Apartment Building Mortgages in Alberta

5+ unit financing structured for cap rate, DSCR, and refinance flexibility

Alberta’s multi-family apartment sector attracted over $3.2 billion in investment volume in 2025, with Edmonton and Calgary registering cap rates between 4.00% and 5.50% — among the widest yield spreads in any major Canadian market (CBRE Canada Market Outlook, 2025). For investors eyeing apartment buildings in this province, the financing decision — CMHC insured, conventional bank, or private bridge — determines more about your return profile than the purchase price itself. Getting the capital structure right on an Alberta apartment building is the single highest-leverage decision you’ll make.

Key Takeaways

– CMHC MLI Select allows as little as 5% down, 50-year amortization, and 10-year fixed terms on qualifying Alberta apartment buildings with affordability, energy, or accessibility commitments (CMHC, 2025).

– Conventional bank financing requires 25-35% down with a 1.20+ DCR and 25-year amortization — faster to close but significantly more equity-intensive.

– Private/MIC bridge lending fills gaps for value-add, low-occupancy, or quick-close deals at 8-12% rates with 12-24 month terms.

– Edmonton cap rates of 4.00-5.50% on stabilised B/C-class buildings make CMHC leverage especially powerful — the spread between cap rate and borrowing cost drives cash-on-cash returns north of 12% on well-structured deals.

Step 1: Determine Your Building Classification

Before you approach a single lender, you need to know which financing lane your building falls into. In Canada, any residential property with 5 or more self-contained units is classified as multi-family commercial and underwritten on the building’s cash flow, not just personal income (CMHC, 2025). Four units and under stays residential. That fifth unit changes everything — the lender desk, the documentation, the down payment, and the timeline.

Alberta apartment buildings generally fall into four categories:

- Small walk-ups (5-12 units): Wood-frame or concrete block, built 1960s-1980s, common in Edmonton’s mature neighbourhoods like Oliver, Strathcona, and Bonnie Doon

- Mid-size apartments (13-40 units): Scattered across Edmonton, Calgary, Red Deer, and Lethbridge — the sweet spot for private investors

- Larger buildings (41-100+ units): Institutional-grade assets in Edmonton’s core, Calgary’s Beltline, and major suburban nodes

- Purpose-built rentals (PBR): New construction, often the strongest candidates for MLI Select financing

Each category carries different lender appetite, cap rate expectations, and financing paths. A 6-unit walk-up in Millwoods and a 60-unit mid-rise in Oliver sit in completely different underwriting conversations, even though both are technically “apartment building mortgages.” See our multi-family mortgage Edmonton guide for the full 5+ unit framework.

