When to Lock Your Mortgage Rate

Rate hold timing, market signals, and the cost of waiting in 2026

Between March and April 2026, the lowest insured 5-year fixed rate in Canada rose from 3.79% to 3.89% — a 10-basis-point jump driven by rising Government of Canada bond yields amid geopolitical uncertainty (Ratehub, 2026). For an Alberta buyer with a $450,000 mortgage, that single move added roughly $26/month to their payment — or $1,560 over a 5-year term. That’s the cost of waiting just a few weeks to lock in.

Here’s how rate locks work in Canada, when to lock, when to float, and how to avoid leaving money on the table.

Key Takeaways

– Most Canadian lenders offer 90- to 120-day rate holds at no cost as part of pre-approval — you’re guaranteed the quoted rate even if rates rise before closing (nesto, 2026).

– If rates drop during your hold period, most lenders will honour the lower rate at closing — you’re protected in both directions.

– The Bank of Canada’s policy rate is currently 2.25%, held at its most recent announcement (Bank of Canada, 2026), but fixed rates move independently based on bond yields, which have risen sharply in early 2026.

– Locking a rate is free. There’s no fee to hold a rate, and no penalty if you don’t close with that lender.

– Rate holds apply to fixed-rate mortgages only — variable rates float by design and can’t be locked in advance.

What Is a Mortgage Rate Lock in Canada?

A mortgage rate lock — often called a rate hold in Canadian lending — is a guarantee from your lender that a specific interest rate will be available to you for a set period, typically 90 to 120 days (nesto, 2026). During that window, even if rates increase, your held rate stays the same.

Rate locks are fundamentally different from what you might read about in American mortgage content. In the U.S., rate locks are often tied to specific loan applications and can carry extension fees. In Canada, a rate hold is built into the pre-approval process — it’s standard, free, and available from virtually every lender.

Here’s how the mechanics work:

- You apply for pre-approval with a lender or broker

- The lender offers a rate hold — typically 120 days for Big Six banks, 90-120 days for monoline lenders

- Your rate is guaranteed for that window, regardless of market movement

- If rates drop, most lenders will give you the lower rate at closing (confirm this with your lender — it’s standard practice but not legally required everywhere)

- If you don’t close with that lender, there’s no penalty — the hold simply expires

The rate you’re offered at hold is usually the lender’s best available rate for your profile at that moment — not a posted rate. Your credit score, down payment size, property type, and amortization all affect the specific rate offered.

Ready to start the process? See our first-time buyer guide for a full walkthrough.

