Edmonton Rent vs Buy 2026: When Renting Stops Making Sense

On Edmonton’s $470,819 March 2026 average home, the monthly carrying cost at a 4.49% 5-year fixed rate now runs about $2,510 — only $880 more than the city’s average $1,630 two-bedroom rent (REALTORS Association of Edmonton, 2026; rentals.ca, 2026). Once equity build-up is factored in, the breakeven point lands at roughly 3.5 years — the shortest Edmonton has seen since 2015.

For anyone planning to stay in Edmonton longer than 3-4 years, the math has quietly flipped. Here’s the full 2026 breakdown.

Key Takeaways

– Edmonton’s average home sold for $470,819 in March 2026, up 13.8% year-over-year (REALTORS Association of Edmonton, 2026).

– Average 2-bedroom Edmonton rent hit $1,630/month in Q1 2026 — up 22% since 2022 (rentals.ca, 2026).

– The rent-vs-buy breakeven on a $470K Edmonton home now sits at 3.5 years with 5% down at current rates.

– A 5-year Edmonton buyer builds roughly $75,000 in equity while a renter pays $102,000 to a landlord with zero ownership.

– You should keep renting if your timeline is under 3 years, your income is unstable, or you carry high-interest consumer debt.

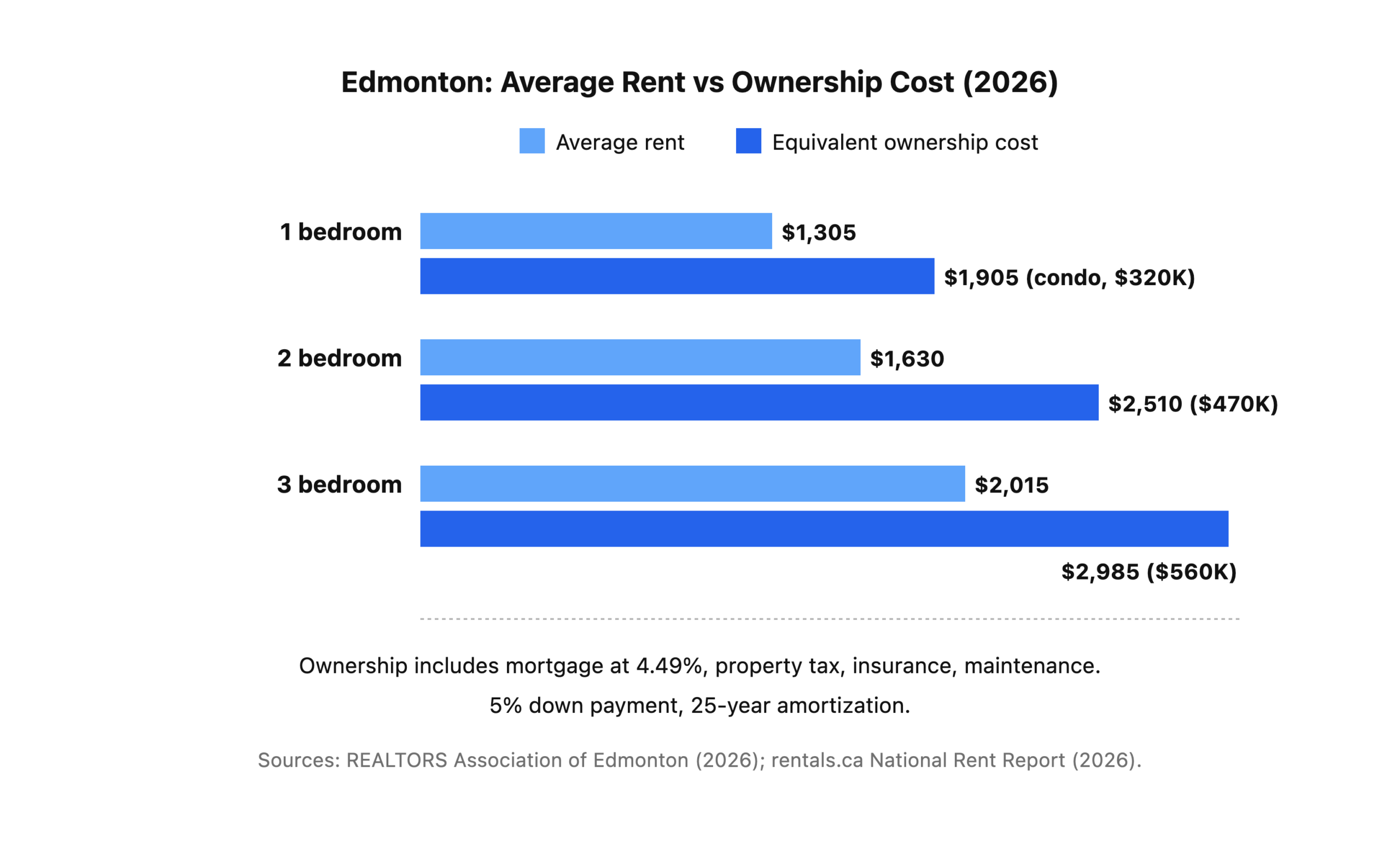

How Much Does It Actually Cost to Rent vs Buy in Edmonton in 2026?

The gap between renting and owning in Edmonton has narrowed to roughly $880/month in 2026, the tightest spread in a decade (rentals.ca, 2026; Bank of Canada, 2026). On a $470K home with 5% down at a 4.49% 5-year fixed, total monthly ownership cost runs about $2,510 including mortgage, taxes, insurance, and condo-level maintenance reserve.

Here’s the side-by-side for a typical Edmonton household choosing between a 2-bedroom rental and a similar 2-bedroom starter home:

The raw monthly number still favours renting by $600-$1,000 — but raw monthly cost isn’t the full picture. A mortgage payment builds equity; rent builds nothing. Once you subtract the principal portion of your mortgage payment (roughly $625/month in year one on a $447K loan), the real cost gap shrinks to about $255/month on a 2-bedroom.

Is It Cheaper to Rent or Buy in Edmonton Right Now?

For a stay of less than 3 years, renting is cheaper; for 5+ years, buying wins by a wide margin (CMHC, 2025). Edmonton’s structural rent increases of 6-8% annually since 2023 have compressed the breakeven window, because rent keeps climbing while a fixed mortgage payment stays locked in.

Here’s how the 5-year math shakes out for two identical Edmonton households, one renting a $1,630 two-bedroom and one buying a $470K starter home:

