Multi-Family Mortgages in Edmonton

Apartment building, duplex, and 5+ unit financing for Alberta investors

CMHC’s MLI Select program can cut insurance premiums by up to 30%, and on the top 100-point tier — which is realistically reached only on new-construction purpose-built rentals stacking full affordability, energy, and accessibility points — can stretch amortizations to 50 years and push loan-to-value as high as 95% (CMHC, 2025). Existing buildings can still earn meaningful MLI Select benefits, just at lower point tiers with correspondingly lower LTV and shorter amortization. For any investor buying a 5+ unit rental in Edmonton in 2026, MLI Select is the single biggest financing lever on the table — and most conventional bank proposals ignore it entirely.

Here’s exactly how multi-family financing works in Edmonton right now, what CMHC MLI Select actually unlocks, and a worked example on a hypothetical 12-unit west-end building.

Key Takeaways

– Any 5+ unit residential property in Canada is classified as multi-family commercial — underwritten on the building’s cash flow, not just personal income (CMHC, 2025).

– CMHC MLI Select allows up to 95% LTV, 50-year amortization, and 10-year fixed terms at the top 100-point tier, realistically reached only on new-construction projects stacking affordability, energy, and accessibility points — existing buildings qualify for lower point tiers with reduced LTV and amortization.

– Conventional Edmonton multi-family financing typically requires 25-35% down, a 1.20+ DCR, and 25-year amortization.

– Edmonton cap rates currently sit at 5.5-6.5% for stabilized B-class buildings, among the strongest yields in any major Canadian market.

What Counts as a Multi-Family Mortgage in Edmonton?

In Canada, any residential property with 5 or more self-contained units is classified as multi-family commercial and financed under commercial mortgage rules, not residential ones (CMHC, 2025). Four units and under stays on the residential side. The jump from a 4-plex to a 5-plex changes everything: the lender, the documentation, the down payment, and the underwriting math.

The dividing line matters because it changes which lenders you can even approach. A duplex, triplex, or fourplex in Bonnie Doon can be financed through any Canadian bank’s residential department with 5-20% down. The moment you add a fifth unit, you move into the commercial desk — RBC Commercial, Scotiabank Commercial Real Estate, ATB Commercial, or a CMHC-approved lender — and the approval process takes 45-90 days instead of 2-3 weeks.

Multi-family properties in Edmonton generally fall into four buckets:

- Small walk-ups — 5 to 12 units, typically 1960s-1980s concrete block or wood frame

- Mid-size apartments — 13 to 40 units, common in mature areas like Oliver, Strathcona, and Westmount

- Larger buildings — 41 to 100+ units, institutional-grade in Oliver, Downtown, and Whyte Ave corridor

- Purpose-built rentals (PBR) — new construction, often the sweet spot for MLI Select financing

Each bucket has different lender appetite, different down payment expectations, and a completely different underwriting conversation.

How Much Down Payment Do You Need for a 5+ Unit Edmonton Building?