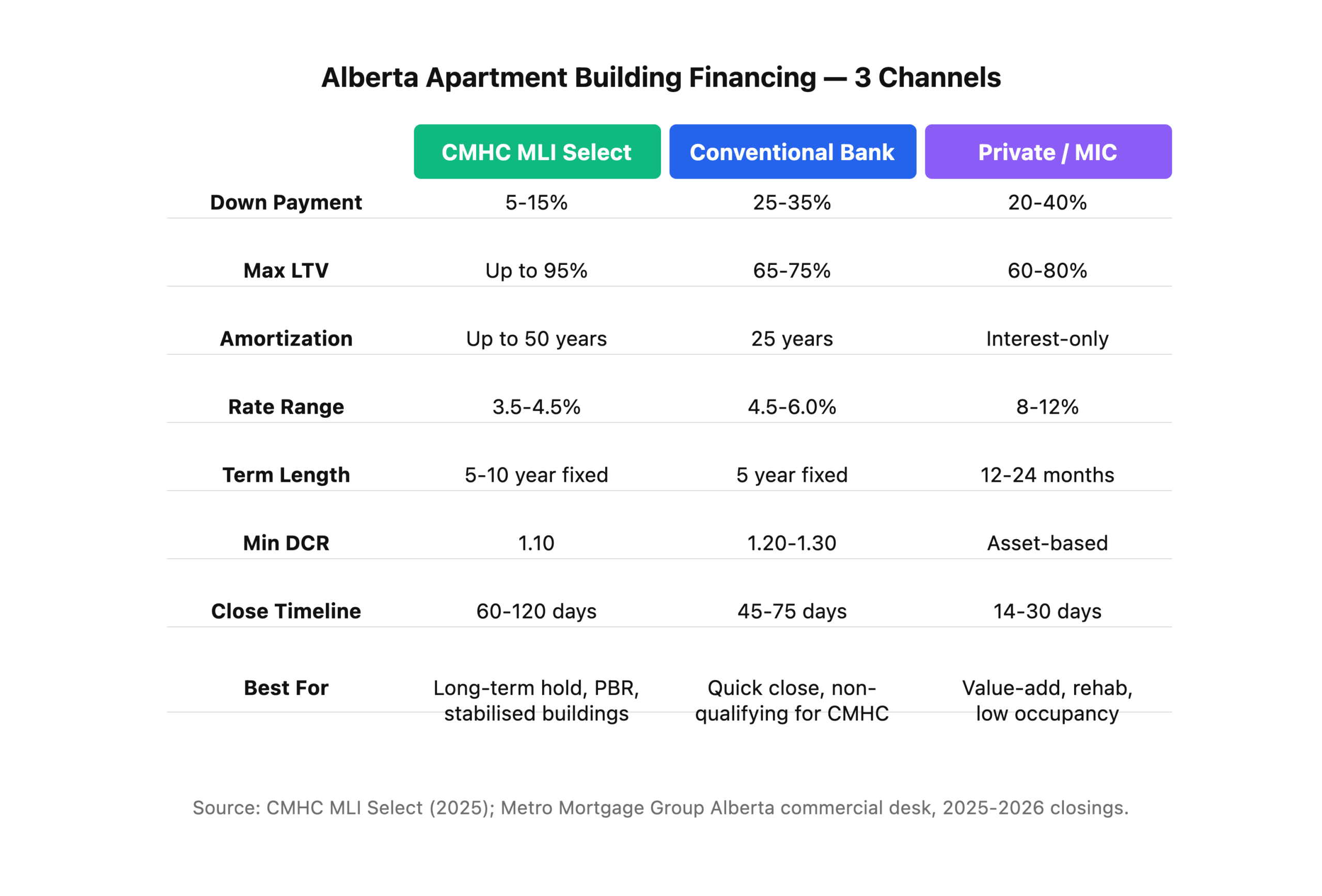

Step 2: Understand the Three Financing Channels

Every Alberta apartment building deal runs through one of three channels — or sometimes a combination if the deal involves a bridge-to-CMHC strategy. Here’s how they compare head to head:

The channel you choose depends on three variables: how much equity you have, how fast you need to close, and whether the building qualifies for CMHC insurance. Most sophisticated investors know which channel before they write the offer. See our commercial mortgages Edmonton guide for the broader picture.

Step 3: Qualify Through CMHC MLI Select (the Best Path)

CMHC MLI Select is the most powerful financing tool available for Alberta apartment buildings in 2026. The program awards points across three categories — Affordability, Energy Efficiency, and Accessibility — and higher point totals unlock deeper insurance premium discounts, longer amortizations, and higher LTV ratios (CMHC, 2025).

How the point tiers work

- 50 points: Up to 85% LTV, 40-year amortization, 10% premium discount, 1.10 DCR

- 70 points: Up to 90% LTV, 45-year amortization, 20% premium discount, 1.10 DCR

- 100 points: Up to 95% LTV, 50-year amortization, 30% premium discount, 1.10 DCR

Earning points isn’t complicated, but it requires commitments that are registered on title. Affordability points come from renting a portion of units at or below median market rent for the area. Energy efficiency points come from meeting or exceeding energy performance targets (NRCAN EnerGuide, ENERGY STAR, Passive House). Accessibility points come from building or retrofitting units to accessibility standards beyond code minimums.

For Alberta specifically, CMHC has prioritised communities experiencing rapid population growth — Edmonton’s metro area added over 50,000 residents in 2024 alone (Statistics Canada, 2025). Projects in high-need areas receive priority consideration during the CMHC underwriting queue, which can shorten the approval timeline by 2-4 weeks.

