revenue Agency, 2026). Alberta first-time buyers should claim both.

Ready to Open Your Alberta FHSA?

The fastest win for any Alberta first-time buyer is opening an FHSA today — even with a one-dollar deposit. That single action starts the 15-year clock, unlocks the $8,000 contribution room for the current year, and makes every dollar you save between now and closing day tax-deductible. We help Edmonton and Calgary clients build full FHSA + RRSP + down-payment strategies every week.

If you want us to review your income, your timeline, and which combination of FHSA, HBP, and savings-rate pace will get you to the keys fastest, book a free 20-minute first-time buyer consultation. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

Keep reading: Start with our complete first-time buyer guide for Edmonton for the full pillar overview, then dig into the RRSP Home Buyers Plan walkthrough for Alberta buyers and our breakdown of how much down payment you actually need in Alberta.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: April 8, 2026