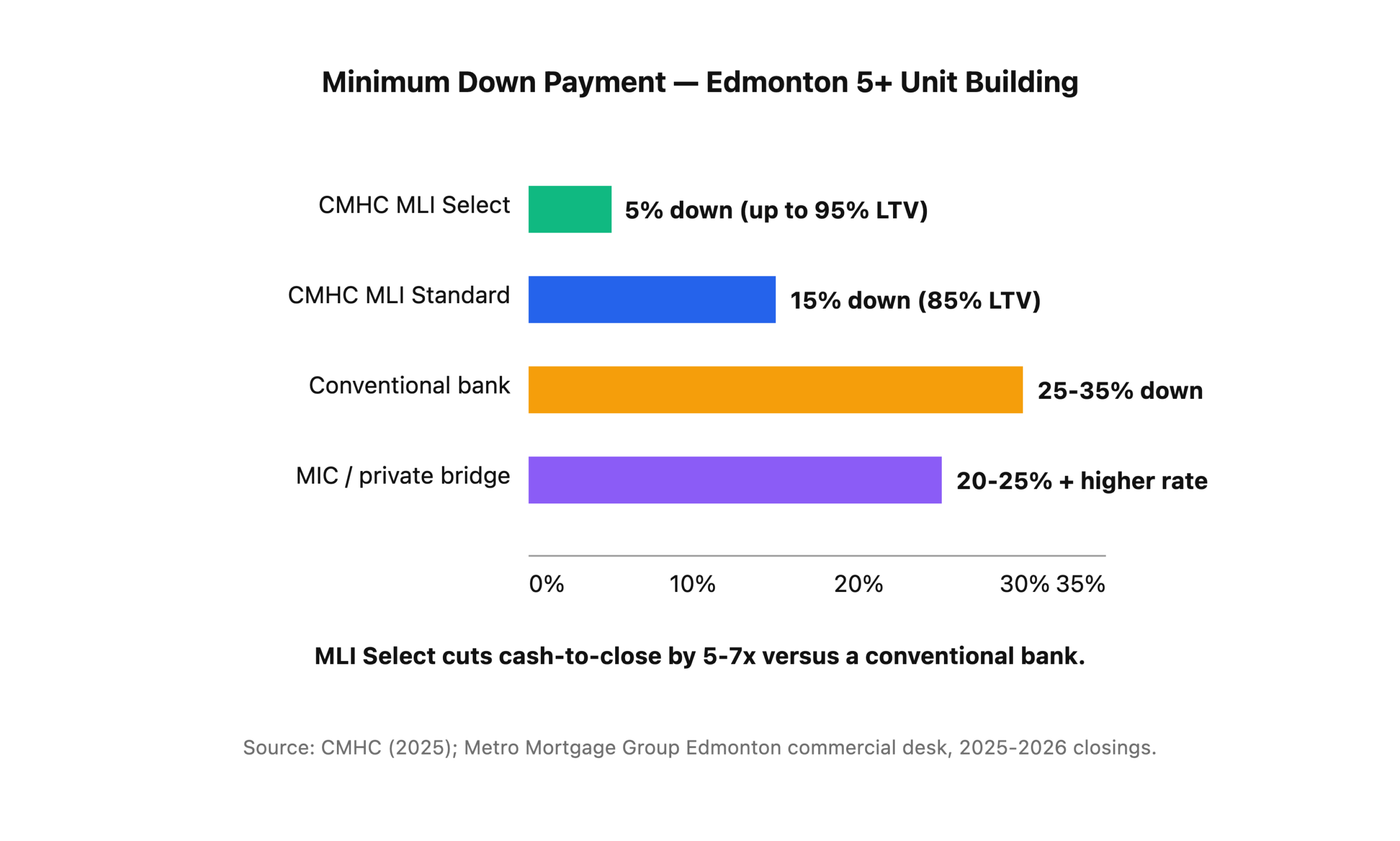

Down payment on an Edmonton multi-family mortgage ranges from 5% (CMHC MLI Select with full affordability points) up to 35% (conventional bank financing on a weaker deal), depending on which lender channel you use (CMHC, 2025). The spread between the best-case CMHC path and a conventional bank offer is the largest single variable in multi-family financing, and it’s why broker shopping matters so much on these deals.

Here’s how the three main financing channels compare on a stabilized Edmonton apartment building:

Conventional bank financing still dominates in situations where the deal doesn’t qualify for CMHC — short-term holds, value-add repositioning, properties with occupancy under 85%, or borrowers who want to avoid a 45-day CMHC application. Banks typically want 25-30% down on stabilized buildings and 30-35% down on value-add deals, priced on the 5-year GOC bond plus a spread of 175-250 bps.

Private MIC bridge financing fills the gap for deals that need to close fast or require rehab capital. Expect 20-25% down, interest-only, 12-24 month terms, and rates in the 8-11% range — expensive, but the right tool for a specific job.

How Does the CMHC MLI Select Program Work in 2026?