What CMHC MLI Select requires from you

- Minimum 5 self-contained residential units

- Net worth equal to at least 25% of the loan amount

- Personal credit score typically 680+ on the sponsoring individual

- Debt Coverage Ratio of at least 1.10 (net operating income / annual debt service)

- Environmental Phase 1 ESA (Phase 2 if flagged)

- Building Condition Assessment for buildings over ~25 years old

- CMHC application fee plus the insurance premium (often capitalisable into the mortgage)

The insurance premium on a full-points MLI Select file runs roughly 1.50-2.50% of the loan amount after the discount — a one-time cost that’s typically added to the mortgage balance. On a $3M loan, that’s $45,000-$75,000 in premium versus $750,000+ in additional equity you’d need on a conventional deal requiring 25% more down. The math heavily favours the insured path for long-term holders. See our multi-family mortgage Edmonton guide for the full MLI Select point-tier breakdown.

Step 4: Evaluate Conventional Bank Financing

Conventional bank financing makes sense when a deal doesn’t qualify for CMHC — short-term holds, value-add repositioning, occupancy under 85%, or borrowers who want to avoid the 45-60 day CMHC application queue (CMHC, 2025). Banks are faster and more flexible on non-standard deals, but they demand significantly more equity.

Typical conventional bank terms on an Alberta apartment building in 2026:

- Down payment: 25-30% on stabilised buildings, 30-35% on value-add

- Amortization: 25 years maximum

- Term: 5-year fixed, priced on the GOC 5-year bond plus 175-250 bps

- DCR requirement: 1.20-1.30 minimum

- Personal guarantee: Required from all principals

- Closing timeline: 45-75 days from application to funding

The Big Six commercial desks — RBC, TD, BMO, Scotiabank, CIBC, and National Bank — all have Alberta commercial real estate teams, but appetite varies meaningfully by deal size. Most Big Six banks aren’t competitive on deals under $3-5M because the underwriting cost doesn’t justify the revenue. Below that threshold, credit unions like Servus and ATB Financial often bid more aggressively on Edmonton and Calgary apartment deals.

One advantage of conventional financing: you can close 2-4 weeks faster than a CMHC file, which matters if you’re competing against other buyers on a tight conditional period. Some investors use a conventional commitment as a backup plan while the CMHC application runs in parallel.

Step 5: Consider Private/MIC Bridge Lending

Private mortgage investment corporations (MICs) and bridge lenders fill a specific gap in the Alberta apartment market: deals that need to close in 14-30 days, properties with occupancy below CMHC’s threshold, or buildings requiring significant capital improvements before they’ll qualify for permanent financing.

Expect these terms on a private Alberta apartment building mortgage:

- Down payment: 20-40%, depending on the MIC and the deal’s risk profile

- Rate: 8-12% annually, often interest-only

- Term: 12-24 months, with extensions available at additional cost

- Fees: 1-3% lender fee plus broker fee, legal costs, and appraisal

- Closing speed: As fast as 14 days with clean title and appraisal

Private lending is expensive by design — it’s short-term capital for specific situations. The classic use case is a bridge-to-CMHC strategy: buy a building with private money, stabilise occupancy to 85%+, complete any deferred maintenance, then refinance into CMHC MLI Select at dramatically lower rates and much higher leverage. Done correctly, the investor recovers most or all of their initial equity on the refinance.

Metro’s commercial team structures these bridge-to-permanent strategies for clients across Edmonton, Calgary, Red Deer, and Lethbridge. The key is structuring the private loan with a realistic exit timeline — 12 months is tight for a full stabilisation and CMHC refinance, while 18-24 months provides a more comfortable runway.

