Construction Mortgages in Alberta

Draw-stage financing for builders, developers, and custom-home buyers

Alberta recorded nearly 55,000 housing starts in 2025 — the highest number in at least 70 years — with Edmonton and Calgary both setting back-to-back annual records (CBC News, 2026; CMHC, 2026). Every single one of those projects needed construction financing, and the process looks nothing like a standard purchase mortgage. Funds don’t arrive in one lump sum on closing day. Instead, they’re released in stages — called draws — as the build progresses through inspections. Miss a milestone, and your money stops flowing.

I’m Nelson Sousa, co-owner of Metro Mortgage Group and a licensed mortgage broker in Alberta. Before I got into mortgages, I ran a construction company for more than 9 years. I’ve stood on both sides of the draw schedule — as the builder waiting for the cheque and as the broker structuring the financing. That dual perspective is exactly why I want to walk you through how construction mortgages actually work in this province.

Key Takeaways

– Alberta construction mortgages release funds through a progress draw system, typically in 4-6 stages tied to construction milestones like foundation, framing, lock-up, drywall, and completion.

– The Bank of Canada’s 2.25% overnight rate in 2026 has brought institutional construction loan rates to approximately 4.45% for qualified borrowers, per Metro’s own current lender pricing (Bank of Canada, 2026).

– Alberta’s Prompt Payment and Construction Lien Act requires a 10% statutory holdback on all payments, released after a minimum 60-day lien period (Government of Alberta, 2026).

– You’ll need a minimum 20-25% down payment for most construction mortgages, with lenders recommending a 15-20% contingency fund on top of that.

– CMHC’s Apartment Construction Loan Program offers terms up to 50-year amortization with interest-only payments during the build phase (CMHC, 2025).

What Is a Construction Mortgage?

A construction mortgage is a short-term loan designed to finance the building of a new home or major renovation, where the lender releases funds in stages as construction progresses rather than as a single lump sum (WOWA, 2026). Once the build is complete, you either convert to a standard mortgage (called a “completion mortgage” or “take-out mortgage”) or pay out the construction loan entirely.

Think of it this way: a regular mortgage is one transaction on one day. A construction mortgage is a series of transactions spread across 8-14 months, each one triggered by a physical inspection confirming that work has been completed to the lender’s standards.

Why does this matter? Because if you’re used to the simplicity of a standard purchase — make an offer, get approved, show up at the lawyer’s office — construction financing is going to feel like a fundamentally different process. It is.

For the broader picture, see our commercial mortgages Edmonton guide.

How Do Draw Schedules Work in Alberta?

The draw schedule is the backbone of every construction mortgage. It defines when money flows from the lender to you (through your lawyer), and ultimately to your builder. Here’s the typical Alberta draw schedule, broken down stage by stage.

