Fixed vs Variable Mortgage in Edmonton

How to choose between rate stability and floating with the Bank of Canada

A York University study spanning 1950 to 2007 found that variable-rate mortgage holders paid less interest than fixed-rate borrowers roughly 90% of the time over any given five-year period (Ratehub, citing Dr. Moshe Milevsky, 2001). That’s a powerful stat — but it doesn’t tell you what to do in 2026, when the Bank of Canada has held its policy rate at 2.25% and geopolitical tension is pushing bond yields (and fixed rates) higher (Bank of Canada, 2026).

Here’s how to decide between variable and fixed for your Edmonton purchase or renewal — with real numbers, not gut feelings.

Key Takeaways

– As of spring 2026, the best 5-year variable rate in Canada sits near 3.35% while the best 5-year fixed is roughly 4.04% — a spread of about 69 basis points (Ratehub, 2026).

– Historically, variable-rate borrowers have saved money roughly 90% of the time over any 5-year term (York University / Milevsky, 2001).

– The 2025 CMHC Mortgage Consumer Survey found 62% of borrowers chose fixed while 25% chose variable (CMHC, 2025).

– Variable mortgages carry a 3-month interest penalty to break early; fixed mortgages use the higher of 3-month interest OR the interest rate differential (IRD) — which can be 10x larger.

– Edmonton’s average home price hit $454,801 in February 2026, up 1.5% year-over-year (WOWA / CREA, 2026).

How Does a Fixed-Rate Mortgage Work?

A fixed-rate mortgage locks your interest rate for the entire term — typically three or five years in Canada. Your payment stays identical from month one to the final payment of the term, regardless of what the Bank of Canada does with its overnight rate. Fixed rates are priced off Government of Canada bond yields, not the BoC policy rate directly (Ratehub, 2026).

That predictability comes at a cost. Fixed rates are almost always higher than variable rates at the time of signing because the lender is absorbing the risk that rates might rise during your term. In April 2026, the best insured 5-year fixed rate is approximately 3.89%, while uninsured sits closer to 4.04% (Ratehub, 2026).

The other hidden cost? Break penalties. If you sell, refinance, or need to break your fixed mortgage early, the lender charges the greater of three months’ interest OR the interest rate differential (IRD). On a $450,000 mortgage at 4.04%, the IRD penalty can easily exceed $10,000 to $15,000 depending on remaining term and current rates.

For a full breakdown of what to budget beyond your down payment, see our closing costs guide.

How Does a Variable-Rate Mortgage Work?

A variable-rate mortgage is tied to your lender’s prime rate, which moves in lockstep with the Bank of Canada’s overnight rate. Your rate is expressed as “prime minus” or “prime plus” a discount — for example, prime minus 0.60%. With the current prime rate at 4.45%, that would give you an effective rate of 3.85% (Ratehub, 2026).

There are two flavours of variable in Canada:

- Adjustable-rate mortgage (ARM): your payment changes each time prime moves, so you always pay the correct split of principal and interest.

- Static-payment variable: your payment stays the same, but the split between principal and interest shifts. If rates rise enough, you can hit your trigger rate — the point where your entire payment covers only interest and no principal is being repaid.

Most Edmonton brokers recommend the ARM version in 2026. The static-payment variety created problems for borrowers during the 2022-2023 rate hikes, when some hit trigger rates and saw their amortizations extend to 40+ years.

Not sure how a trigger rate could affect your budget? Use our affordability guide to see how much mortgage you can afford.

Historical Performance: Which Rate Type Actually Wins?

The data overwhelmingly favours variable — but the margin depends on the period you examine. Dr. Moshe Milevsky’s landmark study at York University’s Schulich School of Business analysed data from 1950 to 2007 and found variable-rate borrowers came out ahead roughly 90% of the time over rolling five-year windows (Ratehub, citing Milevsky, 2001). A later CMLS Financial study covering 25 years of data confirmed the pattern, showing variable won in the majority of periods (CMLS, 2023).

