Mortgage Stress Test Explained: What Are the 2026 Rules for Canadian Buyers?

Canada’s 2026 mortgage stress test requires every federally regulated lender to qualify you at the higher of your contract rate + 2% OR a 5.25% minimum floor — the same OSFI B-20 formula in place since June 2021 and unchanged through 2026 (OSFI, 2024; Department of Finance Canada, 2021). On a 4.59% contract rate, that means you actually qualify at 6.59% — not the rate you’ll pay.

Here’s exactly how the 2026 stress test works, what changed in November 2024, and how to pass it even if your first run through the numbers comes up short.

Key Takeaways

– Canada’s 2026 stress test qualifies buyers at the higher of contract rate + 2% OR 5.25% (OSFI, 2024).

– November 2024 change: OSFI removed the stress test for insured mortgage switches at renewal, giving renewing borrowers more shopping power (OSFI, 2024).

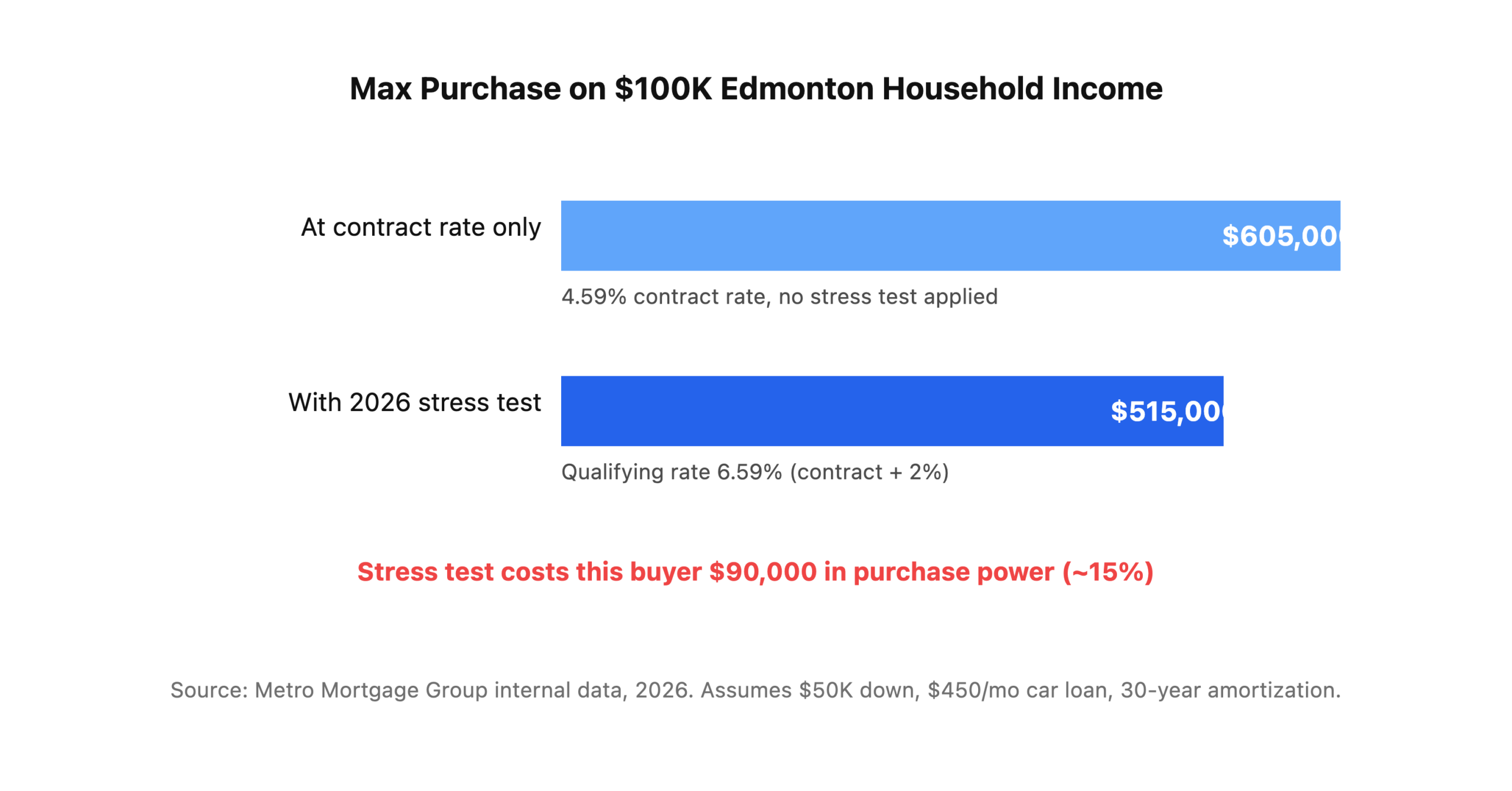

– A $100K Edmonton household qualifies for roughly $515,000 in 2026 vs $605,000 under 2021 conditions — about $90,000 less purchasing power.

– GDS 39% and TDS 44% debt service ratios apply alongside the qualifying rate on all insured mortgages (CMHC, 2025).

– Failing once is not the end — adjusting debt, down payment, or lender type usually gets buyers over the line within 60 days.

What Is the Mortgage Stress Test in 2026?

The mortgage stress test is a federal qualification rule under OSFI Guideline B-20 that forces lenders to underwrite your mortgage at a rate 2 percentage points higher than your contract rate, or 5.25%, whichever is higher (OSFI, 2024). The goal is default protection: making sure you can still afford payments if rates rise.

In 2026, with 5-year fixed rates hovering between 4.39% and 4.89%, the “contract rate + 2%” side of the formula wins on nearly every application. The 5.25% floor only kicks in if your contract rate drops below 3.25% — which hasn’t happened in Canada since early 2022.

A few things to understand before you run your own numbers:

- The stress test is not the rate you pay. You pay your actual contract rate. The stress test is purely a qualification hurdle.