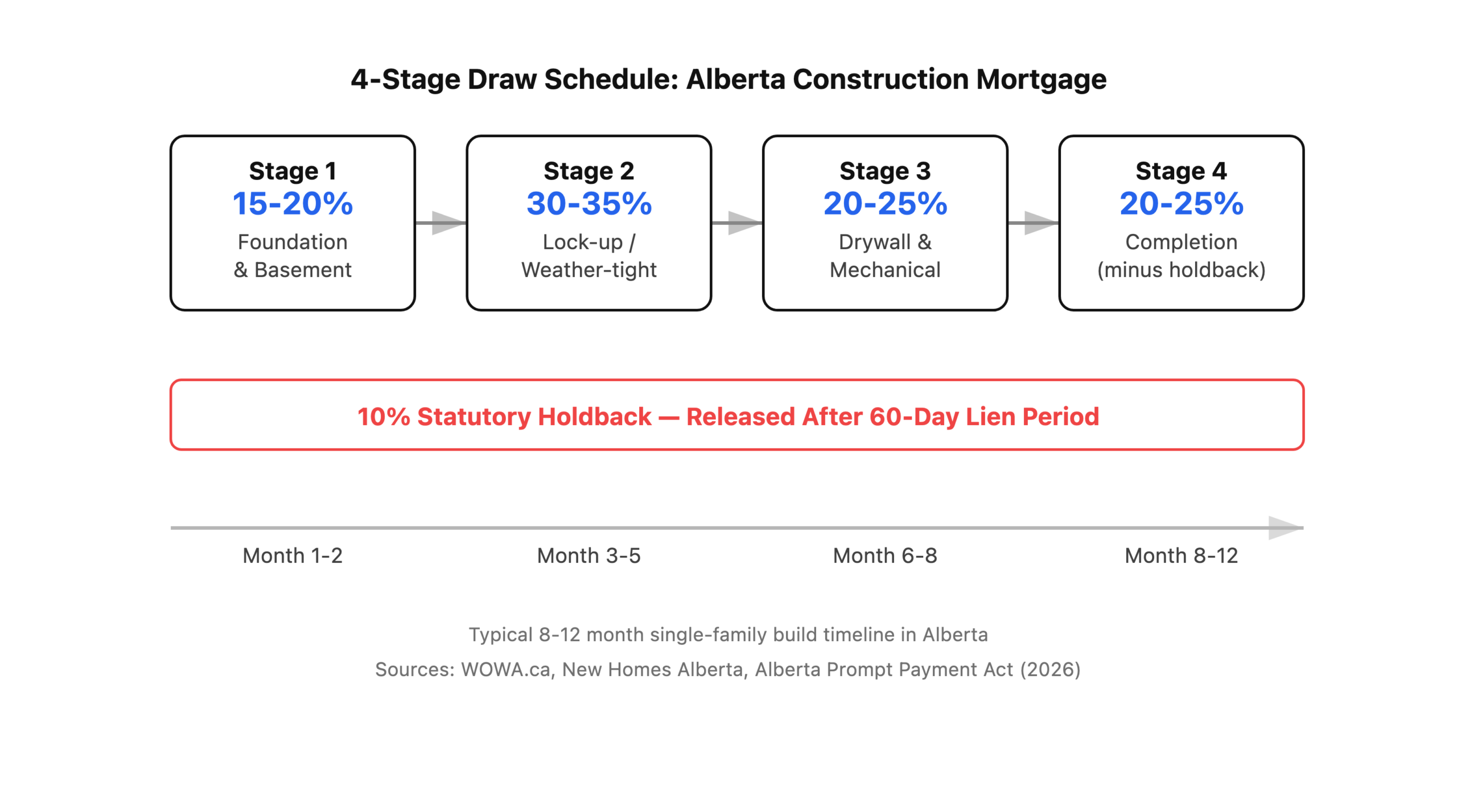

The Standard 4-Stage Draw

Most Alberta lenders use a 4-stage draw model for residential construction, though some offer 5 or 6 stages for larger or more complex builds (New Homes Alberta, 2026):

-

Foundation and basement (15-20% of total): Excavation complete, foundation poured and cured, weeping tile and waterproofing done, basement floor poured. The appraiser confirms the footprint matches approved plans.

-

Lock-up / weather-tight (30-35% of total): Framing complete, roof on, windows and exterior doors installed, house wrap applied. The structure is now protected from weather. This is usually the largest single draw.

-

Drywall and mechanical (20-25% of total): Plumbing, electrical, and HVAC roughed in and inspected by the municipality. Insulation installed, vapour barrier up, drywall hung and taped. Some lenders split this into two separate draws.

-

Completion (20-25% of total, minus holdback): Flooring, trim, cabinets, fixtures, final grading, landscaping deposit. The appraiser does a final inspection confirming the home is habitable and matches the original plans and specifications.

How Each Draw Gets Released

Here’s the process from my experience on both sides of the table. Your builder notifies you that a milestone is complete. The lender sends an independent appraiser to verify the percentage of completion. The appraiser files a report (e.g., “55% complete — consistent with lock-up stage”), and the lender calculates the draw amount: approved mortgage multiplied by percentage complete, minus previous draws and the 10% holdback. Funds go to your lawyer, who pays your builder on your behalf.

Why does the money go through a lawyer instead of straight to the builder? The lawyer confirms there are no liens on the property before releasing funds, and they hold the statutory holdback in trust.