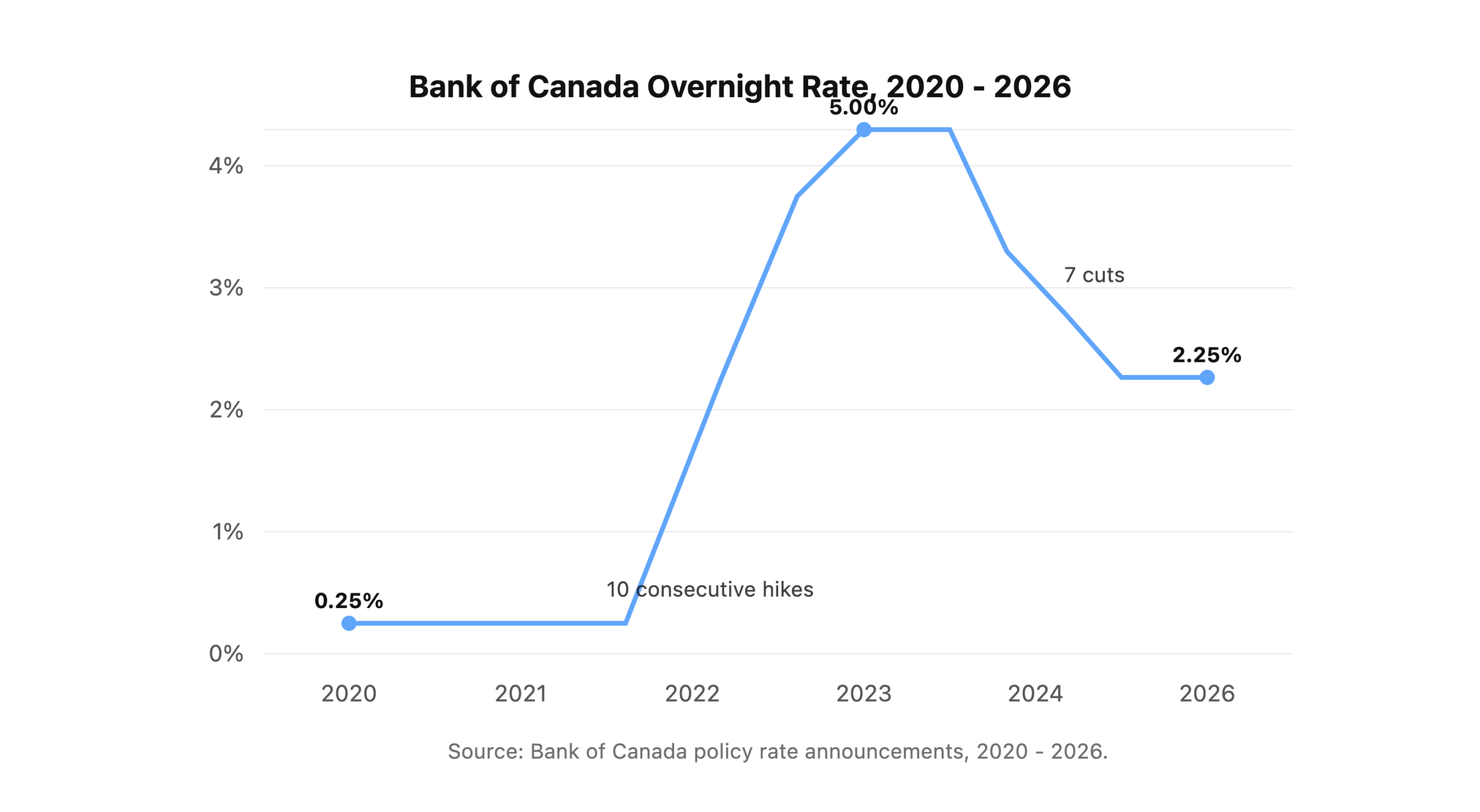

But here’s the caveat: 2022-2024 was the exception. The Bank of Canada hiked its policy rate 10 consecutive times, from 0.25% to 5.00%, in the fastest tightening cycle in Canadian history. During that window, variable-rate borrowers paid substantially more than those locked into pre-2022 fixed rates. It was a painful reminder that historical averages don’t eliminate short-term risk.

The lesson? Variable wins most of the time, but “most of the time” isn’t “all of the time.” Your decision should factor in how much short-term volatility you can absorb financially and psychologically.

Current Rate Environment: Where Do We Stand in 2026?

The Bank of Canada cut its policy rate multiple times through 2024 and into 2025, bringing the overnight rate down from a peak of 5.00% to its current level of 2.25%. The BoC held the policy rate at 2.25% again at its June 10, 2026 announcement, with the next scheduled rate announcement set for July 15, 2026. CPI inflation eased to 1.8% in February 2026, comfortably within the BoC’s 1-3% target band.