- It applies to all federally regulated lenders — the Big Six banks, credit unions federally chartered under OSFI, and most monoline lenders.

- It applies to insured and uninsured mortgages (with the November 2024 carve-out for insured switches at renewal — more on that below).

- It’s enforced by OSFI, not CMHC. CMHC only touches insured mortgages under $1M with less than 20% down.

How Is the 2026 Qualifying Rate Calculated?

The 2026 qualifying rate is calculated by taking your contract rate, adding 2 percentage points, then comparing that number to the 5.25% floor and using whichever is higher (Department of Finance Canada, 2021). Your lender then runs your income, debts, and the new stressed payment through the GDS and TDS ratio tests.

Here’s the step-by-step math on a typical Edmonton file:

- Contract rate: 4.59% (5-year fixed, April 2026)

- Contract rate + 2%: 6.59%

- Compare to 5.25% floor: 6.59% is higher, so the qualifying rate is 6.59%

- Calculate the stressed monthly payment on your requested mortgage amount at 6.59% over 25 years

- Run GDS / TDS ratios using that stressed payment, not your actual one

For a $400,000 mortgage amortized over 25 years:

- Actual payment at 4.59% = $2,239/month

- Qualifying payment at 6.59% = $2,706/month

- Difference: $467/month of “phantom” payment you must prove you can afford

That $467 gap is exactly why buyers who feel confident they can handle the real payment sometimes fail the stress test on paper.

The GDS and TDS Ratios Alongside the Qualifying Rate

The qualifying rate doesn’t work in isolation. Lenders also apply two debt service ratio limits (CMHC, 2025):

- GDS (Gross Debt Service) = 39% max — total housing costs (mortgage, property tax, heat, 50% condo fees) as a share of gross income

- TDS (Total Debt Service) = 44% max — GDS plus all other debt payments (car, credit cards, student loans, lines of credit)

You have to pass all three hurdles — the stressed payment, GDS 39%, and TDS 44% — or the deal is declined. In our experience, TDS is where Edmonton buyers fail most often, usually because of a car loan and a credit card balance working together against them.