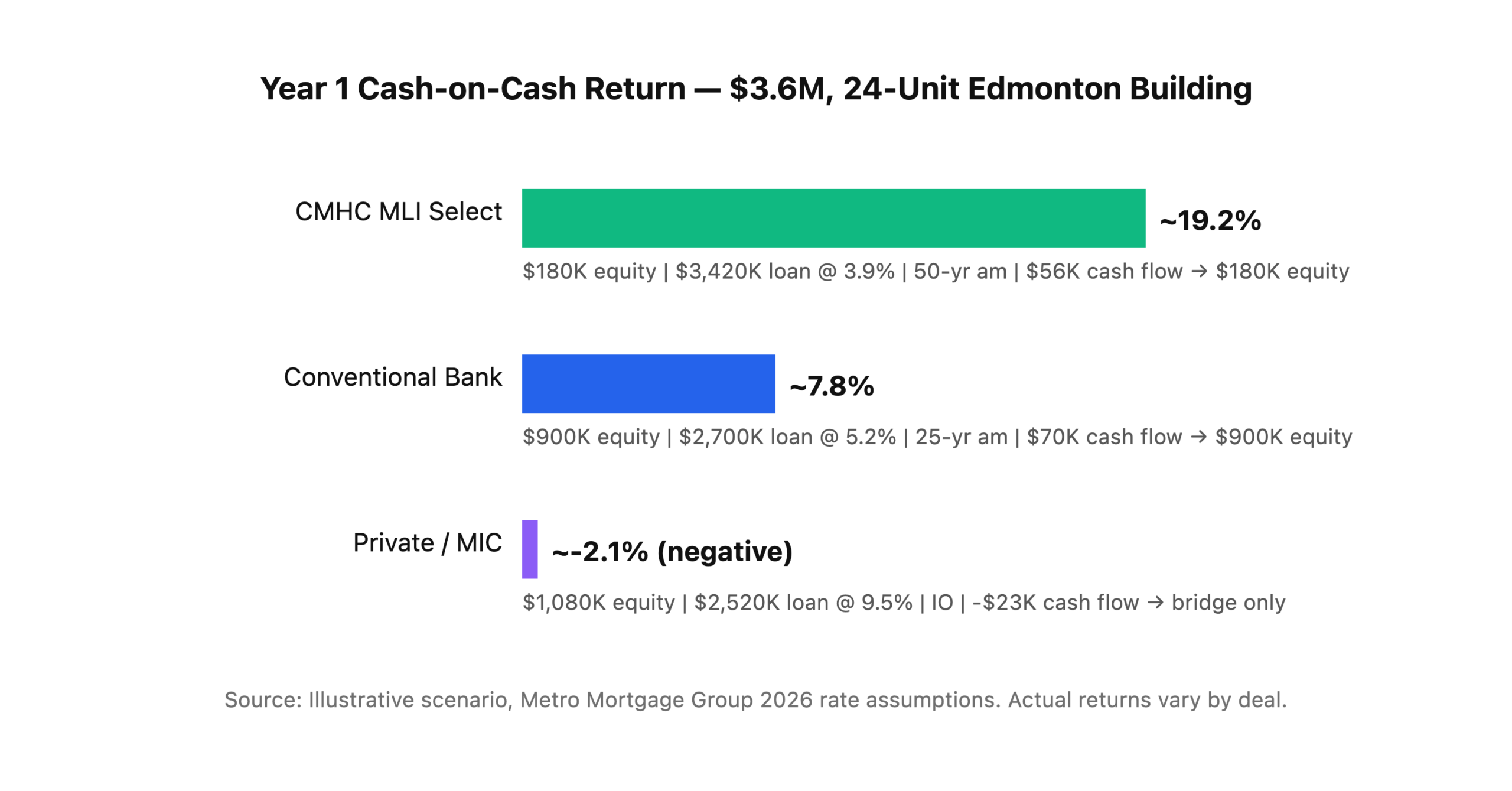

Step 6: Run the Cap Rate and Cash-on-Cash Analysis

The financing channel you choose directly determines your cash-on-cash return, and the difference between channels is dramatic on the same building. Alberta apartment cap rates currently range from 4.00% to 5.50% on stabilised B/C-class product in Edmonton and Calgary, with the wider end of that range sitting in secondary markets and older building stock (CBRE Canada, 2025).