Here’s where rates sit as of spring 2026:

| Product | Best Rate (Insured) | Best Rate (Uninsured) |

|---|---|---|

| 5-year fixed | 3.89% | 4.04% |

| 5-year variable | 3.30% | 3.35% |

| 3-year fixed | 3.99% | 4.14% |

| Current spread (5-yr) | 0.59% | 0.69% |

Rates sourced from Ratehub, April 2026. Your actual rate depends on credit, down payment, and property type.

The variable-fixed spread of roughly 60-70 basis points is historically normal. During 2022-2023, the spread inverted — variable was actually higher than fixed — which was an anomaly caused by the fastest rate-hike cycle in BoC history. Today’s positive spread suggests the market has returned to its normal pricing relationship.

Most Bay Street economists expect the BoC to hold at 2.25% through 2026, with Scotiabank being the lone outlier projecting a possible increase to 2.75% if energy prices and tariff-driven inflation accelerate (nesto, 2026).

When Does Variable Win?

Variable tends to outperform fixed in three specific scenarios:

1. Rate-Cutting or Stable Rate Environments

When the Bank of Canada is cutting rates or holding steady, your variable rate stays flat or drops while fixed-rate borrowers are locked into the higher rate they signed at. This is exactly where we sit in 2026 — the BoC has been holding its policy rate steady at 2.25%, most recently reaffirmed at the June 10, 2026 announcement, and inflation is running below target at 1.8%.

2. You Might Move or Refinance Before Term Ends

Here’s where the math gets dramatic. On a $450,000 mortgage at 4.04% fixed with 3.5 years remaining, the IRD break penalty could run $12,000 to $16,000. The same mortgage on a variable rate? Penalty is capped at three months’ interest — roughly $3,750. If there’s any chance you’ll sell your Edmonton home before the five-year mark, variable gives you an exit that won’t gut your equity.

3. You Can Absorb Payment Swings

A 0.25% BoC rate increase on a $450,000 variable mortgage adds roughly $56 per month to your payment. If your budget has that kind of buffer, the statistical advantage of variable — saving money the majority of the time — works in your favour over multiple terms.

First-time buyer in Edmonton? Start with our first-time home buyer guide for the full picture on financing your purchase.

When Does Fixed Win?

Fixed earns its premium in three situations:

1. Aggressive Rate-Hike Cycles

If the BoC were to reverse course and start hiking again — say tariff-driven inflation pushes CPI above 3% — a fixed rate shields you entirely. The 2022-2023 cycle proved that even a “historically better” variable rate can cost thousands more per year in a hiking environment.

2. You’re Stretching Your Budget

If you’re buying at or near your maximum qualification and every dollar of payment predictability matters, fixed eliminates the risk of a surprise increase. Edmonton’s average home price of $454,801 means many first-time buyers are near their ceiling after the stress test. Payment certainty isn’t just emotional comfort — it’s financial safety.

3. You Plan to Hold the Full Term

If you’re confident you won’t sell, refinance, or make major changes for the full five years, the IRD penalty disadvantage of fixed rates becomes irrelevant. You’ll never pay it. In that case, the premium for fixed is purely an insurance cost against rate increases — and whether that insurance is worth 60-70 basis points per year depends on your risk tolerance.