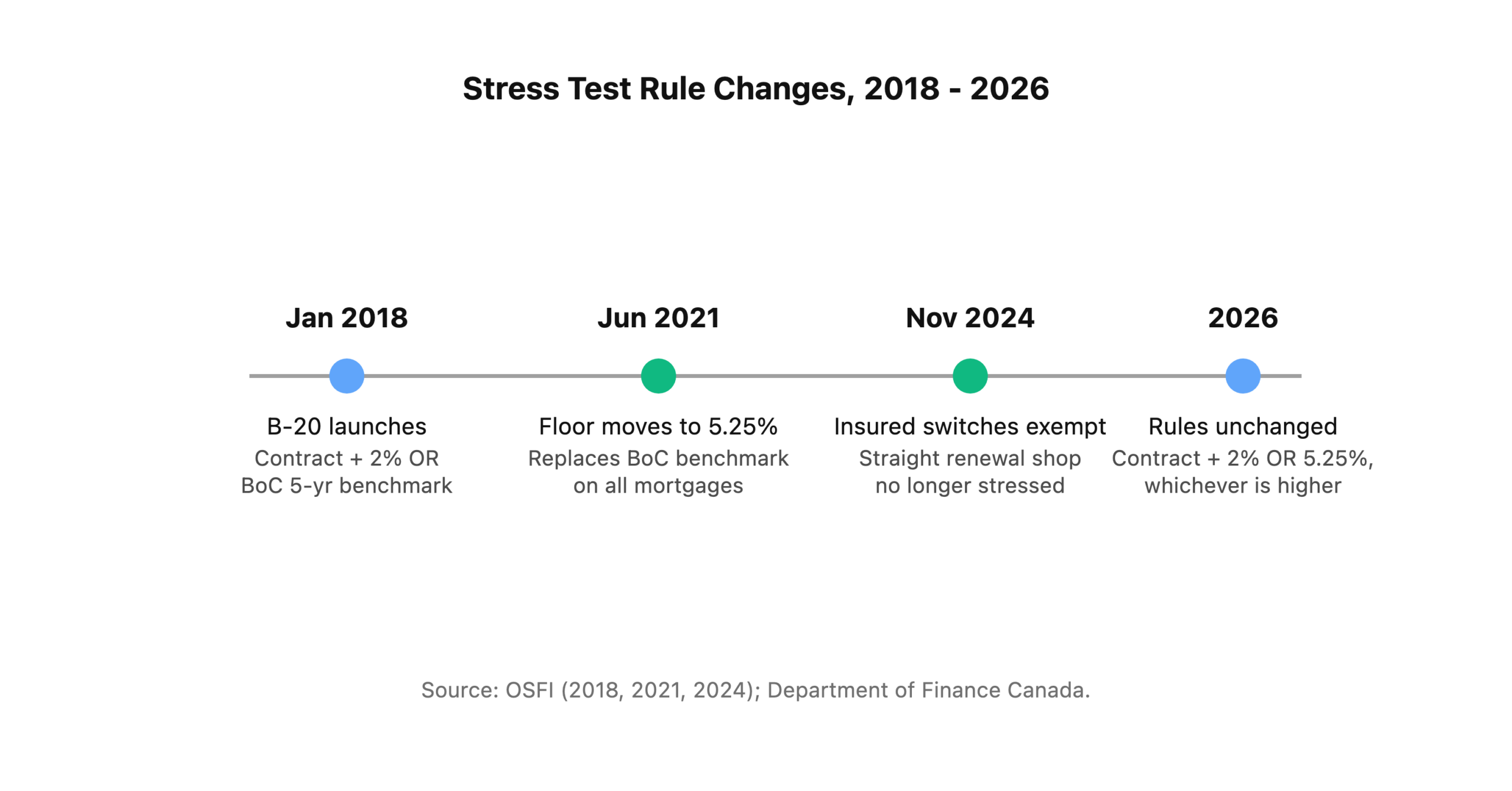

[INTERNAL-LINK: down payment guide → https://metromortgagegroup.ca/how-much-down-payment-alberta/]What Changed in November 2024 for the Stress Test?

The biggest stress test change in years arrived on November 21, 2024, when OSFI announced that the minimum qualifying rate no longer applies to insured mortgage switches at renewal, as long as the borrower is not increasing the loan amount or extending amortization (OSFI, 2024). This change took immediate effect and continues through 2026.