Let’s run a hypothetical scenario on a 24-unit stabilised apartment building in Edmonton, purchased at $3,600,000 with a 5.25% cap rate and $189,000 NOI, purely to illustrate how the three financing channels compare on the same building:

The CMHC path produces a cash-on-cash return roughly 2.5x the conventional path on the same building, because the combination of lower down payment, longer amortization, and lower rate compresses equity requirements while expanding cash flow. Private lending shows a negative year-one cash flow because it’s not designed for permanent hold — it’s bridge capital with an exit strategy built in.

This is exactly why the financing conversation needs to happen before the purchase negotiation. The “right” price for an apartment building depends entirely on which capital channel you can access — see our down payment Alberta guide for residential down payment context.

Step 7: Prepare Your Documentation Package

Whether you’re pursuing CMHC, conventional, or private financing, Alberta apartment building lenders need a comprehensive package. Missing even one document can delay your close by weeks. Here’s the complete checklist:

Property documents:

– Current rent roll with unit numbers, rents, lease terms, vacancy, and arrears

– Trailing 12-month income and expense statements (or T776 for smaller buildings)

– 2-3 years of historical financials to establish expense trends

– Property tax assessment from the municipality

– Insurance certificate showing replacement cost coverage

– Utility bills (12-month history if owner-paid)

Building condition documents:

– Environmental Phase 1 ESA (mandatory for CMHC; strongly recommended for all channels)

– Building Condition Assessment (BCA) for buildings over ~25 years old

– Commercial appraisal ordered by the lender ($3,500-$7,500 depending on building size)

– Capital expenditure plan if the building needs major systems work

Borrower documents:

– Personal net worth statement and 2 years of T1 personal tax returns

– Corporate documents if purchasing through a holdco, LP, or SPE

– Property management plan (or self-management track record)

– Resume of real estate holdings if you own other investment properties

The Debt Coverage Ratio (DCR) is the number that makes or breaks every apartment building deal. It measures whether the building’s net operating income covers the mortgage payment. Banks want 1.20+, CMHC accepts 1.10+. Running this calculation correctly — with realistic vacancy (5-7% in Edmonton, higher in Calgary given recent supply additions) and normalised expenses — is the first thing any experienced commercial broker does before submitting.

Step 8: Choose the Right Broker for Alberta Apartment Deals

A commercial mortgage broker typically shops 6 to 15 lenders on every Alberta apartment building file — CMHC-approved lenders, chartered banks, credit unions, life companies, and MICs. In Metro’s experience, the resulting spread on rate, LTV, and amortization can meaningfully shift a deal’s IRR. Going direct to a single bank means accepting that bank’s appetite on that specific day, which rarely produces the best structure.

The Alberta CMHC-approved lender landscape includes First National, MCAP, Equitable, CMLS, Peoples Trust, and several others. Big Six commercial desks compete on larger files but often don’t bid aggressively under $5M. Credit unions like Servus and ATB Financial have meaningful Alberta apartment appetite, particularly for owner-operator deals and buildings outside Edmonton and Calgary.

What separates a good commercial broker from a great one is knowing which lender wants which deal this quarter. Appetite shifts constantly based on each lender’s portfolio concentration, capital allocation, and CMHC quota. A broker who closed an MLI Select deal last month knows exactly which approved lender has room for another file — and which ones have hit their quarterly cap and aren’t bidding.

Nelson’s 9+ years of construction experience adds a layer that most mortgage brokers can’t replicate: he can read a Building Condition Assessment, assess capital expenditure risk, and have an informed conversation with CMHC underwriters about building envelope, mechanical systems, and energy retrofit feasibility. That matters on older Alberta apartment stock where deferred maintenance is the hidden variable that kills deals.

Alberta Market Context: Why Apartment Buildings Are Attractive in 2026

Edmonton’s multi-family fundamentals heading into 2026 are among the strongest in Canada. The metro area added over 50,000 residents in 2024 (Statistics Canada, 2025), driven by interprovincial migration and international immigration. That population growth is translating directly into rental demand — Edmonton vacancy rates on purpose-built rentals sat at roughly 2.5-3.5% through late 2025, tight enough to support rent growth but not so tight that new supply can’t be absorbed.