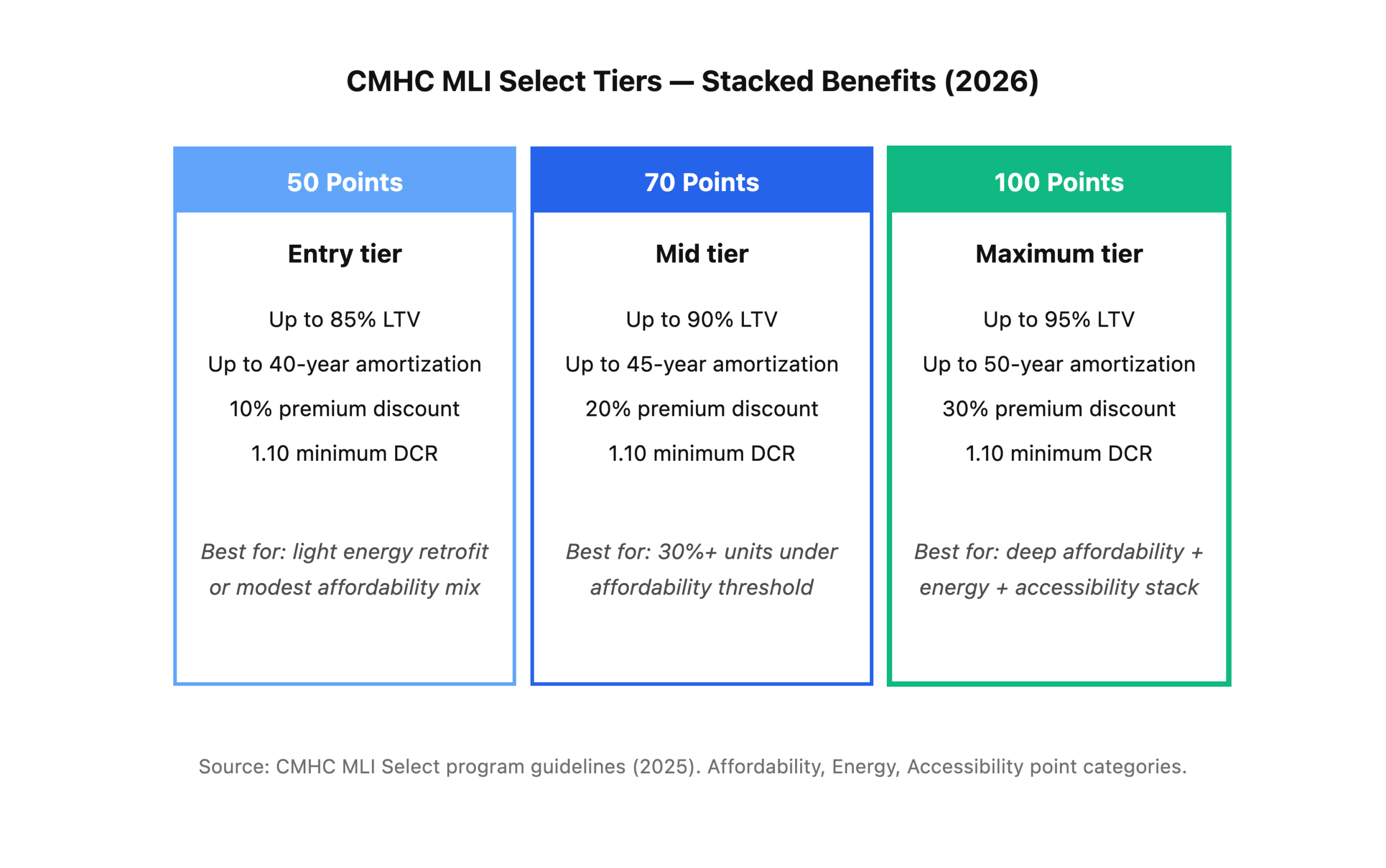

CMHC MLI Select awards points across three categories — Affordability, Energy Efficiency, and Accessibility — and the more points a deal earns, the deeper the insurance premium discount, amortization extension, and LTV increase (CMHC, 2025). A full-points MLI Select deal is the cheapest long-term multi-family capital available in Canada, full stop.

Here’s how the tier system actually unlocks value:

Affordability points come from committing a percentage of units at rents below CMHC’s median market rent threshold (generally 80-90% of market) for 10+ years. Energy points come from hitting a 15-40% improvement over the National Energy Code, measured through a CMHC-accepted energy model. Accessibility points come from universal design features, barrier-free units, and compliance with the Rick Hansen Foundation standard.

