Commercial Mortgage Refinance in Edmonton

Refinancing options for income properties, multi-family, and commercial assets

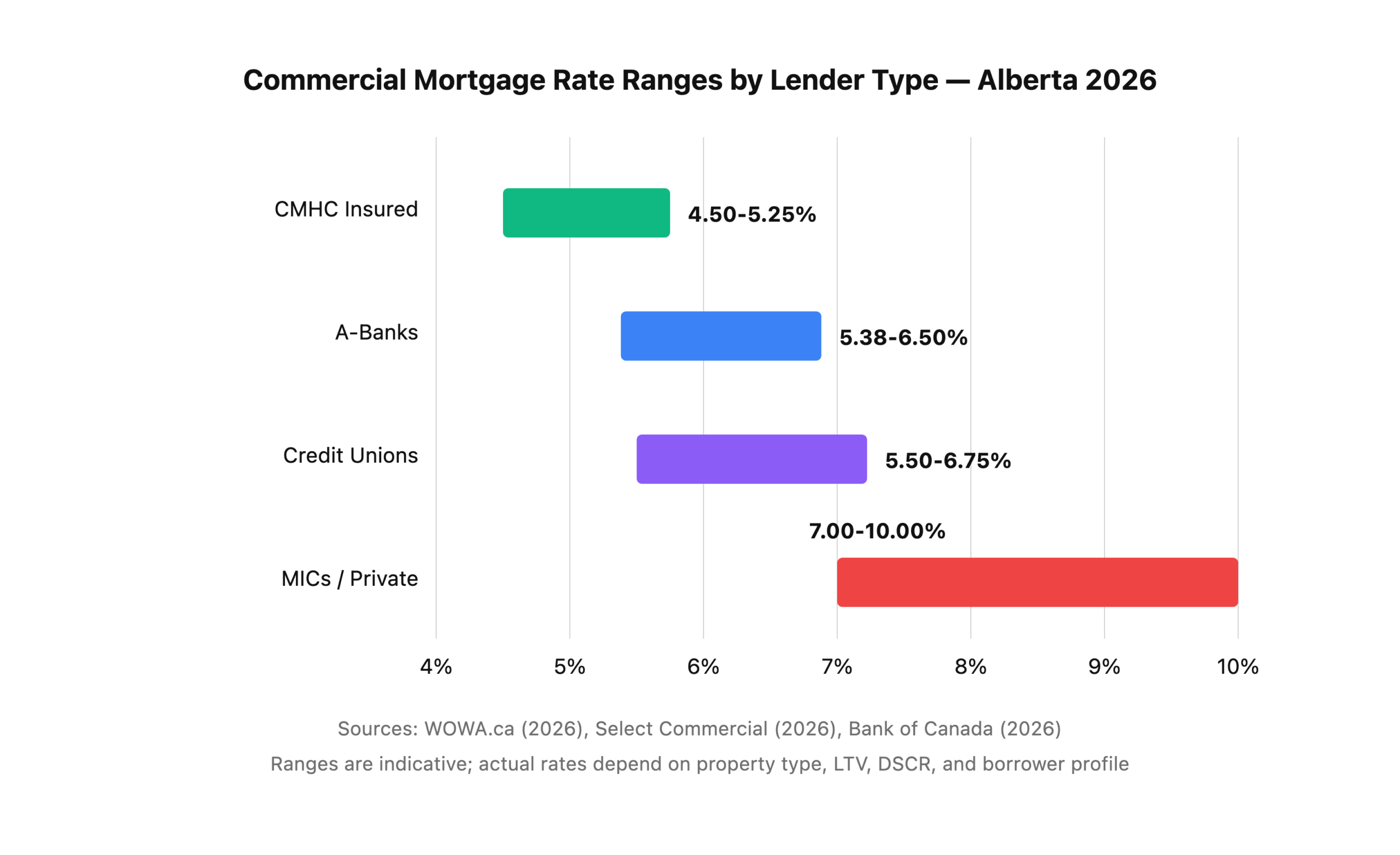

Commercial mortgage rates in Canada start at 5.38% as of mid-2026 (WOWA.ca commercial mortgage guide, 2026) — and with the Bank of Canada holding its overnight rate steady at 2.25% since late 2025, the refinance window is wide open for Edmonton property owners carrying higher-rate legacy debt. Yet most commercial borrowers don’t refinance until renewal, leaving thousands of dollars on the table every year. Why? Because commercial refinancing feels complicated. It doesn’t have to be.

