Credit Score Requirements for an Alberta Mortgage

What credit score you need and how to improve yours before applying

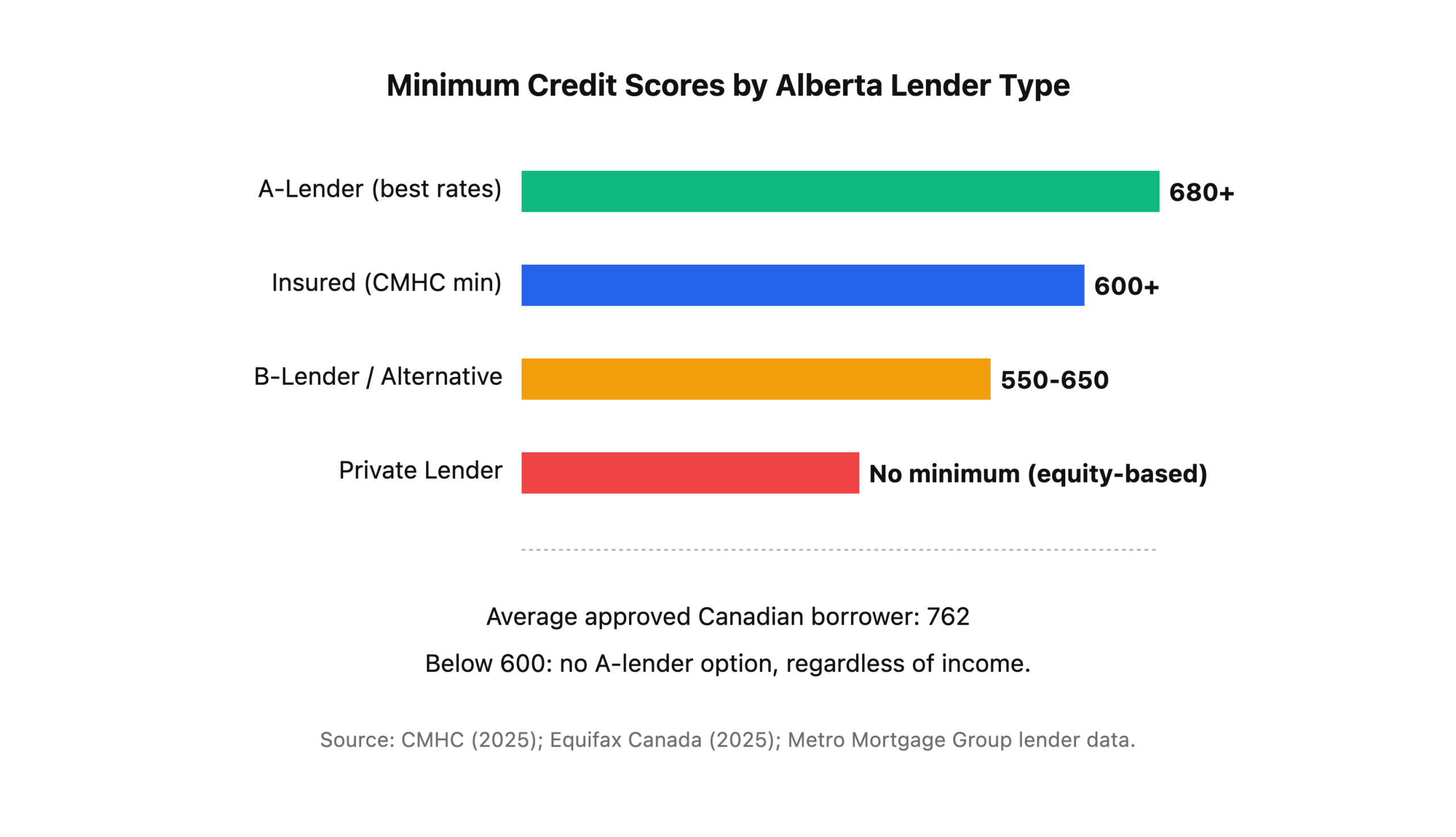

The minimum credit score for an insured mortgage in Alberta is 600, but most A-lender banks want 680 or higher for the best rates and the average approved Canadian borrower actually sits at 762 (CMHC, 2025; Equifax Canada, 2025). The score you bring to your application decides not just whether you qualify, but how much your Edmonton mortgage will cost you over the next 25 years.

Here’s every credit score threshold Alberta lenders actually use in 2026, what a 60-point difference costs a typical Edmonton buyer, and how to repair a thin file in 6-12 months before you apply.

Key Takeaways

– 600 is the hard minimum for a CMHC-insured Alberta mortgage; 680+ unlocks the best A-lender bank rates (CMHC, 2025).