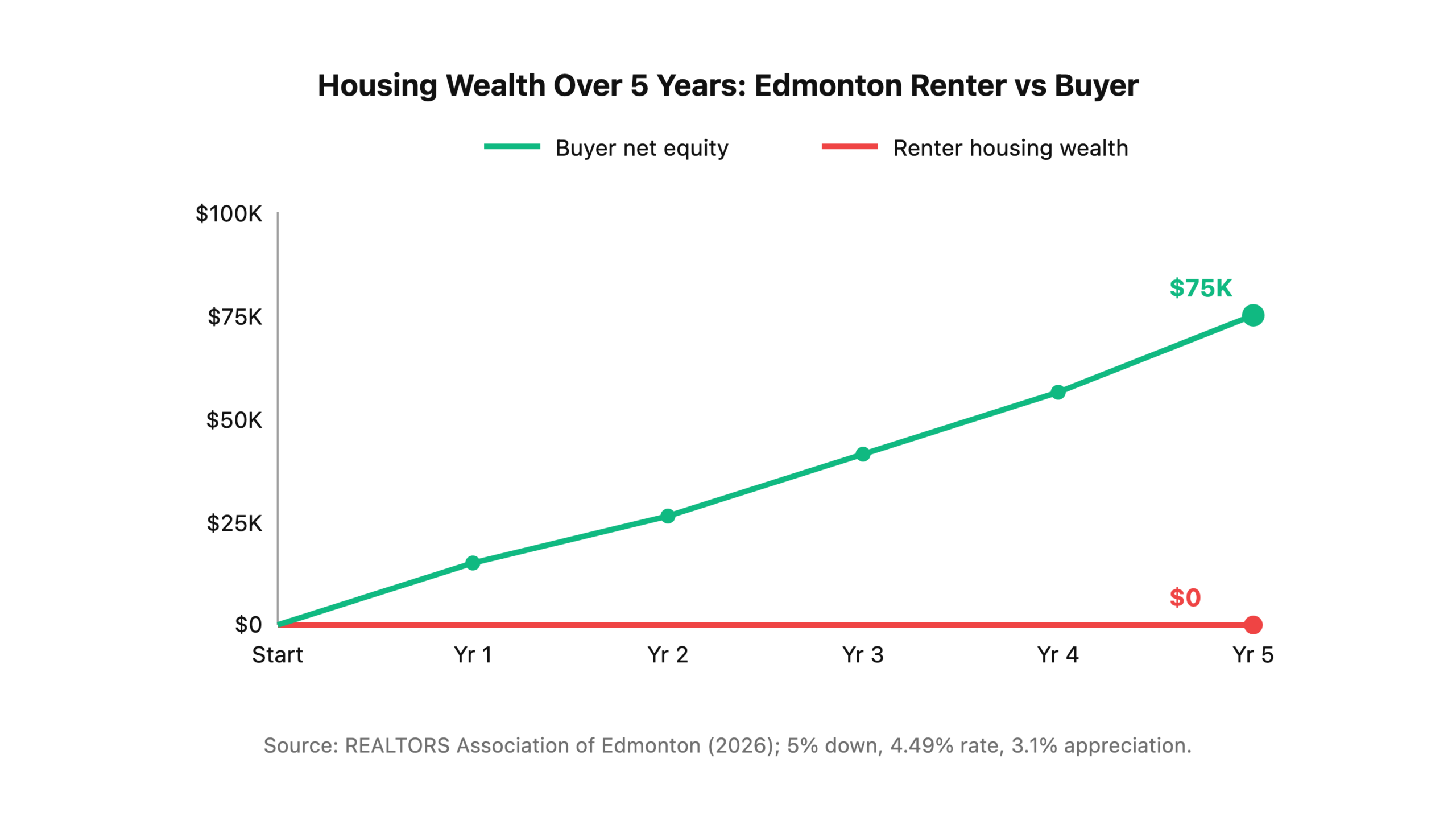

The 5-Year Scorecard

- Renter — Pays $102,000 in rent over 5 years (assuming 5% annual rent increases, well below Edmonton’s 2024-2025 average). Ends with $0 in housing equity.

- Buyer — Pays $150,600 in total carrying costs over 5 years. Of that, roughly $40,500 goes to principal (equity). Plus $35,000-$50,000 in home price appreciation on a $470K base at Edmonton’s 10-year average of 3.1%/year (REALTORS Association of Edmonton, 2026). Net housing wealth after 5 years: ~$75,000.

The real insight most rent-vs-buy calculators miss: Edmonton’s rent growth has been faster than home price growth in 2024-2025, an unusual inversion. Rents climbed roughly 16% while home prices climbed about 14% over the same window. That’s what has pulled the breakeven so close to the 3-year mark, a level we haven’t seen in Alberta since 2015.

Why Have Edmonton Rents Risen So Fast Since 2022?

Edmonton average rents jumped 22% between Q1 2022 and Q1 2026, driven by record interprovincial migration and a purpose-built rental vacancy rate that fell to 2.4% in the latest CMHC report (CMHC Rental Market Report, 2025; Statistics Canada, 2026). Alberta added over 200,000 net new residents in 2023-2024 alone, and a large share chose Edmonton because it’s still the most affordable big city in Canada.

Three forces are pushing Edmonton rents upward at the same time:

1. Interprovincial Migration

Albertans arriving from Ontario and BC are used to paying $2,500+ for a 1-bedroom and happily sign leases at $1,300-$1,500 in Edmonton. Landlords have responded by raising asking rents on turnover, which has no rent cap in Alberta. This is structural and unlikely to reverse in the next 3-5 years.