Key Takeaways

– Commercial mortgage rates start at 5.38% in 2026 — owners locked in at 6%+ during the 2023-2024 rate peak should explore refinancing now (WOWA.ca).

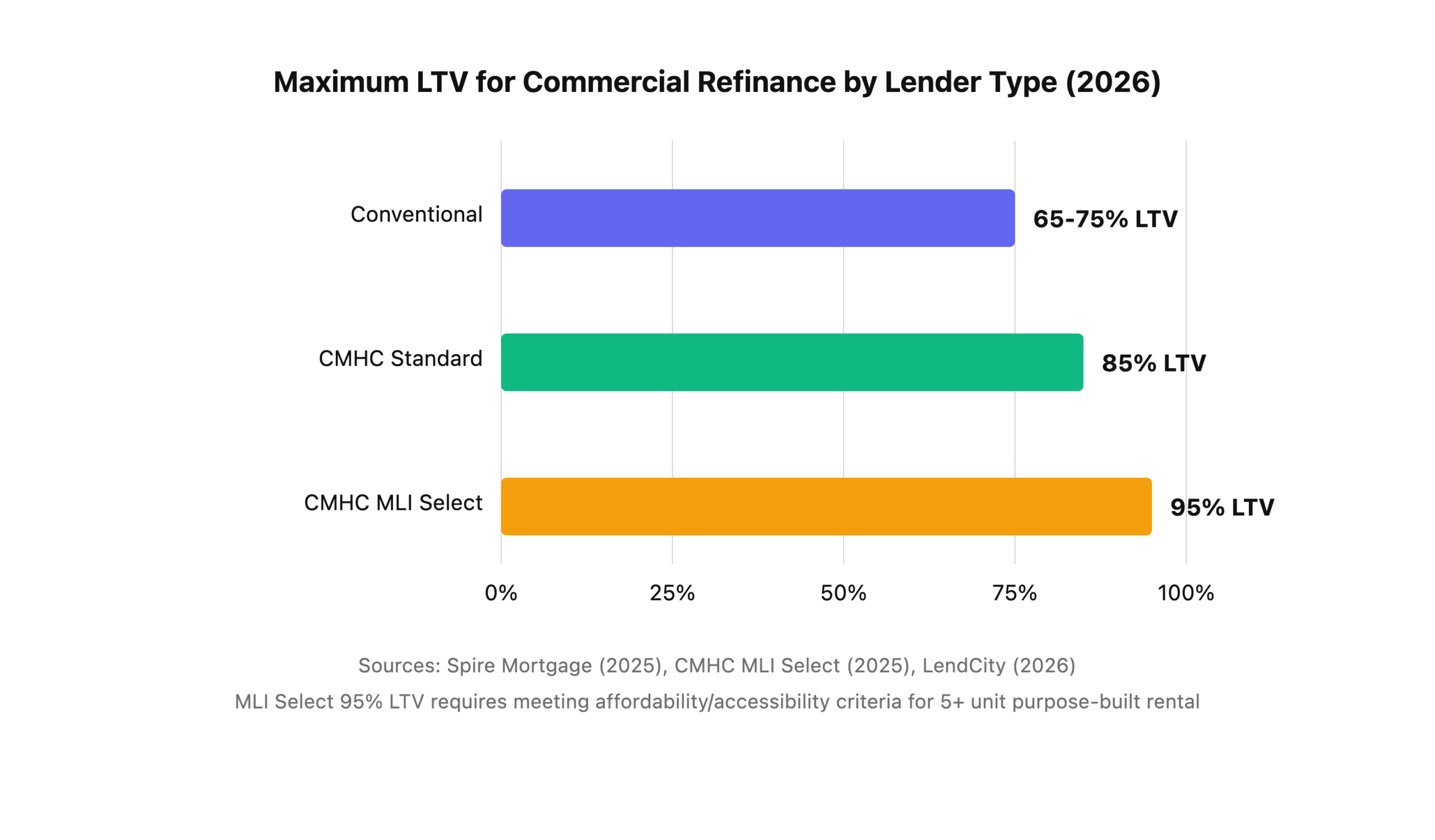

– Conventional commercial lenders offer 65-75% LTV on refinance; CMHC-insured multi-family can reach 85% LTV (CMHC, 2025).