Stress Test Impact: Variable vs Fixed

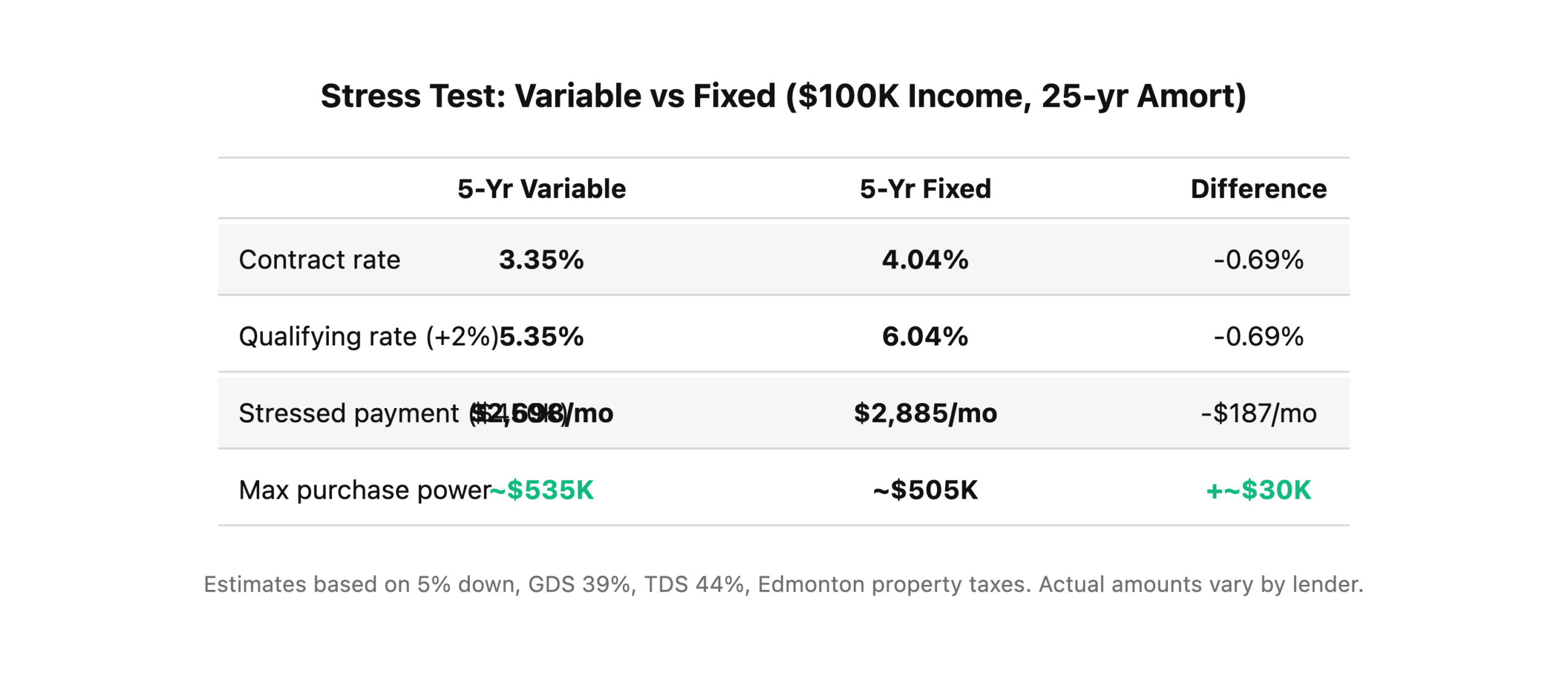

Both variable and fixed mortgages face the same stress test — you qualify at your contract rate + 2% OR 5.25%, whichever is higher (OSFI, 2024). But because variable rates start lower, they can actually give you slightly more purchasing power:

The variable rate’s lower contract rate produces a lower qualifying rate, which translates into roughly $30,000 more purchasing power on a $100,000 household income. For Edmonton buyers competing in a market with an average price of $454,801, that extra headroom can be the difference between getting the home you want and settling.

The Break Penalty Factor: Why It Matters More Than the Rate

Most Edmonton buyers don’t stay in their first home for the full five-year term. The average Canadian mortgage is broken at approximately 3.5 years, according to industry data. That makes the break penalty one of the most underrated factors in the variable vs fixed decision.

Here’s the penalty math on a $450,000 mortgage:

| Scenario | Variable (3-mo interest) | Fixed (IRD) |

|---|---|---|

| Break at year 2 | ~$3,750 | ~$14,000 – $18,000 |

| Break at year 3.5 | ~$3,750 | ~$8,000 – $12,000 |

| Break at year 4.5 | ~$3,750 | ~$3,000 – $5,000 |

The variable penalty is predictable and capped. The fixed penalty depends on the IRD calculation, which varies by lender and can produce eye-watering numbers — especially if rates have dropped since you signed. We’ve seen Metro clients face IRD penalties exceeding $20,000 on relatively modest mortgages.

If you think there’s even a 20% chance you’ll break your mortgage before term, the penalty savings from variable could outweigh any rate advantage from fixed.

Still building your down payment? Our down payment guide breaks down minimums and sources of funds for Alberta buyers.

Decision Framework: 5 Questions to Answer

Not sure which way to lean? Work through these five questions:

1. How long will you stay in this home?

If less than five years: variable’s lower break penalty gives it a structural advantage. If the full term: fixed’s predictability is worth more.

2. Can you absorb a $100-200/month payment increase?

If yes, variable’s historical advantage works in your favour. If that would strain your budget: fixed removes the risk entirely.

3. Where do you think rates are headed?

Most economists expect the BoC to hold at 2.25% through 2026. If you agree, variable saves you money today. If you think tariff-driven inflation could force hikes, fixed is insurance.

