Mixed-Use Property Mortgages in Edmonton

Residential-over-retail and live-work building financing in Alberta

Mixed-use buildings — storefronts on the main floor, apartments above — are some of the most popular investment plays in Edmonton’s mature neighbourhoods, yet they’re also one of the trickiest property types to finance. The reason? Lenders classify them differently depending on how much of the building is commercial, and that classification changes everything: the down payment, the rate, the amortization, and whether CMHC insurance is even on the table (CMHC, 2025).

Here’s how mixed-use financing actually works in Alberta in 2026, which lender channels apply to which building profile, and what Metro’s commercial desk sees on real Edmonton files every month.

Key Takeaways

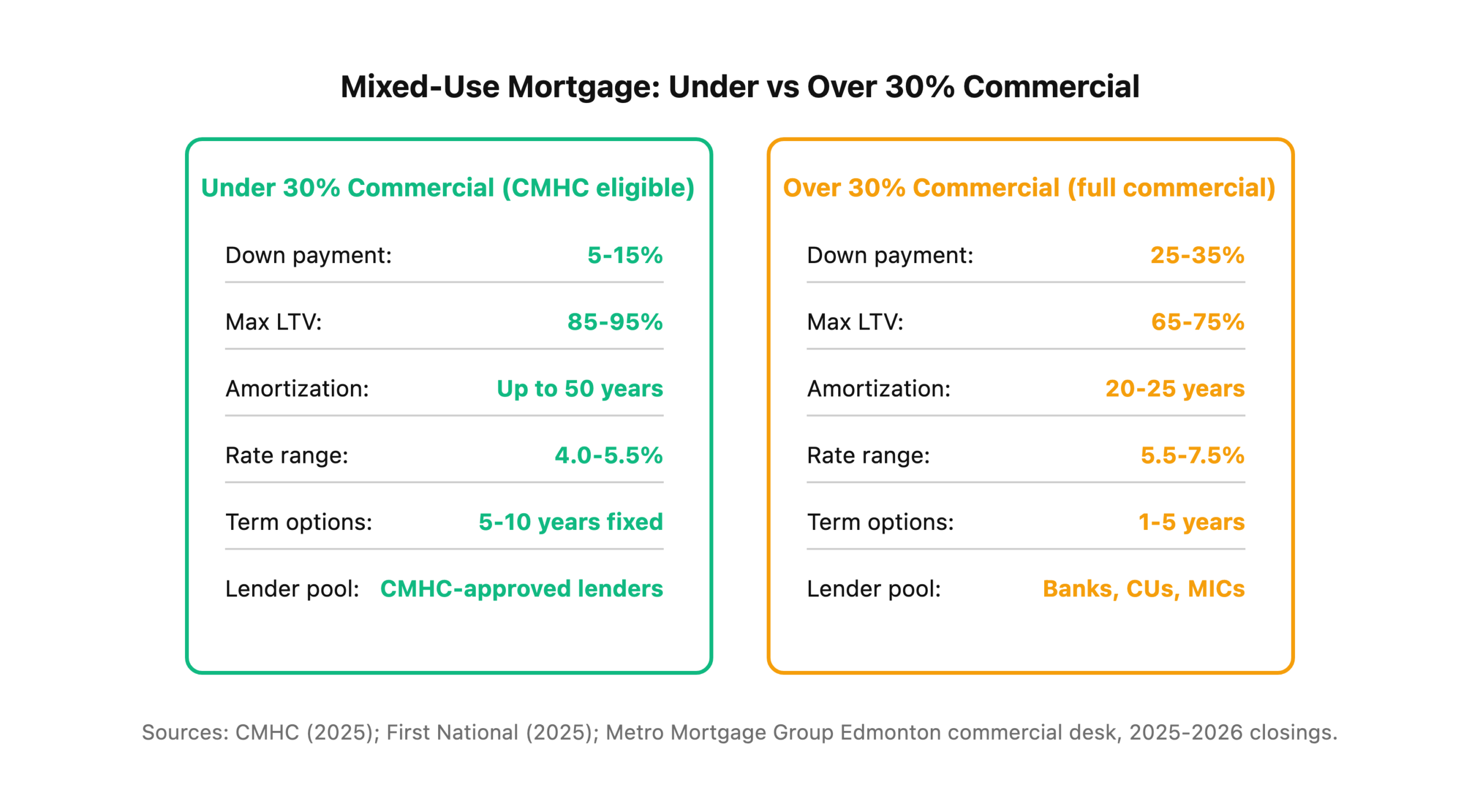

– CMHC will insure a mixed-use building only if the commercial component is under 30% of total floor space and under 30% of gross revenue (CMHC, 2025).