Citation capsule: Alberta construction mortgage draw schedules typically release funds in 4-6 stages, with each draw requiring an independent appraisal confirming that construction progress matches the lender’s milestone requirements before funds are disbursed through the borrower’s lawyer (WOWA, 2026; New Homes Alberta, 2026).

The 10% Statutory Holdback: What Builders and Buyers Need to Know

Alberta’s Prompt Payment and Construction Lien Act (PPCLA) — which replaced the old Builders’ Lien Act for projects started after August 29, 2022 — requires property owners to retain 10% of every payment as a statutory holdback (Government of Alberta, 2026). This money sits in your lawyer’s trust account as a safety net for subtrades and suppliers who might not get paid by the general contractor.

When does the holdback get released? Once construction is substantially complete and a 60-day lien period has passed without any liens being registered against the property. Under the old Builders’ Lien Act, this window was 45 days — the PPCLA extended it to 60 days for projects started after August 2022 (Miller Thomson, 2025).

From my years running a construction company, I can tell you the holdback is one of the most misunderstood parts of the process. Builders price it into their cash flow projections — they know 10% of every draw sits in trust for months. But buyers are often surprised to learn that even after moving in, money is still locked up with their lawyer. Good builders plan for the holdback gap. Under-capitalized builders struggle with it — and that’s one reason choosing a financially stable builder matters as much as choosing the right floor plan.

Lender Requirements for Construction Mortgages in Alberta

Not every lender offers construction mortgages, and those that do have stricter requirements than a standard purchase. Here’s what you’ll need to qualify in 2026.

Down Payment

Most lenders require a minimum 20-25% down payment for construction mortgages. Unlike a standard insured purchase where you can put down as little as 5%, CMHC generally doesn’t insure construction mortgages on custom builds — so you’re in conventional territory from the start. Some credit unions and monoline lenders will go as low as 20%, but the sweet spot for the best rates is 25-35% (WOWA, 2026).

Builder Qualification

This is where many buyers hit an unexpected wall. Lenders don’t just qualify you — they qualify your builder. Requirements typically include:

- New Home Warranty enrollment: Mandatory in Alberta. Your builder must be enrolled with a warranty provider like the Alberta New Home Warranty Program before construction begins (Government of Alberta, 2026).

- Builder track record: Lenders want to see that your builder has completed similar projects on time and on budget. A builder with 2-3 successful completions in the past 24 months is the usual threshold.

- Financial statements: Some lenders request the builder’s financial statements to confirm they can carry the project between draws.

- Fixed-price contract: Most lenders require a fixed-price building contract (not cost-plus) to establish the total mortgage amount upfront.

Contingency Fund

Lenders recommend — and some require — a 15-20% contingency fund above your contracted build price to cover change orders, material price shifts, and unexpected site conditions (New Homes Alberta, 2026). On a $500,000 build, that’s $75,000-$100,000 in accessible cash or credit beyond your down payment and contracted costs.

Citation capsule: Alberta construction mortgage lenders require 20-25% down payment, a qualified builder enrolled in New Home Warranty, a fixed-price building contract, and recommend a 15-20% contingency fund to cover cost overruns during the 8-14 month build period (WOWA, 2026; Government of Alberta, 2026). For a full breakdown of down payment requirements, see our down payment Alberta guide.