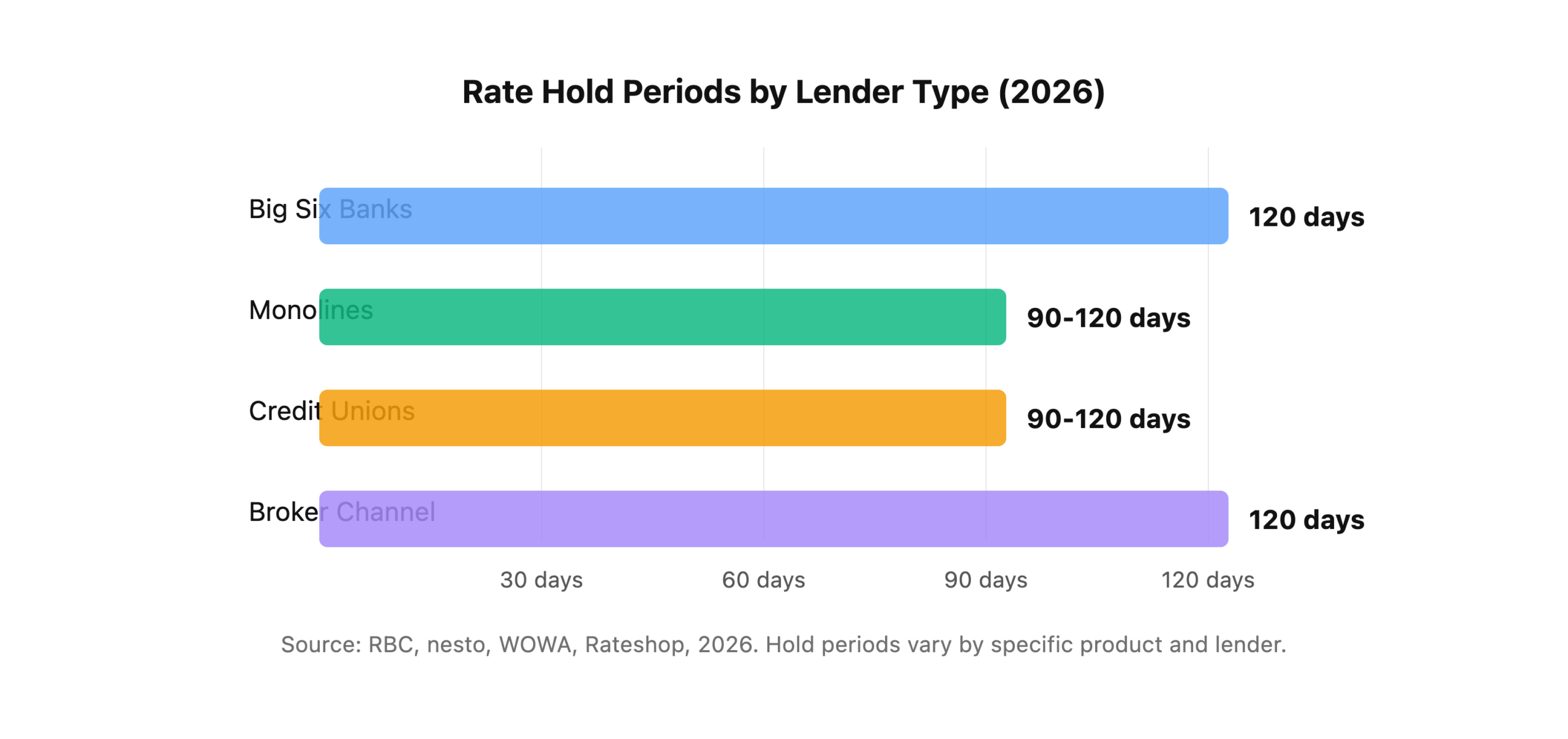

How Long Can You Hold a Mortgage Rate in Canada?

Hold periods vary by lender type, but the standard ranges are well established:

The Big Six banks (RBC, TD, Scotiabank, BMO, CIBC, National Bank) generally offer the longest holds — up to 120 days through their pre-approval programs (RBC, 2026). RBC specifically states they’ll honour the quoted rate on a fixed-rate mortgage for up to 120 days, even if rates go up — and if rates go down, you’ll get the lowest rate in effect for your chosen term.

Monoline lenders (companies like MCAP, First National, CMLS) typically offer 90 to 120 days, depending on the product. Credit unions vary more widely — some provincially regulated credit unions offer as little as 60 days, while larger ones match the 120-day standard.

Through the broker channel, you often get the best of both worlds. Your broker can shop rates from multiple lenders before you commit, then place your hold with the most competitive one. At Metro, we typically hold your rate with one lender at a time while continuously monitoring the broader market — if a better rate appears elsewhere, we can move your file before you close.

Not sure how a rate change affects your budget? Try our mortgage affordability calculator.

Rate Lock vs Float: What’s the Difference?

“Locking” means accepting a rate hold from your lender. “Floating” means choosing not to lock — gambling that rates will drop further before you close. In Canada, floating is less common than in the U.S. because our pre-approval system makes locking essentially free and risk-free (if rates drop, you still get the lower rate).

So why would anyone float?

Floating makes sense when:

– The Bank of Canada is actively cutting rates and you believe another cut is imminent

– Bond yields are trending downward, signalling lower fixed rates ahead

– You have a long timeline before closing (6+ months) and can’t get a hold that covers it

Floating is risky when:

– Bond yields are rising (as they have been in early 2026, driven by energy prices and geopolitical tension)

– Inflation expectations are climbing

– You’re close to your qualification limit and a rate increase could disqualify you

In spring 2026, the argument for locking is stronger than the argument for floating. The BoC policy rate is stable at 2.25%, but fixed rates are driven by bond yields, not the policy rate — and bond yields have been moving up. You could see the BoC hold steady while fixed rates continue to climb.

Still weighing your options? See our variable vs fixed comparison.

The Real Cost of Waiting: A 2026 Illustrative Example

Let’s quantify what “waiting to lock” actually costs. Here’s an illustrative example based on typical Alberta market conditions:

Buyer profile: Edmonton couple, $110,000 combined income, 10% down on a $475,000 home, 5-year fixed, 25-year amortization.

| Timing | 5-Yr Fixed Rate | Monthly Payment | Total Interest (5-yr) |

|---|---|---|---|

| Locked Feb 2026 | 3.79% | $2,217 | $91,430 |

| Locked Apr 2026 | 3.89% | $2,244 | $92,720 |

| If rates hit 4.10% | 4.10% | $2,300 | $95,540 |

| If rates hit 4.30% | 4.30% | $2,356 | $98,380 |

Mortgage amount: $427,500 (90% of $475,000). Calculations assume standard monthly payments on a 25-year amortization.