– Qualifying mixed-use deals can access 85% LTV (MLI Standard) or up to 95% LTV (MLI Select) — dramatically less cash at closing than a conventional bank offer.

– Buildings above the 30% commercial threshold shift to full commercial underwriting: 25-35% down, shorter amortizations, and income-based qualification.

– B-lenders and credit unions fill the gap for deals that don’t fit CMHC criteria, typically at 65-75% LTV with higher rates.

– Edmonton’s zoning bylaw uses DC2 (Direct Control) and MU (Mixed Use) designations — confirm zoning before you make an offer, because it affects both lender appetite and insurance eligibility.

What Qualifies as a Mixed-Use Property in Alberta?

A mixed-use property combines residential and commercial uses in a single building. In Edmonton, the most common format is a two- or three-storey walk-up with ground-floor retail, restaurant, or office space and residential apartments above. Think Whyte Ave, 124 Street, Stony Plain Road, and the Jasper Ave corridor — neighbourhoods where this building type has existed for decades.

From a mortgage lender’s perspective, the critical question isn’t architectural. It’s mathematical: what percentage of the building is commercial? That single number determines which financing channel the deal falls into and how much cash the borrower needs at closing.

CMHC draws the line at 30%. If the non-residential component accounts for less than 30% of total floor space and generates less than 30% of gross revenue, the property can qualify for CMHC multi-unit mortgage insurance (CMHC, 2025; First National, 2025). Cross either threshold and the entire building gets classified as commercial — no CMHC insurance, higher down payment, shorter amortization.

Residential vs Commercial Classification: Why the 30% Rule Matters

The 30% threshold isn’t arbitrary — it’s the single most consequential number in mixed-use financing. Landing on the right side of it can save an Edmonton investor $100,000+ in upfront cash on a mid-sized building purchase. Here’s what each side of the line looks like:

The math speaks for itself. On a $1.5M mixed-use building in Oliver, a CMHC-eligible deal at 15% down requires $225,000 cash at closing. The same building classified as full commercial at 30% down requires $450,000. That’s $225,000 of additional equity — capital that could fund a second property entirely.

How Does CMHC Insurance Work on Mixed-Use Buildings?

CMHC’s multi-unit mortgage insurance program is the only insurer covering mixed-use properties in Canada, and the eligibility criteria are straightforward but rigid (CMHC, 2025). Your building must meet all of the following:

- At least 5 residential units — buildings with 4 or fewer units are underwritten under residential rules, not multi-unit commercial

- Commercial component under 30% of total floor space

- Commercial revenue under 30% of total gross revenue

- Stabilized occupancy — typically 85%+ for existing buildings

- Sponsor qualifications — minimum 5 years of multi-unit property management experience (or a retained property manager with that track record), net worth of at least 25% of the loan amount, and a personal guarantee until 12 months of stable rents are established

If the building qualifies, the borrower can access the same MLI Standard or MLI Select programs available for pure residential multi-family. That means up to 85% LTV on MLI Standard and up to 95% LTV on MLI Select with qualifying affordability, energy, or accessibility points. The insurance premium runs 1.5-4.5% of the loan amount, financed into the mortgage, with discounts available under MLI Select’s tiered point system.

The catch? CMHC underwriting adds 45-90 days to the closing timeline. Plan your purchase conditions accordingly — a mixed-use CMHC file is not closing in 30 days.

For the full breakdown of MLI Select point tiers, see our multi-family mortgage Edmonton guide.

LTV and Down Payment by Financing Channel

Not every mixed-use deal fits CMHC. Buildings with more than 30% commercial space, vacant commercial units, or sponsors who don’t meet the experience requirements need a different path. Here’s how the full lender landscape breaks down for Edmonton mixed-use properties:

CMHC-insured (under 30% commercial): 5-15% down, 85-95% LTV, 40-50 year amortization. Best rates and terms in the market. Requires 5+ residential units, stabilized occupancy, and qualified sponsors.