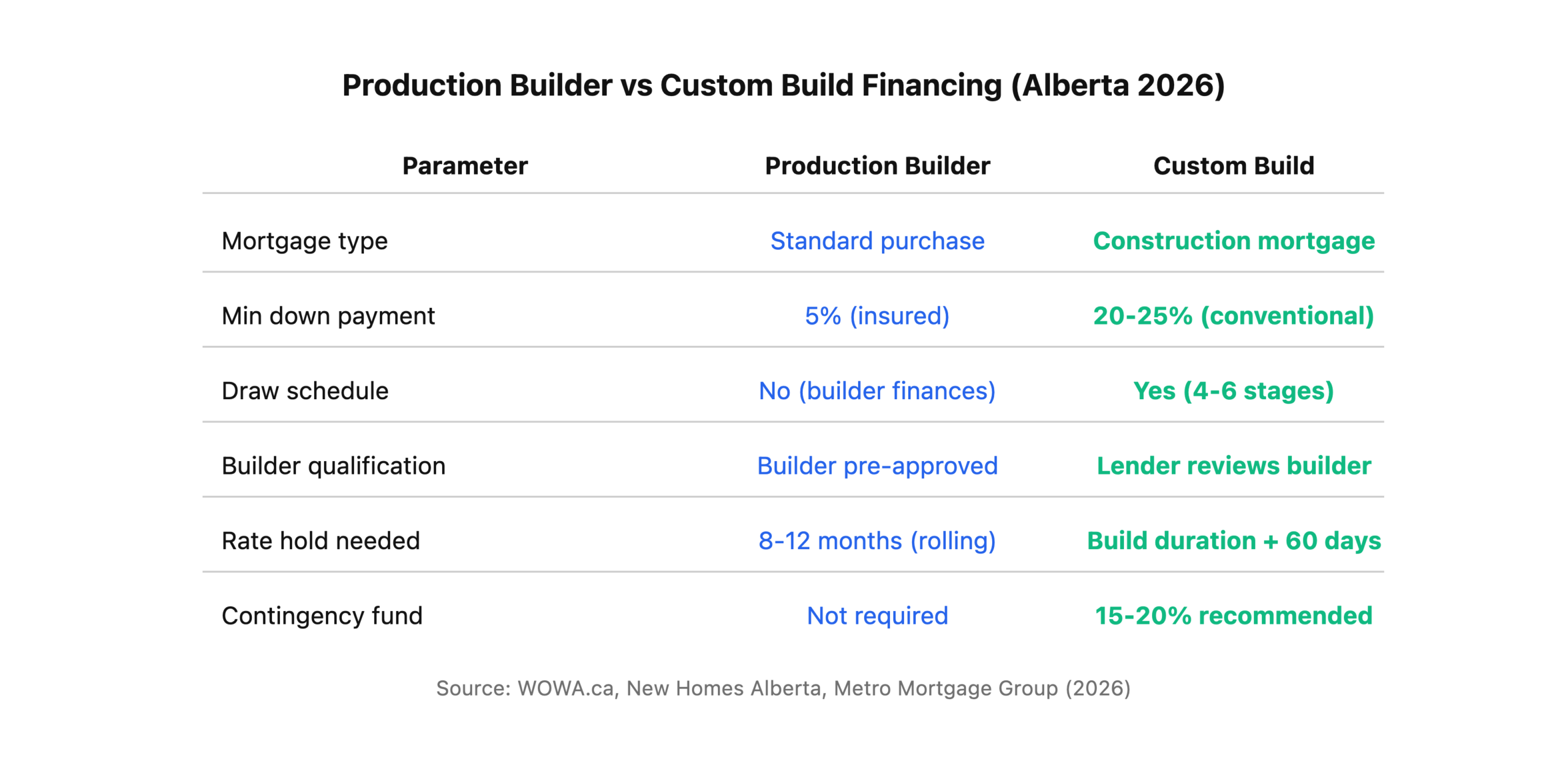

Builder Packages vs. Custom Builds: Different Financing Paths

The construction mortgage process splits into two distinct streams depending on whether you’re buying from a production builder or hiring a custom builder. The financing mechanics are different enough that choosing the wrong approach can cost you months and thousands of dollars.

Production Builder (Spec or Pre-Sale)

When you buy a new home from a production builder like Jayman Built, Homes by Avi, or Coventry Homes, you’re typically signing a purchase agreement — not a construction contract. The builder has already arranged their own construction financing, and you’re buying a finished (or nearly finished) product. Your mortgage works more like a standard purchase with a delayed closing date.

In this scenario, you need a rate hold long enough to cover the build timeline. Most lenders offer rate holds of 90-120 days, but a new build might take 8-12 months. Your broker can structure a rolling rate hold that extends your rate guarantee through to the builder’s estimated completion date.

Custom Build

A custom build is where the full construction mortgage process kicks in. You’re hiring your own builder, you own the lot (or are purchasing it simultaneously), and the lender is underwriting both you and the building project. This is where draw schedules, progress inspections, and builder qualification requirements all apply.