The buyer who locked in February versus April saved roughly $1,290 over the 5-year term — not life-changing, but real money. If rates continue climbing to 4.30%, the total cost of waiting from February stretches to nearly $6,950. That’s a vacation, a furnace replacement, or six months of property tax.

The opposite scenario matters too: if you lock at 3.89% and rates drop to 3.60%, most lenders will honour the lower rate anyway. You’re protected on the downside. This asymmetry is what makes locking the default smart move — you capture today’s rate while retaining the benefit of any future drop.

For a full picture of what you’ll pay at closing, see our closing costs breakdown.

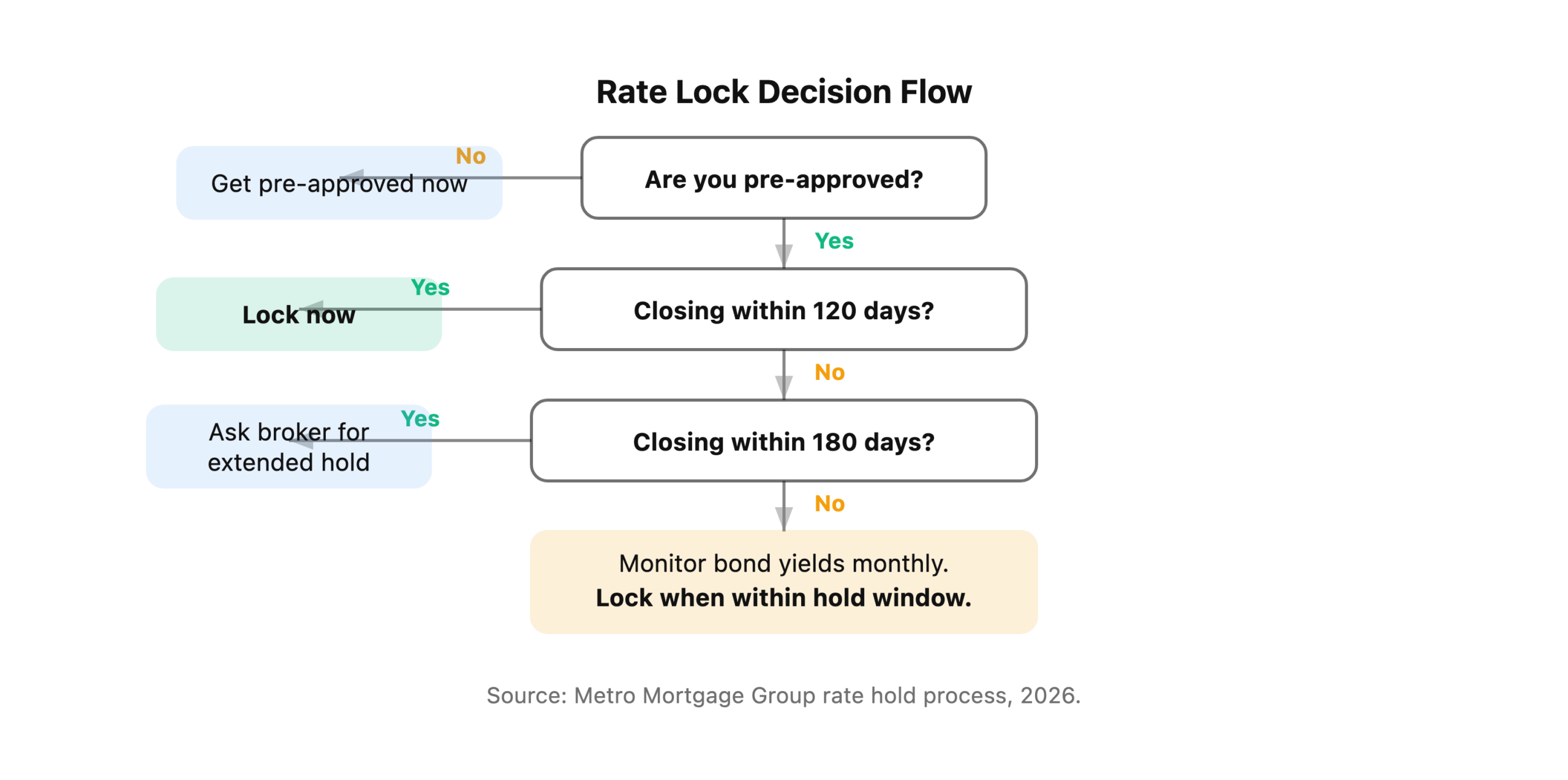

Five Factors That Should Drive Your Lock Timing

1. Your Closing Date Distance

If your closing is within 120 days, lock immediately. There’s no strategic benefit to waiting when you can hold today’s rate and still get any future drop. The 120-day hold from most lenders covers the typical purchase timeline from accepted offer to closing.

If closing is more than 120 days away, you can’t hold yet with most lenders. In that case, watch bond yields and lock as soon as you enter the hold window. Some brokers can arrange extended holds of 130-150 days through specific lender relationships — ask your broker.

2. Bond Yield Direction

Fixed mortgage rates track the Government of Canada 5-year bond yield, not the Bank of Canada policy rate. In early 2026, bond yields have risen due to global uncertainty, pushing fixed rates higher even though the BoC hasn’t moved. If the 5-year bond yield is trending up, lock sooner. If it’s trending down, you have more room to wait — but remember, the hold protects you from increases anyway.

3. Your Qualification Margin

Are you qualifying with room to spare, or are you right at the edge of the stress test? If you’re close to your GDS 39% or TDS 44% limit, even a small rate increase could push you out of qualification. In that case, lock immediately — losing your qualification is far worse than missing a potential rate drop.

4. Bank of Canada Announcement Schedule

The BoC announces rate decisions on eight fixed dates per year (Bank of Canada, 2025). While BoC changes primarily affect variable rates, they also influence market sentiment and bond yields. If an announcement is coming and the market expects a hold or cut, you might wait to see if it pulls fixed rates down. If a hike is possible, lock before the announcement.

The Bank of Canada’s most recent announcement was June 10, 2026, when it held the policy rate at 2.25%. The next scheduled announcement is July 15, 2026.

5. Renewal vs New Purchase