– The average Canadian credit score hit 762 in 2025, up 4 points year-over-year (Equifax Canada, 2025).

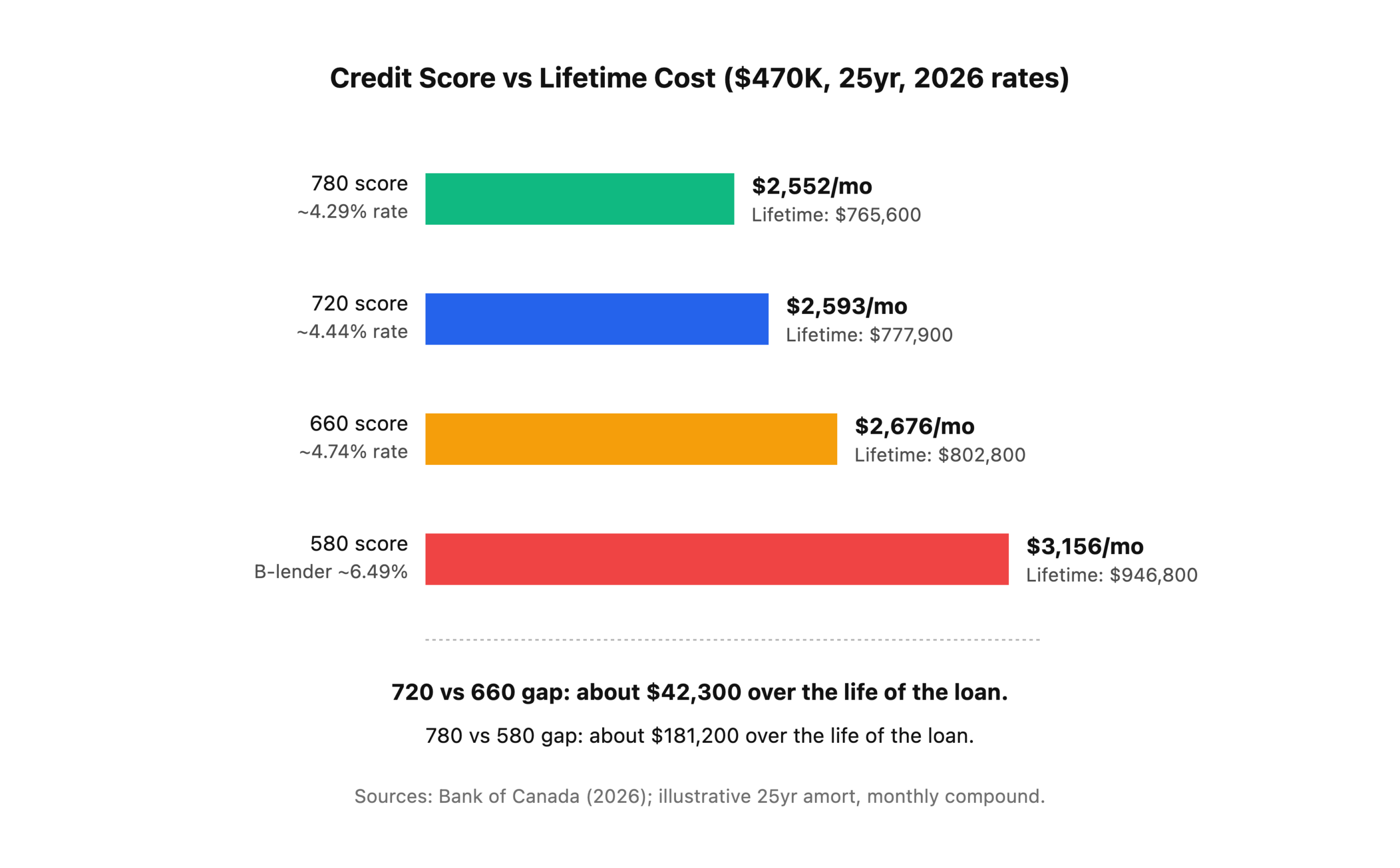

– A 60-point score gap (660 vs 720) costs an Edmonton buyer roughly $42,000 over a 25-year amortization on a $470K mortgage.

– Canada uses two credit bureaus, Equifax and TransUnion, and most lenders pull both and use the lower of the two.

– You can repair a thin or damaged Alberta credit file in 6-12 months with secured cards, utilization discipline, and on-time payments.

What Is the Minimum Credit Score for a Mortgage in Alberta?

The absolute minimum credit score for a mortgage in Alberta is 600 for any CMHC, Sagen, or Canada Guaranty insured loan, a rule that applies nationally to every federally regulated lender (CMHC, 2025). Below 600, your only options are alternative B-lenders or private lenders, both with meaningfully higher rates.