– Prepayment penalties on commercial mortgages can run 3 months’ interest to full yield maintenance — calculate before you commit (FCAC).

– Metro Mortgage Group accesses 30+ lenders to find the right commercial refinance terms — not just the lowest rate.

What Is a Commercial Refinance, and How Does It Differ from Residential?

Commercial refinancing replaces your existing commercial mortgage with a new one — but the similarities to residential refinancing end there. According to CMLS Financial, commercial deals need 60-90 days minimum to close, compared to 30 days for residential (CMLS Financial, 2025). The lender underwrites three things simultaneously: you (the borrower), the property’s income (rent rolls, operating statements, cap rate), and the physical asset (appraisal, Phase 1 environmental, building condition report).

That triple-underwrite is why commercial refinancing takes longer, costs more in due diligence, and rewards owners who start early. If you’re waiting until your renewal date to explore options, you’ve already lost your best negotiating window. Have you checked what your current rate actually costs you compared to today’s market?

Citation Capsule: “Commercial mortgage transactions typically require 60-90 days from application to funding, compared to 30 days for residential deals, because lenders must underwrite the borrower, the property income, and the physical asset simultaneously.” — CMLS Financial commercial lending FAQ

For the fundamentals of commercial financing, see our commercial mortgages Edmonton guide.

When Does a Commercial Refinance Make Sense?

Rate improvement is the most common trigger, but it’s not the only one. The Bank of Canada cut its overnight rate nine times between June 2024 and October 2025, dropping from 5.00% to 2.25% (Bank of Canada, 2026). If you locked a commercial mortgage during the 2023-2024 rate peak, you could be paying 100-200+ basis points above today’s best available rates.

Here are the five scenarios where a commercial refinance in Edmonton typically pays for itself:

1. Rate Reduction

Your current rate is meaningfully higher than what’s available today. Even a 50-basis-point improvement on a $2-million commercial mortgage saves $10,000 per year in interest. On a five-year term, that’s $50,000 — usually far more than the cost of breaking your existing mortgage.

2. Equity Takeout

Your property has appreciated, and you need capital for renovations, a down payment on another property, or business expansion. Conventional lenders offer 65-75% LTV on commercial refinance. If your property is worth $3 million and you owe $1.5 million, you could potentially access $750,000 or more in equity.

3. Term Extension or Restructuring

You want longer amortization to improve cash flow, or you need to move from a variable rate to a fixed rate (or vice versa) based on your outlook for interest rates.

4. Consolidation

You’re carrying a first mortgage plus a second mortgage, vendor take-back, or line of credit on the same property. Rolling everything into a single, lower-rate first mortgage reduces your blended cost and simplifies your payments.

5. Renewal Shopping

Your term is maturing in the next 120-180 days, and you want to test the market rather than blindly accepting your lender’s renewal offer. This is the lowest-friction refinance scenario because there’s typically no prepayment penalty at maturity.

If your property is a 5+ unit rental, see our multi-family mortgage Edmonton guide for CMHC-specific refinance options.

How Much Equity Can You Take Out?

The answer depends on the lender type and whether CMHC insurance is involved. Here’s what Edmonton commercial property owners can expect in 2026:

Conventional refinance (65-75% LTV): Available for any commercial property type — retail, office, industrial, multi-family. Most A-lenders cap at 75% LTV on strong deals with proven cash flow. Credit unions and MICs (Mortgage Investment Corporations) can sometimes stretch to 80%, but expect higher rates.

CMHC-insured refinance (up to 85% LTV): Available for multi-family properties with five or more units. CMHC insurance gives you access to lower rates and higher leverage, but the process takes longer (90-150 days), and CMHC revised premiums upward in July 2025, adding a 0.25% surcharge for every five-year amortization extension beyond 25 years (CMHC, 2025).