Chartered banks — commercial desk: 25-30% down, 70-75% LTV, 20-25 year amortization. Available for any mixed-use configuration. ATB Financial, RBC Commercial, and Scotiabank Commercial are active in the Edmonton mixed-use space. Expect a DSCR requirement of 1.20-1.40x and full commercial underwriting (OSFI, 2025).

Credit unions: 25-35% down, 65-75% LTV, 20-25 year amortization. Alberta credit unions like Servus and Connect First sometimes offer more flexibility on mixed-use deals than chartered banks, particularly on smaller buildings in established neighbourhoods. They’re worth quoting on every mixed-use file.

B-lenders and MICs: 25-40% down, 60-75% LTV, interest-only or 20-year amortization, rates in the 7-11% range. Private MICs fill the gap for mixed-use deals with high vacancy, recent commercial turnover, or sponsors who don’t meet A-lender criteria. They’re expensive, but they close when nobody else will — typically in 14-30 days.

Compare these channels against pure multi-family options in our multi-family mortgage Edmonton guide.

B-Lender and Alternative Options for Mixed-Use Properties

What happens when the commercial component exceeds 30%, the building has a vacant storefront, or the borrower doesn’t have five years of management experience? The deal doesn’t die — it just moves to a different lender channel.

B-lenders and Mortgage Investment Corporations (MICs) are the primary alternative for Edmonton mixed-use deals that don’t fit CMHC or A-lender criteria. They trade higher rates for flexibility. A typical B-lender mixed-use term looks like 65-70% LTV, 1-3 year term, interest-only payments, and a rate of 7-10% depending on the building’s cash flow and the sponsor’s profile.

Why would anyone pay those rates? Speed and structure. A B-lender can close a mixed-use acquisition in 2-4 weeks while CMHC takes 60-90 days. And for value-add plays — buying a building with a vacant commercial unit, renovating, re-tenanting, and then refinancing into CMHC once the building stabilizes — the B-lender bridge is often the only path to the deal.

Metro regularly structures these two-step plays: acquire on a short-term MIC or B-lender mortgage, stabilize the property and achieve 85%+ occupancy, then refinance into CMHC MLI Standard or Select at dramatically better terms. The exit strategy is the whole point.

Edmonton Zoning Considerations for Mixed-Use Properties

Before you even think about the mortgage, you need to confirm the property’s zoning supports mixed-use. Edmonton’s Zoning Bylaw uses several designations that permit combined residential and commercial:

- MU (Mixed Use) — Specifically designed for buildings combining commercial and residential uses. Common along transit corridors and in mature neighbourhoods (City of Edmonton Zoning Bylaw, 2025).

- DC2 (Direct Control) — Site-specific zoning that can allow tailored mixed-use configurations. Many of Edmonton’s established mixed-use buildings on Whyte Ave, 124 Street, and Jasper Ave sit on DC2 parcels.

- CB1/CB2 (Commercial Business) — Permits residential above commercial in certain configurations.

Why does zoning matter for mortgage purposes? Because lenders verify it. A CMHC-approved lender won’t fund a mixed-use deal if the zoning doesn’t support the building’s current use — and a non-conforming use creates risk that shows up in the appraisal and the legal opinion. If you’re looking at a property where the commercial tenant operates under a conditional use permit rather than a permitted use, flag it for your broker early.

Also watch for parking requirements. Edmonton’s zoning bylaw ties parking minimums to both the residential and commercial components. A mixed-use building that doesn’t meet parking requirements can trigger conditions on the development permit that affect the mortgage timeline.

For a broader look at Edmonton commercial financing, see our commercial mortgages Edmonton guide.

OSFI’s 2026 Rule Changes and Mixed-Use Financing

OSFI’s updated Capital Adequacy Requirements (CAR) guideline, effective November 2025, introduced a classification that directly affects mixed-use mortgage holders: Income-Producing Residential Real Estate (IPRRE) (OSFI, 2025).

Under the new framework, if more than 50% of the qualifying income used to service a mortgage comes from the property itself (rental income rather than personal employment income), the mortgage gets classified as IPRRE. Banks must hold more capital against IPRRE loans, which makes these files marginally more expensive to originate. For borrowers, this means lenders are applying tighter scrutiny to how rental income is used across multiple properties.

The practical impact on mixed-use deals? Borrowers who already own several rental properties may find it harder to qualify for additional mixed-use acquisitions at A-lenders, because personal employment income can’t be double-counted across multiple files. This is where having a broker who works across 30+ lenders becomes particularly valuable — the same deal rejected at one bank can often be approved at a credit union or monoline lender with different internal risk appetite.