If you’re renewing, you can lock a rate up to 120 days before your renewal date with a new lender, even before starting the switch process (WOWA, 2026). This gives you a safety net: if rates rise before renewal, you have your held rate. If rates drop, you renegotiate. For insured mortgages, the November 2024 OSFI change means you can now shop at renewal without re-qualifying under the stress test (OSFI, 2024).

If you’re making a new purchase, lock the moment you’re pre-approved. You can always shop for a better rate with other lenders while your hold is active — multiple holds from multiple lenders cost nothing.

What About Locking a Variable Rate?

Short answer: you can’t. Variable rates float by definition — they move with your lender’s prime rate, which tracks the Bank of Canada overnight rate. There’s no mechanism to “hold” a variable rate because the rate will change throughout your term regardless.

What you can hold is the discount to prime. When a lender offers you prime minus 0.60%, that discount is typically guaranteed at pre-approval and honoured at closing. The discount itself doesn’t change — only prime does. So if prime drops between your pre-approval and closing, your effective rate drops too. If prime rises, your rate rises, but your discount stays the same.

For Alberta buyers choosing variable in 2026, the relevant question isn’t “when to lock” but rather “is the discount to prime competitive enough?” The best 5-year variable rates currently offer discounts around prime minus 1.10%, producing an effective rate near 3.35% (Ratehub, 2026).

For more on how the two options compare, see our variable vs fixed guide.

Metro’s Rate Hold Process: How We Handle It

At Metro Mortgage Group, we approach rate holds as a multi-lender strategy, not a single-shot decision. Here’s what our process looks like for Alberta buyers:

-

Initial consultation: We review your income, debts, credit, and property goals. This takes 15-20 minutes by phone or video.

-

Multi-lender rate check: We pull rate options from our network of 30+ lenders and identify the most competitive hold for your profile.

-

Rate hold placement: We typically place your hold with one lender at a time — the one offering the most competitive rate for your profile — while we keep monitoring the rest of the market.

-

Market monitoring: Between your hold date and closing, we watch bond yields and lender rate sheets. If a better rate appears, we renegotiate or switch your file to the stronger offer — usually within 24 hours.

-

Closing day rate check: On closing day, if rates have dropped below your held rate, we confirm the lower rate with your lender. If rates have risen, your hold protects you.