Do you already own your lot? That simplifies things — the land equity counts toward your down payment. If you’re buying the lot and building simultaneously, some lenders will wrap both into a single construction mortgage, while others require a separate land purchase.

Progress Inspections: The Gatekeeper of Every Draw

Each draw triggers a progress inspection by an independent appraiser hired by the lender — not your builder’s inspector and not a municipal building inspector. The appraiser confirms three things: percentage complete matches the draw request, quality meets plan specifications, and the project is tracking within the approved budget.

From my construction days, I can tell you the inspection is where most draw delays happen. If the appraiser shows up and the framing isn’t actually complete — maybe the garage trusses aren’t set or the sheathing isn’t finished — they’ll report a lower percentage, meaning a smaller draw and more cost for your builder to carry until the next milestone. Stay in regular communication with your builder about draw timing, and make sure the work is genuinely complete before the appraiser visits.

Citation capsule: Progress inspections by independent appraisers are required at each draw stage of an Alberta construction mortgage, verifying percentage of completion, quality of workmanship, and budget adherence before funds are released to the borrower’s lawyer (WOWA, 2026).

The Completion Mortgage: Transitioning to Permanent Financing

Once your home is complete and you’ve received your occupancy permit, your construction mortgage converts to a completion mortgage (or “take-out mortgage”) — the standard 25-year amortization, 5-year term mortgage most Canadians are familiar with. The transition involves a final appraisal, title insurance registration, holdback release after the 60-day lien period, and rate conversion to your permanent terms.

This is where having a broker pays dividends. During the construction phase, you’re limited to lenders that do construction financing. But for the completion mortgage, the full market opens up. We shop your completion mortgage separately to make sure you’re getting the best permanent rate, not just defaulting to the construction lender’s offer. Your credit profile still matters at this stage — see our credit score and mortgage Alberta guide for how it factors in.

CMHC’s Role in Construction Financing

For multi-unit residential construction (5+ units), CMHC offers the MLI Select program and its Apartment Construction Loan Program, which are among the most attractive financing tools available to Alberta developers. Key features include:

- Amortization up to 50 years — dramatically improving cash flow projections compared to conventional 20-25 year terms.

- Interest-only payments during construction — you’re not paying down principal while the building is going up.

- 10-year fixed rate terms — providing stability through the full build and initial stabilization period.

- Funding extended through 2031-32 — CMHC renewed the program recently, giving developers a long runway to plan projects.

For single-family construction, CMHC generally doesn’t insure custom builds — which is why the 20-25% down payment applies. However, if you’re buying from a production builder and the home is already complete, standard CMHC insurance with 5% down becomes available. Building a small apartment or rental project with 5+ doors? The MLI Select amortization advantage alone can make a project viable that wouldn’t pencil out with conventional financing — see our multi-family mortgage Edmonton guide for the full breakdown.

Construction Mortgage Rates in 2026

With the Bank of Canada holding at 2.25%, construction mortgage rates in Alberta currently break down into three tiers (Bank of Canada, 2026):

- A-lender construction loans: Approximately 4.45-5.50%, typically prime + 1.5% to prime + 2.5%. Available to borrowers with strong credit, 25%+ down, and a qualified builder.

- B-lender / credit union: Approximately 5.50-7.00%. More flexible on builder qualification and property type, but higher rates and fees.

- Private construction loans: Approximately 8.00-12.00%. Used for land assembly, speculative builds, or borrowers who don’t qualify with institutional lenders. Short terms (6-18 months) with lender fees of 1-3%.

One thing that catches many buyers off guard: you pay interest on the drawn portion only, not the full mortgage amount. During Stage 1, when only 15-20% has been drawn, your monthly interest cost is relatively low. It ramps up with each subsequent draw — but you’re never paying interest on money still sitting with the lender.

Citation capsule: Alberta construction mortgage rates in mid-2026 range from 4.45% on institutional A-lender products to 8-12% on private construction loans, with borrowers paying interest only on the drawn portion during the build phase (Bank of Canada, 2026; WOWA, 2026).