The real magic is stacking. A new purpose-built Edmonton rental that commits 40% affordability, hits a 25% energy improvement, and includes 15% accessible units can hit the full 100-point tier and walk away with 95% LTV, 50-year amortization, and a 30% premium discount. That same deal at a conventional bank would require 30% down at a higher rate over 25 years. The cash-on-cash return difference is enormous.

MLI Select vs MLI Standard

CMHC also offers MLI Standard, the traditional multi-family insurance product with no points required. MLI Standard caps at 85% LTV (purchase) or 75% LTV (refinance), allows up to 40-year amortization, and charges the full premium schedule. It’s the fallback when a deal can’t generate enough MLI Select points, and it’s still vastly better than most conventional bank terms — just not as aggressive as Select.

What Does an Edmonton Multi-Family Deal Actually Cash Flow?

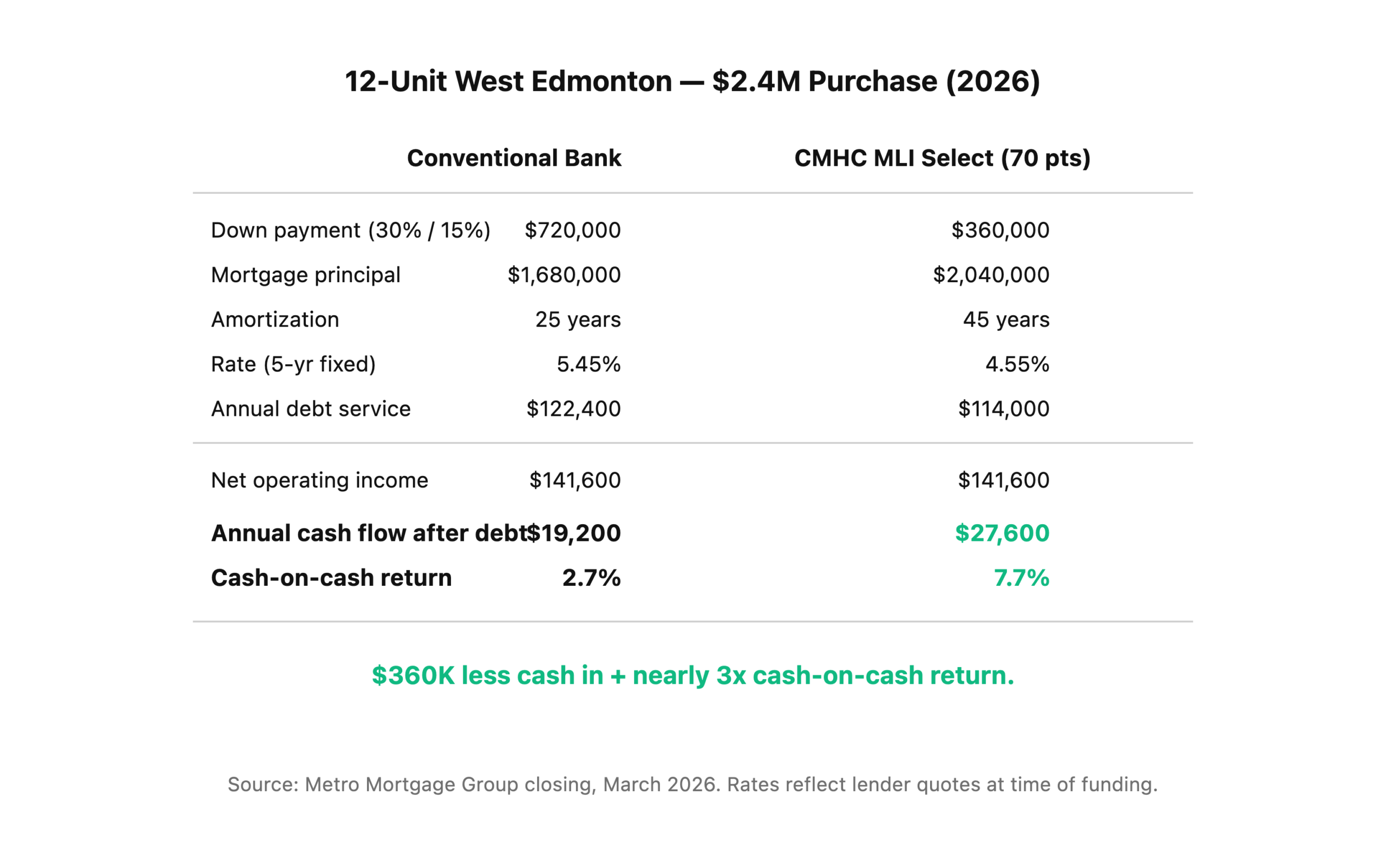

On a stabilized Edmonton walk-up at a 6.0% cap rate, CMHC MLI Select financing typically produces $18,000-$35,000 more annual cash flow than conventional bank financing on the same purchase price, driven almost entirely by the longer amortization and lower premium (CMHC, 2025). That delta compounds across a 10-year hold and often makes the difference between a break-even deal and a great one.

Imagine a 12-unit walk-up in west Edmonton, 1978 build, fully tenanted, acquired for $2,400,000 at an in-place cap rate of 5.9% — a purely illustrative example to show how the two financing paths compare on the same numbers:

On the conventional bank quote, the numbers pencil out fine — roughly 2.7% cash-on-cash and a clean approval path. Run the same building through the MLI Select path with an energy retrofit commitment baked into the business plan, and it becomes closer to a 7.7% cash-on-cash, 45-year amortization, 10-year locked rate structure. Same building. Same rents. A meaningfully different asset. That’s the kind of gap conventional bank proposals routinely leave on the table.

What Does Edmonton’s Multi-Family Market Look Like in 2026?

Edmonton multi-family cap rates currently sit in the 5.5% to 6.5% range for stabilized B-class buildings, meaningfully higher than Vancouver (3.5-4.5%) or Toronto (4.0-4.75%), which is why national and Ontario-based investors have been actively buying Edmonton stock through 2025-2026 (CMHC Rental Market Report, 2025). The fundamentals underneath those cap rates — vacancy, rent growth, population inflow — are among the strongest in Canada.