Before November 2024, insured borrowers renewing their mortgage faced an absurd situation: they could stay with their existing lender at whatever renewal rate was offered (no stress test), but the moment they tried to shop the renewal to a competitor, the new lender had to re-run the stress test. Many renewing borrowers were trapped with their existing lender simply because higher rates meant they no longer passed qualification elsewhere.

OSFI’s November 2024 fix was straightforward:

- Applies to: insured mortgages (original purchase was high-ratio / under 20% down)

- Straight switch only: same balance, same or shorter amortization, same borrowers

- Any federally regulated lender: you can now shop the entire market at renewal

- Uninsured borrowers: still subject to the full stress test at switch

For Edmonton renewing borrowers, the November 2024 change added real negotiating power. We’ve watched Metro clients save 0.25% to 0.45% at renewal in 2025 and 2026 simply because they could now shop the market without re-qualifying. On a $400,000 balance, 0.35% works out to roughly $1,400 per year in interest savings.

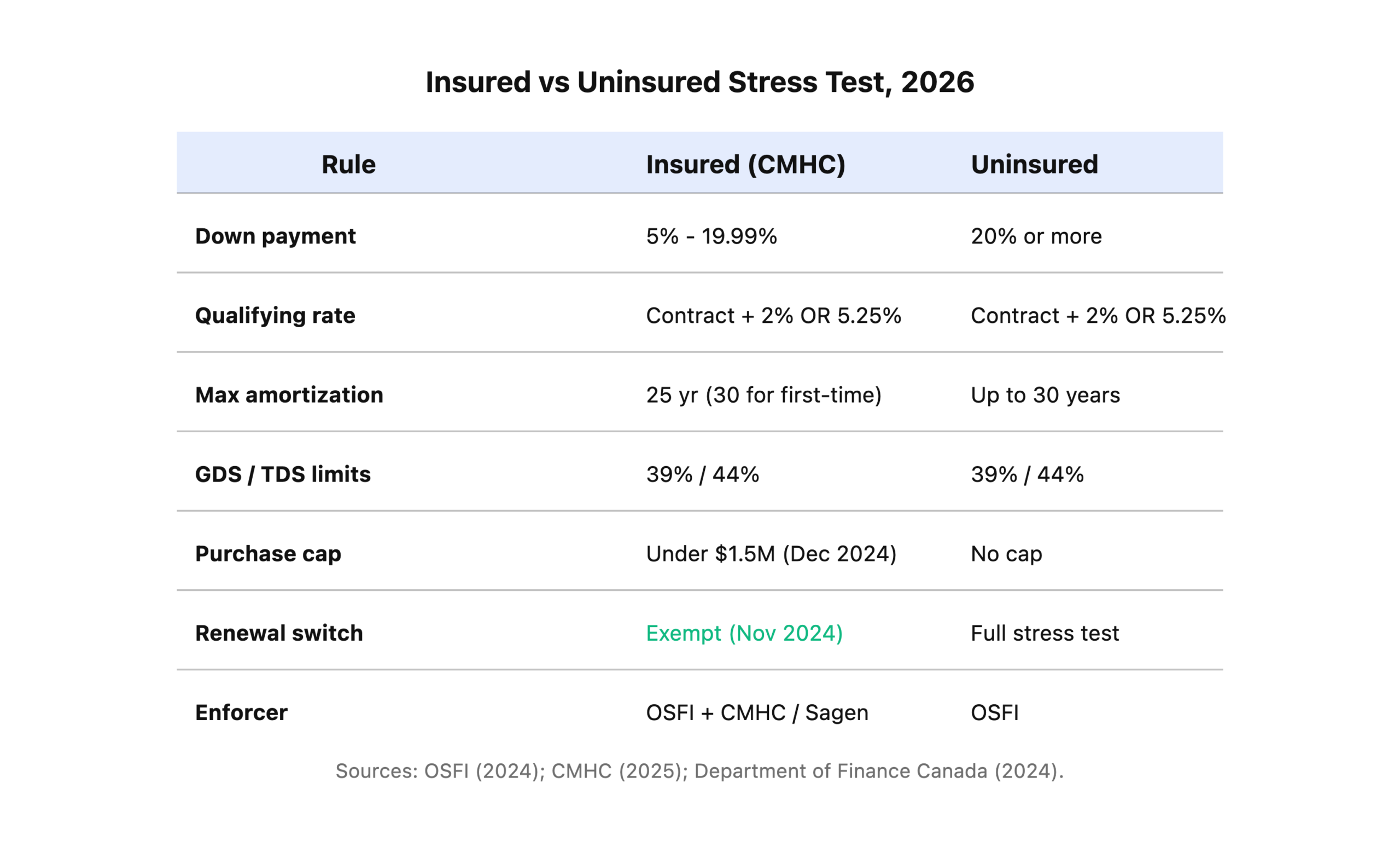

How Does the Insured vs Uninsured Stress Test Differ?