CMHC MLI Select (up to 95% LTV): The most aggressive leverage available, but only for purpose-built rental that meets CMHC’s affordability, accessibility, or energy efficiency criteria. This is a powerful tool for Edmonton apartment building owners looking to extract maximum equity for portfolio growth.

Citation Capsule: “CMHC’s MLI Select program allows insured mortgages for new and existing multi-unit rental properties with an LTV of up to 95% for the residential portion, provided the property meets affordability, accessibility, or climate compatibility criteria.” — CMHC MLI Select

For down payment context on the residential side, see our down payment Alberta guide.

Understanding Commercial Mortgage Penalties

The biggest barrier to a mid-term commercial refinance is the prepayment penalty — and commercial penalties are more complex than residential ones. According to the Financial Consumer Agency of Canada, borrowers should always calculate the penalty before committing to a refinance (FCAC, 2026).

Three Months’ Interest

The simplest penalty calculation: outstanding balance × annual rate × 3/12. On a $1.5-million commercial mortgage at 5.75%, that’s $21,563. This is the standard penalty for variable-rate commercial mortgages and the minimum penalty for most fixed-rate products.

Interest Rate Differential (IRD)

More common on fixed-rate commercial mortgages. The formula: principal × (contract rate – current rate) × remaining term. If current rates are higher than your contract rate, the IRD can drop to zero, and you’ll pay only the three-month minimum. If current rates are lower, the IRD can be substantial.

Yield Maintenance

The most expensive penalty structure, common with institutional lenders and CMHC-insured loans. Yield maintenance ensures the lender receives the same return they would have earned had you kept the mortgage to maturity. On a large commercial mortgage with years remaining, yield maintenance penalties can run into six figures.

Lock-Out Period

Some commercial mortgages include a lock-out period (typically the first 1-2 years) during which prepayment is simply not permitted at any price. Know your lock-out dates before you start planning.

The takeaway? Not every penalty makes refinancing prohibitive. When the rate savings over the remaining term exceed the penalty cost, the math works. That’s exactly the analysis we run for every commercial refinance client at Metro.

For a broader look at closing costs, see our closing costs Alberta guide, and for current rate context, check our current rate benchmarks.

How Lender Shopping Changes the Outcome

Commercial mortgage pricing varies 100+ basis points across A-banks, credit unions, and MICs on identical deals (Bank of Canada banking and financial statistics, 2026). That spread matters enormously on a seven-figure mortgage. On a $2-million commercial mortgage, 100 basis points equals $20,000 per year.

Most Edmonton commercial property owners default to their relationship bank — the institution where they have their business chequing account or their personal mortgage. That’s a comfortable choice, but it’s rarely the cheapest one. Why would your bank offer you their best rate if you’re not shopping?

A mortgage broker’s value on a commercial refinance isn’t just rate — it’s knowing which lender fits your deal. An eight-unit apartment building in Oliver has different lender options than a strip mall in Sherwood Park or a warehouse in Nisku. At Metro, we submit to the lenders whose lending criteria match your asset, not just whoever quotes the lowest posted rate.

Illustrative Scenario: Edmonton Strip Mall Refinance

Here’s a hypothetical illustration of how a commercial refinance can play out for an Edmonton retail property owner — a composite example, not a specific client file, with all details changed for privacy:

The situation: An investor owned a 12,000 sq ft strip mall in south Edmonton, fully leased, with a $1.8-million mortgage at 6.45% through a credit union. The five-year term had 22 months remaining. The property had appreciated to $3.1 million based on a recent appraisal.

The problem: The owner wanted to purchase a second commercial property and needed $400,000 for the down payment. Their credit union wouldn’t increase the existing mortgage, and a second mortgage would cost 9-10%.

What we did: We arranged a new first mortgage for $2.2 million (71% LTV) at 5.65% with an A-bank — an 80-basis-point rate improvement. The prepayment penalty on the old mortgage was three months’ interest: $1.8M × 6.45% × 3/12 = $29,025. Legal, appraisal, and environmental costs added another $12,000.

The result: The owner received their $400,000 equity takeout, reduced their rate by 80 bps (saving approximately $17,600 per year on the larger balance), and the penalty plus closing costs were recovered in under 2.5 years of interest savings. Net five-year benefit: approximately $47,000.

Could your property tell a similar story?