Here’s how Alberta lenders actually tier credit scores in 2026:

- 760+ — Exceptional. Best-available discounted rates at every A-lender.

- 720-759 — Very good. Qualifies for top-tier bank pricing.

- 680-719 — Good. Qualifies at all A-lenders with standard rates.

- 660-679 — Fair. Some rate premium, still A-lender eligible.

- 600-659 — Weak A-lender territory. Insured only, limited lenders.

- 550-599 — B-lender / alternative lender territory.

- Below 550 — Private lender only, equity-based qualification.

A quick note on the 600 threshold. CMHC requires only one applicant on the mortgage to hit 600 on joint applications, so a strong co-borrower can carry a partner with a weaker file. That’s a workaround we use often for Edmonton couples where one person has a thin or damaged credit history from student years or a recent immigration move.

How Do Equifax and TransUnion Differ in Canada?

Canada has two credit bureaus, Equifax and TransUnion, and they rarely report identical scores because lenders don’t always report to both bureaus (Financial Consumer Agency of Canada, 2025). A typical Canadian sees a 20-40 point gap between the two reports, and Alberta mortgage lenders are aware of it.

Most Alberta A-lenders pull both bureaus on a mortgage application and use one of three rules:

- Lower of the two — conservative banks (the majority in Alberta)

- Middle score — if they pull three scores via a tri-merge

- Highest of the two — rare, a few credit unions and B-lenders

What Goes Into a Canadian Credit Score?

Both Equifax and TransUnion use roughly the same five-factor model for Canadian credit scoring (Equifax Canada, 2025):

- Payment history — 35% — On-time payments on every credit account. One missed payment can drop you 60-100 points.

- Credit utilization — 30% — How much of your available credit you’re using. Keep it under 30% per card.

- Length of credit history — 15% — The age of your oldest account and the average age of all accounts.

- Credit mix — 10% — A healthy mix of revolving (cards) and installment (loans).

- New credit inquiries — 10% — Hard pulls stay on your file for 3 years and can ding you 5-10 points each.

Utilization is the single biggest quick-win lever for Alberta buyers. If you’re sitting at 80% on a $5,000 credit card the month before applying, paying it down to under $1,500 can lift your score 30-50 points within a single billing cycle.

How Much Does Your Credit Score Actually Cost You on an Edmonton Mortgage?

A 60-point credit score difference costs a typical Edmonton buyer roughly $42,000 in extra interest over a 25-year amortization on a $470,000 mortgage, based on current 2026 Bank of Canada overnight rate spreads (Bank of Canada, 2026). That’s real money, equivalent to a down payment on a second investment property.

Here’s how the numbers actually pencil out on a $470,000 Edmonton mortgage across four common credit score bands:

The jump from 660 to 720 is where the biggest real-world savings live for Edmonton buyers. It’s also the most achievable jump for a motivated borrower. Most of our clients who commit to a credit improvement plan hit that 60-point target inside of 8-10 months.

Read our breakdown on how much down payment you actually need in Alberta to pair this credit score math with your total cash-to-close target.

How Do You Check Your Credit Score in Canada for Free?

You can check your Canadian credit score for free in three ways, and none of them ding your score because they use soft inquiries (Financial Consumer Agency of Canada, 2025). Hard inquiries, the kind lenders do when you apply for credit, stay on your file for three years.

Your free options in 2026:

- Borrowell — Free Equifax score and full report, updated weekly. The most-used free tool in Canada with over 3 million users (Borrowell, 2024).

- Credit Karma Canada — Free TransUnion score and report, updated weekly.

- Direct from Equifax or TransUnion — You’re legally entitled to a free credit report once per year by mail from each bureau under federal privacy law (Equifax Canada, 2025).

Most of your Alberta bank’s mobile app also shows a free credit score now. RBC, TD, Scotia, CIBC, and BMO all include it as a default feature. Check both an Equifax source and a TransUnion source before applying for a mortgage so you see the full picture your Metro broker will see.

How Do You Repair a Damaged or Thin Credit File Before Applying?

Most Alberta buyers can move a damaged or thin credit file up 60-100 points in 6-12 months with a disciplined repair plan, which is enough to move from B-lender territory into A-lender territory (Financial Consumer Agency of Canada, 2025). The key is starting early, before you fall in love with a specific Edmonton listing.

We recently helped an Edmonton client, a 32-year-old nurse relocating from Winnipeg, who showed up with a 612 credit score and a dream of buying a $435K detached in Rutherford. Her file had one stale medical collection dragging everything down. We paused her application, wrote a dispute letter to Equifax on the collection, added her as an authorized user on her partner’s 8-year-old Visa card, and coached her to keep utilization under 20%. Nine months later she applied at 724 and closed at a rate 0.52% lower than she would have qualified for in month one, saving her roughly $38,000 over her 25-year amortization.