4. Is this your first home or a step-up purchase?

First-time buyers tend to move sooner (growing family, job change, upgrade). Variable’s flexibility and lower penalties match that reality. Long-term homeowners who’ve found their “forever” house lean fixed.

5. What keeps you up at night — overpaying or uncertainty?

If the thought of paying more than you need to bothers you most: variable. If the thought of a surprise payment increase keeps you awake: fixed. Neither answer is wrong — it’s about aligning your mortgage with your temperament.

What About a Hybrid Approach?

Some Edmonton buyers split their mortgage — for example, 60% fixed and 40% variable. This hedges your bets: the fixed portion provides stability while the variable portion captures potential savings. According to the CMHC 2025 Mortgage Consumer Survey, 9% of Canadian borrowers chose a combination of fixed and variable (CMHC, 2025).

The trade-off? Two rate products to manage, two potential penalties if you break early, and slightly more complex paperwork. For borrowers who genuinely can’t decide — and who have a mortgage large enough to make the split meaningful — it’s a legitimate middle ground. We typically recommend it for mortgages above $500,000 where the savings potential is worth the added complexity.

Want to run your own numbers? Try our mortgage calculator to model payments under both rate types.

Metro’s Recommendation for Edmonton Buyers in 2026

There’s no universal right answer — but there is a right answer for you, and it depends on the five questions above. Here’s how we’d frame it for most Edmonton buyers in today’s market:

- Leaning variable if you have budget flexibility, might move within 5 years, or want to benefit from a stable/declining rate environment. The 60-70 bps savings over fixed adds up to roughly $3,100 per year on a $450,000 mortgage — that’s real money.

- Leaning fixed if you’re buying at your maximum, plan to stay put for the full term, and sleep better knowing your payment won’t change. The premium is the cost of certainty.

- Consider hybrid if your mortgage exceeds $500K and you truly can’t decide.

Whatever you choose, make sure you’re comparing rates from multiple lenders. As a brokerage with access to 30+ lenders, we consistently find rate differences of 0.20% to 0.40% between the best and worst offers for the same borrower profile. On a $450,000 mortgage, that’s $900 to $1,800 per year in unnecessary interest.

Ready to see both variable and fixed options side-by-side for your situation? Call Metro at 780-974-1270 or email info@MetroMortgageGroup.ca. We’ll run the numbers on both paths — including stress test qualification, break penalties, and total interest cost — within 24-48 hours.

Your credit score plays a big role in the rate you qualify for on either path — see our credit score guide for details.

Frequently Asked Questions

Is variable or fixed better for first-time buyers in Edmonton?

It depends on your timeline and risk tolerance. Variable rates are currently 60-70 basis points lower than fixed (Ratehub, 2026), and first-time buyers statistically move sooner — making variable’s lower break penalty valuable. However, if you’re buying at your maximum and can’t absorb payment swings, fixed offers safety. Most Metro first-time buyers in 2026 are choosing variable when they have at least $200/month of budget buffer.

What happens to my variable rate if the Bank of Canada raises rates?

Each 0.25% BoC rate increase raises your variable rate by the same amount. On a $450,000 mortgage, that’s roughly $56/month per quarter-point hike. If the BoC raised rates by a full 1.00%, your payment would increase by approximately $224/month. The stress test already qualifies you at your rate + 2%, so a 1% increase should be within your tested capacity.

Can I switch from variable to fixed mid-term?

Yes — most lenders allow you to convert from variable to fixed at any time without penalty. However, you’ll lock into the lender’s posted fixed rate at the time of conversion, not the discounted rate you’d get as a new borrower. This is often 0.30% to 0.50% higher than the best available rate. It’s a safety valve, not a free option.

Do variable and fixed mortgages qualify differently under the stress test?

Both face the same stress test formula — contract rate + 2% OR 5.25%, whichever is higher (OSFI, 2024). But because variable rates start lower, they produce a lower qualifying rate, which gives you roughly $30,000 more purchasing power on a $100K income compared to fixed.

Why do most Canadians still choose fixed if variable saves more money historically?

Behavioural finance. The CMHC 2025 Mortgage Consumer Survey found 62% chose fixed (CMHC, 2025). Loss aversion — the pain of a rate increase — is psychologically about twice as powerful as the satisfaction of a rate decrease. Fixed rates sell certainty, and certainty has emotional value that doesn’t show up in spreadsheets. Neither choice is irrational; they just optimise for different things.

About the author: Nathan Danzo is a mortgage broker at Metro Mortgage Group, helping Edmonton and Alberta buyers navigate rate decisions for several years. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: June 9, 2026