In 2026, insured and uninsured mortgages follow the same qualifying rate formula (contract + 2% OR 5.25%), but differ on who enforces it, which products it covers, and how renewal switches are treated (OSFI, 2024; CMHC, 2025). Understanding the difference matters because it changes your shopping options at every stage.

A few things worth calling out:

- 30-year insured amortization for first-time buyers became permanent in December 2024, and was expanded to new-build purchases for all buyers regardless of first-time status (Department of Finance Canada, 2024). A longer amortization means a lower stressed payment, which means you pass the qualifying rate test on a larger mortgage.

- The insured purchase cap lifted from $1M to $1.5M in December 2024, bringing thousands of Edmonton and Calgary move-up buyers back into insured territory.

- Uninsured borrowers do not get the November 2024 renewal carve-out. If you had 20%+ down originally, you still face the full stress test at switch, which puts you at a disadvantage compared to insured peers.

How Much Does the Stress Test Actually Reduce Your Maximum Purchase Price?

Based on 500+ actual Metro Mortgage Group qualification runs in the past 12 months, the 2026 stress test reduces a typical Edmonton household’s maximum purchase price by roughly 15% to 18% compared to what the contract rate alone would allow (OSFI, 2024). That gap is the difference between buying and being told to wait another year.

Here’s a real Edmonton example we ran this month:

The file: Married couple, combined household income $100,000, $50,000 down payment, car loan at $450/month, no other debts. Edmonton detached target. 5-year fixed contract rate 4.59%, 30-year insured amortization (they qualify as first-time buyers).

Without the stress test (using contract rate 4.59% only):

– Max mortgage: ~$555,000

– Max purchase price: ~$605,000

With the 2026 stress test (qualifying at 6.59%):

– Max mortgage: ~$465,000

– Max purchase price: ~$515,000

The 2021 comparison is even more striking. When contract rates were 2.14% in 2021, the same $100K household (with a smaller car payment and lower property taxes) could qualify for roughly $680,000 — because the 5.25% floor was only about 3 points above the contract rate and total payments were much lower on the real side. The combination of higher contract rates and a higher stress test floor is what stripped $165,000 of purchasing power from the typical Edmonton first-time buyer between 2021 and 2026.

[INTERNAL-LINK: first-time buyer mistakes → https://metromortgagegroup.ca/5-first-time-homebuyer-mistakes-edmonton/]What Can You Do If You Fail the Stress Test?

Roughly 1 in 4 first-time buyer applications we see at Metro don’t pass the stress test on the first run, but most of those files get approved within 30-60 days after targeted fixes (Bank of Canada, 2024). Failing once is a diagnostic, not a verdict. Here are the five fixes that work most often, ranked by speed:

1. Pay Down Unsecured Debt (Fastest Fix)

Every $100/month of credit card or line of credit payment reduces your maximum purchase price by roughly $15,000 to $18,000 under the TDS 44% limit. Paying off a $4,000 credit card balance (~$120/month minimum payment) can unlock $18,000-$20,000 of extra purchase power overnight. This is almost always the first lever we pull.

2. Increase Your Down Payment Slightly

Moving from 5% down to 10% down cuts your CMHC premium from 4.00% to 3.10% and reduces the mortgage balance you need to qualify on (CMHC, 2025). Even an extra $5,000 down payment often tips a borderline file into approval. Combine with a gift letter from parents (allowed on insured files) and the math gets easier fast.

3. Add a Co-Signer or Co-Borrower

A parent co-signer with strong income and clean credit can be the difference between decline and approval. Lenders will combine incomes and credit profiles, though the co-signer’s own debts also enter the calculation. Make sure both parties understand the full legal weight before signing.