This entire process is free to you — broker compensation comes from the lender, not the borrower, on standard residential mortgages in Alberta.

The advantage of working with a broker versus a single bank should be obvious here: a bank can only hold their own rate. We compare rates across our full lender network and hold with whichever one offers the best outcome for you, while continuing to monitor the rest of the market for a better deal.

Curious how your credit profile affects your rate? See our credit score guide.

Common Rate Lock Mistakes to Avoid

Mistake 1: Not locking because you think rates will drop further.

This is the classic floating error. In a stable or rising rate environment like spring 2026, the downside risk (rates climb) outweighs the upside potential (rates drop) — especially since most lenders honour the lower rate at closing anyway. Lock and let the hold work for you.

Mistake 2: Only holding with one lender.

A single hold means a single option. If a competing lender drops their rate mid-hold, you’re stuck. Multiple holds give you pricing flexibility at zero cost.

Mistake 3: Waiting until your offer is accepted to seek pre-approval.

By the time your offer is accepted, you’re on a closing timeline and rates may have moved. Get pre-approved (and locked) before you start making offers. In Edmonton’s market, sellers also prefer pre-approved buyers — it strengthens your offer.

Mistake 4: Confusing a rate hold with a mortgage commitment.

A rate hold is not a binding agreement to borrow. It’s a guarantee that a specific rate will be available if you choose to proceed. You can walk away from any held rate with no penalty. Don’t let the fear of “commitment” stop you from locking.

Mistake 5: Ignoring the hold expiry date.

Rate holds have hard expiration dates. If your closing is delayed beyond the hold window, you’ll need to renegotiate — potentially at a higher rate. Know your expiry date and build buffer into your closing timeline.

Ready to Lock Your Rate?

The best time to lock a mortgage rate in Alberta is the moment you’re pre-approved — assuming your closing falls within the hold window. It costs nothing, protects you from increases, and still lets you benefit from any decreases. There’s genuinely no downside.

At Metro Mortgage Group, we place your hold with the most competitive lender for your profile and monitor the market between your hold date and closing. If a better rate appears, we move your file — usually within 24 hours. Call 780-974-1270 or email info@MetroMortgageGroup.ca to start your pre-approval and secure today’s rate.

If you’re still deciding between variable and fixed before locking, read our variable vs fixed mortgage comparison for Edmonton buyers — it covers current rates, historical performance, and a 5-question decision framework.

Also worth reading: our down payment requirements guide, our FHSA guide, and our RRSP Home Buyers’ Plan guide.

Frequently Asked Questions

Is there a fee to lock a mortgage rate in Canada?

No — rate holds are free through virtually every Canadian lender and broker. The hold is part of the standard pre-approval process. You pay nothing to hold, nothing to extend (if the lender allows it), and nothing if you walk away and close with a different lender. There’s no catch.

Can I lock a mortgage rate without a pre-approval?

Not formally. The rate hold is issued as part of the pre-approval, which requires a credit check and income verification. Some brokers will give you a verbal “rate indication” before pre-approval, but it’s not a guaranteed hold. To get a real lock, you need a real pre-approval — which typically takes 24-48 hours once you submit your documents.

What happens if my rate hold expires before closing?

You’ll need to renegotiate your rate at whatever the current market rate is on the day your hold expires. If rates have risen, you’ll pay the higher rate. This is why it’s important to build buffer time into your hold — if your closing is 100 days out, a 120-day hold gives you a 20-day cushion for delays. At Metro, we track all expiry dates and start renegotiating well before they hit.

Do rate holds apply to mortgage renewals?

Yes. If your renewal is coming up within 120 days, you can get a rate hold from a new lender or your existing one (WOWA, 2026). For insured mortgages, the November 2024 OSFI change removed the stress test for straight switches at renewal, making it easier to shop around (OSFI, 2024). We recommend starting the renewal shopping process at least 4 months before your maturity date.

Should I lock now or wait for the next Bank of Canada announcement?

If you’re within the hold window and can lock today, lock today. The hold protects you from increases, and most lenders will honour a lower rate if rates drop after an announcement. Waiting adds risk with no upside — the hold itself is your insurance policy in both directions. The Bank of Canada held its policy rate at 2.25% at its June 10, 2026 announcement; the next scheduled announcement is July 15, 2026 (Bank of Canada, 2025).

About the author: Miguel Cunha is a mortgage broker at Metro Mortgage Group, specializing in rate strategy and renewal optimization for Edmonton and Calgary clients. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: July 7, 2026