2. Tight Purpose-Built Vacancy

CMHC pegs Edmonton’s purpose-built rental vacancy at 2.4%, well below the 3% “balanced market” threshold. Anything under 3% gives landlords pricing power, and Edmonton hasn’t been above 3% since 2022.

3. Slower New Rental Construction

Higher interest rates in 2023-2024 stalled dozens of Edmonton rental projects. The units coming online in 2026 were approved in 2020-2021, and the pipeline behind them thins out significantly through 2027-2028.

When Does Renting Still Make More Sense?

Renting still beats buying if your timeline is under 3 years, your employment is unstable, or you carry high-interest consumer debt at rates above your potential mortgage rate (Financial Consumer Agency of Canada, 2025). The break-even math only works when you stay long enough to cover the transaction costs — closing costs, Realtor fees on eventual sale, and mortgage interest paid in years 1-2.

Keep Renting If Any of These Apply

- You’ll move within 3 years — closing costs plus eventual sale commissions (roughly 5% of sale price) will eat any equity gains.

- Your employment is unstable — a layoff 18 months into a mortgage is far more stressful than a layoff 18 months into a lease.

- You carry consumer debt above 7% — pay off the credit cards and unsecured lines of credit first. Every $10K of 19.99% credit card debt costs $2,000/year, which is more than a year of Edmonton homeownership premium.