Metro’s Commercial Refinance Process: Step by Step

We’ve refined this process over 15 years of arranging commercial deals across Edmonton and Calgary. Here’s what to expect:

Step 1 — Discovery call (Day 1). We review your current mortgage terms, property financials (rent roll, operating statement, NOI), and your goals for refinancing. Is it rate? Equity? Term? All three?

Step 2 — Property and borrower package (Days 2-10). We compile the lender submission package: two years of financial statements, current rent roll, environmental and building condition reports (if available), your personal net worth statement, and the current mortgage statement showing balance, rate, and maturity date.

Step 3 — Lender submissions (Days 10-15). We submit to 3-5 lenders simultaneously, targeting A-banks, credit unions, and specialty lenders whose criteria match your property type and location. Parallel submissions create competition for your deal.

Step 4 — Commitment review (Days 15-30). We present the best commitments side by side — not just rate, but prepayment terms, amortization, covenant requirements, and reporting obligations. The cheapest rate with the worst prepayment penalty isn’t always the best deal.

Step 5 — Conditions and due diligence (Days 30-60). The chosen lender orders their appraisal, reviews the Phase 1 environmental, and works through credit committee. We manage the process and flag any conditions that need your attention.

Step 6 — Funding (Day 60-90). Legal documents are prepared, the existing mortgage is discharged, the new mortgage is registered, and funds flow. You start saving on Day 1 of the new term.

For a breakdown of what closing actually costs, see our closing costs Alberta guide.

Common Questions About Commercial Refinancing in Edmonton

Can I refinance a commercial mortgage before the term is up?

Yes, but you’ll pay a prepayment penalty. On variable-rate commercial mortgages, the penalty is typically three months’ interest. On fixed-rate products, it’s the greater of three months’ interest or the interest rate differential (IRD). On CMHC-insured loans, yield maintenance may apply. Always request a penalty quote from your current lender before proceeding — it’s free to ask.

What credit score do I need for a commercial refinance?

Commercial lending is less credit-score-dependent than residential. Lenders focus on the property’s debt service coverage ratio (DSCR), your net worth, and your track record as a property owner. That said, a personal credit score above 680 opens the widest range of A-lender options. Below 650, expect to work with alternative or private lenders.

How long does a commercial refinance take in Edmonton?

Plan for 60-90 days from application to funding for a clean deal. If CMHC insurance is involved, or if the property requires a new Phase 1 environmental assessment, it can stretch to 120-150 days (CMLS Financial, 2025). Starting the process 6 months before your renewal date gives you maximum flexibility.

Is there a minimum loan amount for commercial refinance?

Most A-lenders start at $500,000 for commercial mortgages. Some credit unions will go as low as $250,000. Below $250,000, you’re typically looking at commercial lines of credit or private lending. Metro works with lenders across the full spectrum, so we can find a fit regardless of deal size.

Can I refinance a commercial property I own personally?

Yes. Many Edmonton investors hold smaller commercial properties (retail condos, small office buildings, mixed-use) in their personal name. The refinance process is similar, though lenders may want to see the property held in a corporation for larger deals. We can advise on the best ownership structure as part of the refinance discussion.

Ready to Explore a Commercial Refinance?

The Bank of Canada’s overnight rate has held at 2.25% since late 2025, and commercial mortgage rates start at 5.38%. If you’re carrying a higher-rate commercial mortgage on an Edmonton property, the math may already be in your favour. Every month you wait is another month of unnecessary interest.

Call Metro Mortgage Group at 780-974-1270 or email info@MetroMortgageGroup.ca for a no-obligation commercial refinance analysis. We’ll pull your penalty quote, run the numbers, and tell you straight whether refinancing makes sense — or whether you’re better off waiting for renewal.

Ready to talk? Contact us, or explore our full range of commercial mortgage services.

About the Author

Daniel De Sousa is co-owner of Metro Mortgage Group Inc., an independent mortgage brokerage in Edmonton, Alberta. With access to 30+ lenders and over a decade of experience in commercial and residential financing, Daniel helps Edmonton and Calgary property owners find the right mortgage — not just the cheapest rate. Metro Mortgage Group: 5.0 stars from 229 Google reviews.

Last updated: June 23, 2026