How Metro Mortgage Group Structures Mixed-Use Deals

Metro’s approach to mixed-use financing starts with a simple question: does this building qualify for CMHC, and if not, what’s the fastest path to get it there?

For buildings that already meet the 30% threshold, Metro submits to the CMHC-approved lender panel — typically 3-5 simultaneous submissions — and negotiates rate, term, and premium across the full range of MLI Standard and MLI Select options. The goal is the lowest blended cost of capital over the hold period, not just the lowest rate on day one.

For buildings above 30% commercial, Metro structures the file across the B-lender, credit union, and bank channels simultaneously. If the long-term plan is to convert commercial space to residential (a play that’s increasingly common in Edmonton as retail vacancy shifts), Metro models the refinance into CMHC at the stabilization date so the borrower knows their exit numbers before they close the acquisition.

Every mixed-use file gets a full cash flow model with sensitivity analysis — what happens if a commercial tenant doesn’t renew, if residential vacancy bumps to 10%, or if rates move 100 bps at renewal. The mortgage structure has to survive all three scenarios.

Read about Metro’s full commercial process in our commercial mortgages Edmonton guide.

Frequently Asked Questions

Can I get a mixed-use mortgage with less than 20% down in Alberta?

Yes, but only if the building qualifies for CMHC multi-unit insurance — which requires at least 5 residential units and a commercial component under 30% of floor space and revenue (CMHC, 2025). CMHC MLI Standard allows up to 85% LTV (15% down), and MLI Select can push to 95% LTV (5% down) on qualifying deals. Buildings that don’t meet the 30% threshold require conventional commercial financing at 25-35% down.

Do mixed-use buildings qualify for CMHC MLI Select in Edmonton?

They can, provided the commercial component stays under 30% and the building meets MLI Select’s point requirements for affordability, energy efficiency, or accessibility (CMHC, 2025). The energy efficiency pathway is often the most accessible for existing mixed-use buildings — a retrofit that achieves 15-25% improvement over the National Energy Code can earn enough points for the 50-point tier (85% LTV, 40-year amortization, 10% premium discount).

How is rental income from commercial tenants treated in a mixed-use mortgage?

Lenders underwrite mixed-use properties on blended income — residential and commercial rents combined — and assess the building’s Debt Service Coverage Ratio (DSCR) rather than the borrower’s personal GDS/TDS ratios. Most lenders want a DSCR of 1.20x or higher, meaning net operating income is at least 120% of the annual debt service (OSFI, 2025). Commercial tenant lease terms, credit quality, and remaining lease duration all factor into the DSCR calculation.

What happens if a commercial tenant leaves a mixed-use building mid-mortgage?

The building’s DSCR drops, which can trigger covenant issues at renewal. Most lenders underwrite with some vacancy assumption (5-10% on residential, higher on commercial), but a fully vacant commercial unit on a small mixed-use building can push the DSCR below 1.0x. Proactive measures include negotiating longer commercial lease terms before closing, maintaining a cash reserve for commercial vacancy, and structuring the mortgage with enough headroom in the DSCR to absorb a single commercial vacancy.

Ready to Finance an Edmonton Mixed-Use Building?

Mixed-use financing rewards precision — the right classification, the right lender channel, and the right deal structure can save six figures of equity on a single transaction. Metro’s commercial desk works mixed-use files across Edmonton and Calgary every month, from 6-unit Whyte Ave walk-ups to 40-unit transit-corridor builds. Whether the deal fits CMHC today or needs a bridge-to-CMHC strategy, we’ll model every scenario before you sign. Call 780-974-1270 or email info@MetroMortgageGroup.ca to get started.

For the broader commercial financing picture, start with the commercial mortgages Edmonton guide. Looking at a pure residential multi-family instead? See the multi-family mortgage Edmonton guide.

Also see our down payment Alberta guide for residential down payment context, our closing costs Alberta guide for closing cost planning, and our current rate benchmarks for where rates sit today.

About the author: Miguel Cunha is a mortgage broker at Metro Mortgage Group specializing in commercial and mixed-use financing across Edmonton and Alberta. Metro Mortgage Group has served Alberta borrowers since 2011 with 229 five-star Google reviews.

Last updated: June 18, 2026