Calgary’s apartment market tells a slightly different story. Vacancy spiked from 1.4% in 2023 to roughly 4.8% in 2024 as a wave of new purpose-built rental supply hit the market simultaneously (CBRE Canada, 2025). That higher vacancy is compressing NOI on some buildings and creating buying opportunities for investors who can stomach a 12-18 month lease-up period. Cap rates in Calgary are widening slightly, which favours purchasers willing to deploy patient capital.

Secondary Alberta markets — Red Deer, Lethbridge, Medicine Hat, Grande Prairie — offer even wider cap rates (often 6.0-7.5%) but come with thinner tenant pools and fewer lender options. CMHC will still insure in these markets, and Servus Credit Union is often the most competitive conventional option outside the two major cities.

The bottom line: Alberta’s combination of population growth, relatively affordable entry prices compared to Vancouver or Toronto, and accessible CMHC financing makes it one of the best apartment building investment markets in Canada right now. The financing strategy just needs to match the hold period and the investor’s equity position. See our current rate benchmarks for where commercial rates sit today.

Frequently Asked Questions

What’s the minimum building size for CMHC apartment building insurance in Alberta?

CMHC multi-family insurance requires a minimum of 5 residential units per property. Buildings with 4 or fewer units are financed under residential mortgage rules with different down payment thresholds and underwriting criteria (CMHC, 2025). There’s no upper unit limit — CMHC regularly insures Alberta buildings from 5-unit walk-ups to 300+ unit purpose-built rentals.

Can I buy an Alberta apartment building in a corporation?

Yes, and most experienced investors do. Lenders generally accept purchases through a single-purpose entity (SPE) or holding corporation, with personal guarantees from the principals (CMHC, 2025). Structuring ownership correctly up front matters for tax treatment, liability protection, and future refinance flexibility. Always consult your accountant before drafting the offer.

How long does CMHC MLI Select take to close in Alberta?

Plan on 60 to 120 days from application to funding — roughly 30-45 days for CMHC underwriting plus another 30-60 days for lender funding, appraisal, environmental, and legal work (CMHC, 2025). Always negotiate purchase conditions that reflect this timeline. Conventional bank financing closes faster at 45-75 days, and private bridge can fund in as few as 14 days.

Is CMHC MLI Select available on existing buildings, or only new construction?

MLI Select applies to purchase, refinance, and construction of 5+ unit residential buildings, including existing properties (CMHC, 2025). Existing Alberta apartment buildings typically earn points through affordability commitments (renting units below median market rent) and post-closing energy retrofits. Refinancing an existing rental building into MLI Select is one of the most powerful equity recapture strategies available.

What cap rate should I target for an Alberta apartment building?

Edmonton stabilised B/C-class buildings are currently trading at 4.00-5.50% cap rates, while Calgary sits in a similar range with slightly wider spreads due to higher vacancy (CBRE Canada, 2025). Secondary markets offer 6.0-7.5% cap rates with thinner liquidity. The “right” cap rate depends on your financing channel — a 5.25% cap rate building financed at 3.9% through CMHC generates strong positive leverage, while the same building at 5.2% conventional financing compresses returns significantly.

Ready to Finance Your Next Alberta Apartment Building?

Apartment building financing in Alberta rewards preparation and lender access. The difference between a bank’s first offer and the best CMHC MLI Select structure on the same building is often six figures of equity and several points of cash-on-cash return. Metro’s commercial desk runs full financing scenarios on Alberta 5+ unit deals every week — purchase, refinance, and construction — across every CMHC-approved lender, bank, credit union, and MIC in the province. Call 780-974-1270 or email info@MetroMortgageGroup.ca to walk through your file.

Start with the multi-family mortgage Edmonton guide for the full 5+ unit framework, or check our current rate benchmarks to see where commercial rates sit today.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and leads the firm’s commercial and multi-family practice across Edmonton and Calgary. With Nelson Sousa’s 9+ years of construction industry experience supporting the commercial desk, Metro brings both financing expertise and building knowledge to every apartment deal. Metro Mortgage Group has served Alberta investors and owner-operators since 2011 with 229 five-star Google reviews.

Last updated: June 16, 2026