5 Common Construction Mortgage Mistakes

After 9+ years in construction and over a decade in mortgage brokering, these are the mistakes I see most often:

-

Underestimating the contingency fund. A 10% buffer sounds reasonable until lumber prices spike or your excavation hits rock. Budget 15-20% and hope you don’t need it.

-

Choosing a builder without checking lender compatibility. Your dream builder might not meet your lender’s qualification requirements. Get your builder pre-approved with the lender before signing a building contract.

-

Not getting a fixed-price contract. Cost-plus contracts give builders flexibility, but most lenders won’t approve them because the final cost is unknown. Insist on a fixed-price contract with clearly defined specifications.

-

Starting construction before financing is confirmed. I’ve seen buyers break ground with only a verbal commitment from a lender, then scramble when the formal approval doesn’t come through. Get your construction mortgage in writing before a single shovel hits dirt.

-

Forgetting about the completion mortgage. The construction phase is only half the financing picture. Arrange your completion mortgage early — don’t wait until the build is done to start shopping permanent rates.

Budgeting for a build also means budgeting for closing — see our closing costs Alberta guide for a full breakdown.

FAQ

How much down payment do I need for a construction mortgage in Alberta?

Most lenders require 20-25% of the total project cost (land + construction), since CMHC generally doesn’t insure custom construction mortgages. If you already own the lot free and clear, the land equity can count toward your down payment. Lenders also recommend a 15-20% contingency fund above the contracted build price.

How long does a construction mortgage last?

The construction phase typically runs 8-14 months for a single-family home in Alberta. Once the build is complete and you receive your occupancy permit, the construction mortgage converts to a permanent completion mortgage with a standard 25-year amortization and 5-year term.

Can I act as my own builder (owner-builder) and still get a construction mortgage?

It’s possible but significantly harder. Most A-lenders require a licensed, warranty-enrolled builder. Some B-lenders and credit unions will finance owner-builder projects, but expect higher rates (6-8%), lower LTVs (maximum 65%), and more frequent draw inspections. You’ll also need to demonstrate construction experience and provide detailed cost breakdowns.

What happens if my builder goes bankrupt during construction?

This is every homeowner’s nightmare — and it’s why the New Home Warranty Program exists in Alberta. Your warranty coverage protects deposits and provides completion assurance. From the mortgage side, the lender will typically freeze draws until a new builder is contracted and approved. The holdback in your lawyer’s trust account provides a financial buffer for this scenario.

Does Metro Mortgage Group arrange construction mortgages?

Yes. Metro Mortgage Group has arranged construction financing for custom builds, renovations, and multi-unit projects across Alberta since 2011. Nelson Sousa’s 9+ years of construction industry experience gives our team a builder’s perspective on draw schedules, cost estimation, and project management that most mortgage brokerages simply don’t have. Call us at 780-974-1270 or email info@MetroMortgageGroup.ca.

Ready to Build? Let’s Structure Your Construction Mortgage

Whether you’re planning a custom build on your own lot, buying from a production builder, or developing a multi-unit project, Metro Mortgage Group’s team understands construction financing from the ground up — literally. Nelson Sousa’s years running a construction company, combined with our access to 30+ lending partners, means your construction mortgage gets structured by someone who’s actually held a set of blueprints.

Call us: 780-974-1270

Email: info@MetroMortgageGroup.ca

Visit: 10706 120 St NW #200, Edmonton, AB T5H 0W7

For the broader commercial picture, see our commercial mortgages Edmonton guide, and if you’re weighing what you can afford before you build, check how much mortgage you can afford.

About the Author

Nelson Sousa is co-owner of Metro Mortgage Group Inc. and a licensed mortgage broker in Edmonton, Alberta. Before entering the mortgage industry, Nelson spent more than 9 years running a construction company, giving him first-hand expertise in draw schedules, builder relationships, project costing, and construction financing. He co-founded Metro Mortgage Group in 2011 and has helped structure hundreds of residential, commercial, and construction mortgages across Alberta. The team maintains a 5.0-star rating across 229 Google reviews.

Last updated: May 26, 2026