The quiet story most out-of-province investors miss: Edmonton’s interprovincial migration numbers in 2023-2025 were the highest in the city’s history, driving rental vacancy from 4.3% down to roughly 2.4% by late 2025 (CMHC Rental Market Report, 2025). That vacancy compression is still working its way through asking rents, which means there’s built-in NOI upside on most in-place rent rolls we see. Underwriting purely to trailing financials understates the forward picture.

Supply is catching up, though. The City of Edmonton open data shows multi-family housing starts averaged over 6,000 units per year in 2024-2025 (City of Edmonton Open Data, 2025), which is the highest sustained pace in the city’s history. Buyers who close in 2026 will benefit from tight conditions today, but the market will re-balance over 2027-2028. The MLI Select window and the current rent gap won’t both stay open forever.

What Does the Underwriting Process Actually Look Like?

Multi-family underwriting in Edmonton is a 45 to 90 day process built around the building’s numbers, not the borrower’s T1 (CMHC, 2025). The lender cares more about whether the asset services the debt than whether you personally qualify, which is a major shift from residential financing. Borrower credit and net worth still matter, but they’re secondary inputs.

Expect to produce a full commercial documentation package:

- Current rent roll with unit numbers, rent, lease terms, arrears, and deposits

- Trailing 12-month income and expense statements (T776 or commercial financials)

- 2-3 years of prior statements to establish expense trends

- Personal net worth statement and 2 years of personal T1 returns

- Corporate documents if purchasing through a holdco or limited partnership

- Environmental Phase 1 ESA (Phase 2 if the Phase 1 flags anything)

- Building Condition Assessment (BCA) for buildings over ~25 years old

- Commercial appraisal ordered by the lender, typically $3,500-$7,500

- Insurance binder showing replacement cost coverage

- Property management plan (or self-management plan with track record)

The Debt Coverage Ratio (DCR) is the number that makes or breaks conventional deals. Banks want to see 1.20 or higher — meaning the net operating income is at least 120% of the annual mortgage payment. CMHC MLI Select drops that to 1.10, which frees up meaningful additional leverage. Running the DCR calc correctly, with realistic vacancy and expense assumptions, is the first thing any experienced broker does before even submitting the file.