- You have no down payment or closing cost reserve — scrambling for the minimum 5% and cutting your emergency fund to zero is a recipe for panic-selling in year 2. See our full breakdown on how much down payment you actually need in Alberta.

- You’re unsure about the city — if there’s any chance you leave Edmonton in the next 24 months, don’t buy.

We had a client in Mill Woods last spring who came to us ready to buy at 26 years old, pre-approved, 5% saved, the whole package. Two conversations in, it came out that her contract job was ending in 8 months and she wasn’t sure she’d stay in Alberta. We told her to keep renting. She came back 14 months later with a permanent role at the University of Alberta, bought a townhouse in Rutherford, and is on track to build $70K in equity by 2030. Timing matters more than rate.

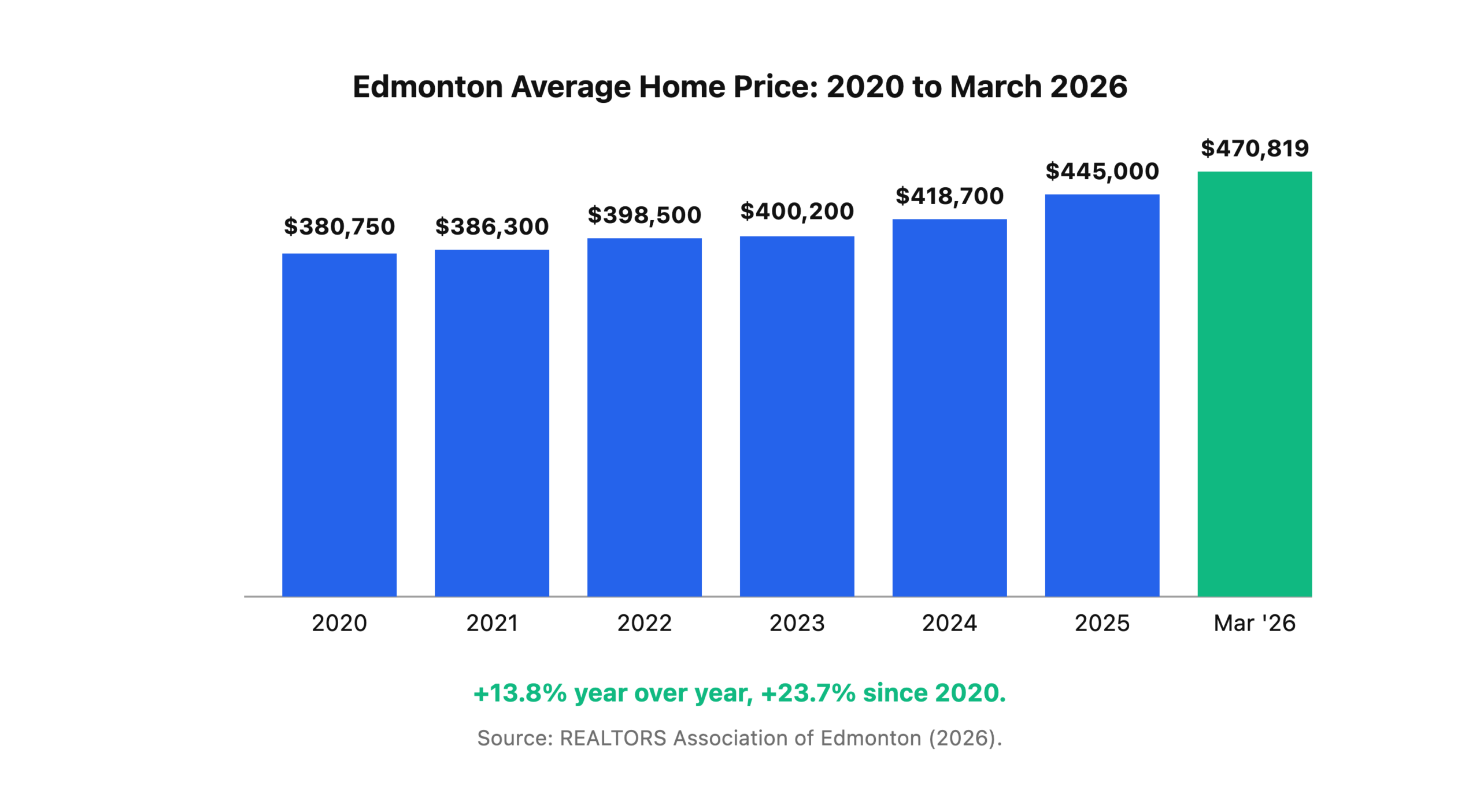

How Much Has Edmonton Home Price Growth Actually Been?