A Practical 6-Month Credit Repair Framework

- Pull both bureaus the day you start — dispute any errors in writing, send by registered mail.

- Pay every bill on the day it’s due — set up autopay on the minimum for every account, then make manual payments for the full balance.

- Crush utilization to under 30%, ideally under 10% — pay cards down before statement date, not after.

- Do not close old cards — your oldest account is worth more than you think. Leave it open with a small recurring charge.

- Do not apply for new credit in the 6 months before your mortgage application, full stop.

- Add a thin file with a secured card — a Capital One Guaranteed Secured or Home Trust secured card builds history fast, and both report to Equifax and TransUnion.

For new-to-Canada buyers, most A-lenders accept a 12-month rental history plus 6 months of cell phone / utility on-time payments as an alternative credit reference under CMHC Newcomer program rules (CMHC, 2025). You don’t have to wait 2 years to qualify.

Before you apply, also read our guide on the 5 first-time homebuyer mistakes we see in Edmonton, because a damaged credit file is only one of them.

When Should You Apply Through a Broker Versus Your Bank?

Mortgage brokers access 40+ lenders on a single application with a single soft credit pull, while going bank-to-bank creates multiple hard inquiries that compound and actively damage your score (Canadian Mortgage Brokers Association, 2024). For any Alberta borrower with a credit score under 720, this is the single biggest reason to use a broker.

Here’s the mechanical difference:

- Bank-direct shopping — Each bank pulls a hard inquiry. Shop 4 banks, take 4 hard hits. Score can drop 20-40 points before you’ve even made an offer.

- Broker single-pull — We pull your credit once (soft first, then one hard pull for the chosen lender), then present your file to multiple lenders using that single report.

On top of that, a broker has access to lenders that don’t exist at the retail level: monoline lenders like First National, MCAP, and Strive, plus B-lender relationships for clients in the 550-650 band that no bank branch manager can offer. If your credit is borderline, you need a broker. If your credit is exceptional, you probably still want a broker, but for rate-shopping rather than rescue.

Call our team at 780-974-1270 for a free, no-obligation credit review. We’ll tell you exactly what tier your file falls into and what rate you’d qualify for today versus 6 months from now.

Ready to Find Out What Rate Your Credit Score Actually Qualifies For?

The biggest mistake we see Alberta first-time buyers make is guessing at their credit standing instead of checking it. Pull both Equifax and TransUnion before you start house hunting, not after. Metro Mortgage Group runs free credit reviews for Edmonton and Calgary buyers every day, and we’ll tell you honestly whether you should apply now or spend 6 months on a repair plan first. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the complete roadmap, start with our Edmonton first-time home buyer guide, then price the rest of your cash-to-close with our closing costs Alberta 2026 breakdown.

Frequently Asked Questions

Can I get a mortgage in Alberta with a 580 credit score?

Yes, but not from an A-lender bank. At 580 you’re in B-lender territory, which means alternative lenders like Home Trust, Equitable Bank, or MCAP with rates roughly 1.5-2.5% higher than prime bank rates (CMHC, 2025). Most Edmonton buyers in this range use a B-lender short-term, then refinance to an A-lender once their score crosses 680.

What’s the average credit score in Alberta?

The average credit score in Alberta sits right around the Canadian national average of 762 as of mid-2025, with Albertans slightly above the national mean thanks to higher average household incomes (Equifax Canada, 2025). Edmonton specifically tracks within 2-3 points of the national average. First-time buyers in their late 20s typically sit around 725, still well inside A-lender territory.

Does checking my own credit score hurt it?

No. Checking your own credit score through Borrowell, Credit Karma, your bank app, or directly from Equifax or TransUnion is a soft inquiry and has zero impact on your score (Financial Consumer Agency of Canada, 2025). Only hard inquiries from lenders when you apply for new credit affect your score, and each one typically costs 5-10 points for up to 12 months.

How long does it take to raise my credit score from 650 to 720?

Most Alberta borrowers see a 650-to-720 jump in 6 to 10 months with disciplined utilization management and perfect on-time payments across all accounts (Equifax Canada, 2025). The fastest wins come from paying revolving card balances below 10% of limit before the statement date. We’ve seen clients jump 40 points in a single billing cycle with nothing but utilization fixes.

Do I need a credit score at all to buy a home in Alberta?

Not strictly, but your options are extremely limited without one. New-to-Canada buyers without a Canadian credit file can qualify through the CMHC Newcomer program using 12 months of rental history and 6 months of on-time utility or phone payments as alternative credit (CMHC, 2025). Canadian-born buyers without a credit file typically need to build one for 6-12 months with a secured card first.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and has helped Edmonton and Alberta families secure mortgages since 2011. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: April 22, 2026