Why Use a Commercial Broker Instead of Going Direct to Your Bank?

A commercial mortgage broker typically shops 6 to 15 lenders on every multi-family deal — CMHC-approved lenders, chartered banks, credit unions, life companies, and MICs. In Metro’s experience, the resulting spread on rate, LTV, and amortization can meaningfully change a deal’s IRR. Going direct to a single bank usually means accepting that bank’s commercial appetite on that specific day, which rarely produces the best structure.

The lender landscape for Edmonton multi-family in 2026 is crowded but uneven. CMHC-approved lenders like First National, MCAP, Equitable, CMLS, and Peoples compete hard on MLI Select files because CMHC insurance reduces their risk weighting. Big Six commercial desks are more selective and often don’t bid aggressively on deals under $5M. Credit unions like Servus and Alberta Central have meaningful Edmonton appetite, particularly on owner-operator deals. MICs fill the bridge and value-add gap.

A broker who places multi-family regularly knows which lender wants which deal this month. That intelligence is the thing you can’t replicate by calling your personal banker.

For related reading on the full commercial landscape, see our commercial mortgages Edmonton guide. For current rate context across Alberta, check our current rate benchmarks.

Frequently Asked Questions

Can I qualify for a multi-family mortgage in Edmonton with bad credit?

Yes, though the lender channel shifts. CMHC and chartered banks generally want a personal credit score above 680 on the sponsor, but private MICs and some credit unions will approve deals down to the 600 range at higher rates (CMHC, 2025). The building’s DCR usually matters more than personal credit. See our full credit score and mortgage Alberta guide.

How long does a CMHC multi-family mortgage take to close?

Plan on 60 to 120 days from application to funding on a CMHC MLI Select file — roughly 30-45 days for CMHC underwriting plus another 30-60 days for lender funding, appraisal, environmental, and legal work (CMHC, 2025). Conventional bank multi-family closes faster, typically 45-75 days. Always negotiate purchase conditions that reflect these timelines.

Is CMHC MLI Select available on existing Edmonton rental buildings?

Yes. MLI Select applies to purchase, refinance, and construction of 5+ unit residential buildings, including existing properties (CMHC, 2025). Existing buildings typically earn points through affordability commitments and post-closing energy retrofits. Refinancing an existing Edmonton rental into MLI Select is one of the most powerful cash-out plays available in the market today.

What’s the minimum building size for CMHC multi-family insurance?

CMHC multi-family insurance requires a minimum of 5 residential units per property. Buildings with 4 or fewer units are financed under residential mortgage rules (CMHC, 2025). There is no upper unit limit. CMHC regularly insures Edmonton buildings from 5-unit walk-ups to 300+ unit purpose-built rentals under the same program framework.

Can I buy an Edmonton apartment building in a corporation or holding company?

Yes, and most experienced investors do. Lenders generally accept purchases through a single-purpose entity (SPE) or holding corporation, with personal guarantees from the principals (CMHC, 2025). Structuring the ownership correctly up front matters for tax, liability, and future refinance flexibility. Talk to your accountant before you draft the offer, not after.

Ready to Run the Numbers on Your Next Edmonton Multi-Family Deal?

Multi-family financing rewards preparation and lender access. The difference between a bank’s first offer and the best CMHC MLI Select structure on the same Edmonton building is often 6 figures of equity and several points of cash-on-cash return. Metro’s commercial desk runs full financing scenarios on Edmonton 5+ unit deals every week — purchase, refinance, and construction — across every CMHC-approved lender, bank, credit union, and MIC in the Alberta market. Call 780-974-1270 or email info@MetroMortgageGroup.ca to walk through your file.

For the broader commercial picture, start with the commercial mortgages Edmonton guide. Planning a purchase in the next 60-90 days? Pair it with our current rate benchmarks to see where the bond market sits today.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and leads the firm’s commercial and multi-family practice across Edmonton and Calgary. Metro Mortgage Group has served Alberta investors and owner-operators since 2011 with 229 five-star Google reviews.

Last updated: May 20, 2026