Edmonton’s average home price rose from $380,750 in 2020 to $470,819 in March 2026, a 23.7% cumulative increase — noticeably slower than Toronto or Vancouver but steady and recently accelerating (REALTORS Association of Edmonton, 2026). The last 12 months alone posted a 13.8% year-over-year gain as the migration-driven demand finally hit the resale market.

Edmonton sat nearly flat from 2020-2023 while Toronto and Vancouver doubled, then started catching up in late 2024. The March 2026 average of $470,819 is still 58% below Toronto and 62% below Vancouver for a comparable detached home — which is why the interprovincial migration story isn’t slowing.

How Do Edmonton’s Energy Economy and Downtown Rental Supply Affect the Decision?

Edmonton’s economy remains anchored to energy, which historically created 5-10 year boom-bust cycles in both rent and home prices (Government of Alberta, 2025). The 2026 market is different: energy employment is stable, the diversified tech and health sectors have grown 18% since 2021, and rental demand is driven by migration rather than oil-sands hiring.

Downtown vs Suburban Tradeoffs

Downtown Edmonton rentals remain softer than the suburbs because several large purpose-built towers came online in 2023-2024. A 1-bedroom downtown still rents for $1,200-$1,400, well below the city average. If you work downtown and value flexibility, renting downtown can still pencil out longer than in Terwillegar, Windermere, or Summerside, where 3-bedroom rents have climbed past $2,100.

The Energy Economy Risk

If oil prices crash and Edmonton hiring reverses, rents could soften faster than home prices — the opposite of what’s happened since 2022. We factor this into every client conversation, especially for clients in energy-adjacent roles. For stable public-sector or health-care clients, the energy downside case matters less.

For the tax-advantaged savings side of the plan, see our guides on the First Home Savings Account in Alberta and the RRSP Home Buyers’ Plan — both can add $30K-$100K to your down payment without touching your taxable income.

Ready to Run Your Own Edmonton Rent vs Buy Numbers?

Generic online calculators miss Edmonton-specific variables: the zero land transfer tax, the real property tax rates by neighbourhood, the CMHC premium on 5-10% down, and today’s actual broker rates. We run live rent-vs-buy scenarios for Edmonton and Calgary clients every week, free of charge, using your actual income and savings. Call 780-974-1270 or email info@MetroMortgageGroup.ca and we’ll build the numbers with you.

For the full buyer playbook, start with our complete Edmonton first-time home buyer guide. To plan the cash you’ll need on possession day, read our Alberta closing costs breakdown.

Frequently Asked Questions

What is the rent-vs-buy breakeven point in Edmonton in 2026?

The breakeven on a typical $470K Edmonton home with 5% down is roughly 3.5 years at current rates, meaning you need to stay in the home at least that long for buying to beat renting financially (REALTORS Association of Edmonton, 2026). Stay 5+ years and the buyer wins by roughly $75,000 in net wealth.

How much more does it cost per month to own vs rent in Edmonton?

On a 2-bedroom, owning a $470K home costs about $880/month more than renting a comparable unit at $1,630 (rentals.ca, 2026). But roughly $625 of that “extra” goes to principal (equity), so the real cost premium of ownership is closer to $255/month in year one — and shrinks every year as rents climb.

Are Edmonton home prices actually going up or is this a blip?

Edmonton home prices are up 13.8% year-over-year as of March 2026, the highest annual gain since 2006, driven by interprovincial migration and tight supply (REALTORS Association of Edmonton, 2026). Most Alberta economists expect another 4-7% gain in 2026-2027 before the market normalizes.

Is it smarter to keep renting and invest the difference in Edmonton?

Only if you actually invest the difference — most renters don’t. Even assuming 7% annual stock returns, a renter investing $880/month for 5 years ends with roughly $63,000 (Bank of Canada, 2026). An Edmonton buyer builds around $75,000 in housing wealth over the same window, and lives in their home the whole time.

What if mortgage rates drop in 2027?

If 5-year fixed rates drop from 4.49% to 3.99% in 2027, you can refinance or take a shorter-term fixed now and reset later (Bank of Canada, 2026). Waiting for lower rates often backfires — Edmonton home prices historically rise faster than rate drops save you on monthly payments, so the total cost of waiting usually exceeds the savings.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and has helped Edmonton and Alberta families secure mortgages since 2011. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: April 24, 2026