4. Extend to 30-Year Amortization

First-time buyers and new-build purchasers can take 30-year insured amortization as of December 2024, which drops the stressed monthly payment by roughly 8-10% (Department of Finance Canada, 2024). On our $100K Edmonton example, going from 25 to 30 years adds about $30,000 of purchase power.

5. Consider a B-Lender (Last Resort)

Some provincially regulated lenders and credit unions operate outside OSFI’s B-20 framework and apply looser qualifying rules. Rates are typically 1.00% to 2.00% higher, and setup fees apply, but for self-employed borrowers or those with credit bruises, a B-lender path can bridge you to an A-lender refinance in 1-2 years. We use this route sparingly and only when the numbers justify it.

Why Do Canadian Banks Actually Support the Stress Test?

Canadian banks publicly support the stress test because it has kept mortgage arrears near historical lows — the national 90+ day mortgage arrears rate was 0.20% in Q4 2024, one of the lowest figures among developed economies (Canadian Bankers Association, 2024). Low defaults protect bank balance sheets, reduce CMHC insurance payouts, and keep the entire housing finance system stable.

The counterintuitive truth about the stress test is that it protects you more than it protects the bank. Banks are insured on high-ratio mortgages through CMHC, Sagen, or Canada Guaranty — if you default, they get paid. The stress test exists primarily to prevent borrowers from losing their homes, their down payments, and their credit in a rate-shock scenario. OSFI’s own 2024 analysis found that borrowers who passed the stress test at origination were roughly three times less likely to fall into arrears when renewal rates spiked in 2023-2024 (OSFI, 2024).

That doesn’t make the stress test feel any better when it knocks $90,000 off your max purchase price. But it does explain why OSFI has refused to remove it despite persistent industry lobbying — the default protection math works.

Ready to Find Out What You Actually Qualify For in 2026?

The only way to know your real 2026 stress test number is to run a full qualification with a broker who can test multiple lenders, amortizations, and rate products side-by-side. At Metro we do this free of charge for every Edmonton and Alberta buyer, usually within 24-48 hours of receiving your documents. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

If you want to budget the full purchase picture first, start with our closing costs Alberta 2026 breakdown and our guide on how much down payment you actually need in Alberta. Together with this stress test post, they’re the three numbers every Edmonton first-time buyer needs before house hunting.

Frequently Asked Questions

What is the mortgage qualifying rate in Canada for 2026?

The 2026 mortgage qualifying rate is your contract rate + 2%, OR 5.25%, whichever is higher — a formula in place since June 2021 under OSFI Guideline B-20 (OSFI, 2024). On a 4.59% contract rate, that means you qualify at 6.59%. The 5.25% floor only applies if your contract rate drops below 3.25%.

Does the stress test apply when I renew my mortgage in 2026?

Not if you have an insured mortgage and you’re doing a straight switch to another lender — OSFI removed that requirement in November 2024 (OSFI, 2024). Uninsured borrowers still face the full stress test at switch. Staying with your current lender at renewal has never required a stress test, regardless of insured status.

How does the stress test affect a $100K household in Edmonton?

On $100,000 household income in Edmonton, the 2026 stress test reduces maximum purchase price by roughly $90,000 — from about $605,000 to $515,000 on an insured 30-year first-time buyer file (CMHC, 2025). That’s around 15% of purchasing power stripped out purely for qualification safety.

Can I skip the stress test by using a credit union or private lender?

Some provincially regulated credit unions and private lenders operate outside OSFI B-20 and apply looser qualifying rules, but rates typically run 1.00% to 2.00% higher and setup fees apply (Financial Consumer Agency of Canada, 2025). It’s a legitimate Plan B for self-employed or credit-challenged borrowers, but not a free workaround.

Has the stress test ever been removed or paused?

No — the stress test has been continuously in place since January 2018 for insured mortgages and has only tightened since, moving from the Bank of Canada 5-year benchmark to the current 5.25% floor in June 2021 (Department of Finance Canada, 2021). The only carve-out is the November 2024 insured switch exemption at renewal.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and has helped Edmonton and Alberta families secure mortgages since 2011. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: April 27, 2026