5-Year Fixed Mortgage Rates in Alberta

Why the 5-year fixed is Canada’s most popular term — and when it isn’t right for you

The 5-year fixed mortgage rate in Alberta sits near 3.64% insured as of early June 2026 — roughly 25 basis points below where it started the year and a full 40-60 bps cheaper than what the Big Five banks post on their websites (WOWA, June 2026). But here’s what most Alberta buyers don’t realize: your 5-year fixed rate has almost nothing to do with the Bank of Canada. It’s driven by bond yields, lender spreads, and whether you’re shopping through a broker or walking into a branch unprepared.

Key Takeaways

– Best 5-year fixed insured mortgage rates in Alberta sit near 3.64%-3.79% as of June 2026, with uninsured rates 10-20 bps higher (WOWA, June 2026).

– Fixed rates are set by the 5-year Government of Canada bond yield (currently ~2.65%), not the Bank of Canada’s overnight rate (Bank of Canada, 2026).

– The spread between broker-access rates and Big Five posted rates is 40-60 basis points, worth roughly $10,000-$14,000 in interest over a 5-year term on a $450,000 mortgage.

– Fixed vs variable: with the spread at ~60 bps favouring variable, fixed still wins for borrowers who can’t absorb a 75 bps upside shock.

What Drives the 5-Year Fixed Mortgage Rate in Alberta?

Your 5-year fixed rate is not set by the Bank of Canada. That’s the single most important thing to understand before you shop for a mortgage, and it’s the thing most rate commentary gets wrong. The Bank of Canada’s overnight rate — currently 2.25%, held at the June 10 announcement — directly controls variable mortgage rates through the prime rate. Fixed rates march to a different drummer entirely.

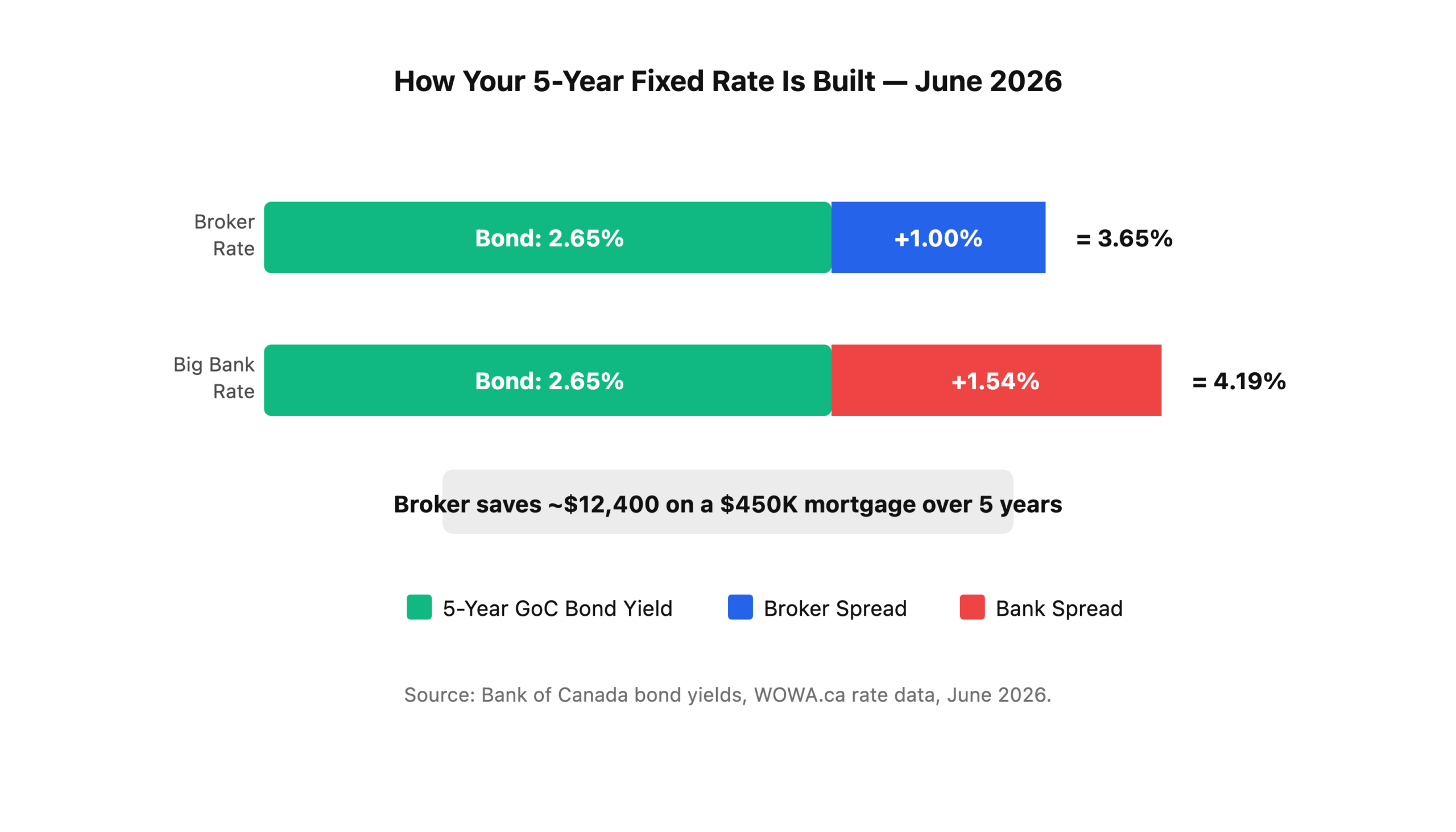

The 5-year Government of Canada bond yield is the benchmark that determines your 5-year fixed rate. When institutional investors buy and sell Government of Canada bonds on the open market, the yield on those bonds moves up or down. Lenders then add a spread — typically 100-150 basis points — on top of that yield to arrive at the fixed mortgage rate they offer you (Bank of Canada, 2026).

As of early June 2026, the 5-year GoC bond yield sits near 2.65%, down from 3.06% in early April (Bank of Canada, 2026). Add a typical broker-channel spread of 100-110 bps, and you get an insured 5-year fixed rate of roughly 3.64%-3.79%. Add a Big Five bank spread of 140-160 bps, and you get their posted rate of 4.19%-4.29%. Same bond yield. Vastly different rates. The difference is the channel.

Why the gap? Big Five banks build in branch overhead, shareholder margins, and the cost of having a teller greet you by name. Mortgage brokers work on thinner margins, access wholesale lender pricing, and compete purely on rate. Neither model is inherently better — but if rate is your priority, the broker channel consistently delivers lower fixed rates across Alberta.

Current 5-Year Fixed Rates in Alberta (June 2026)

Here’s where Alberta’s 5-year fixed rates sit right now, broken down by lender type and insurance status. These are real rates available to qualified Alberta borrowers this week, not promotional teasers:

| Lender Type | 5-Year Fixed Insured | 5-Year Fixed Uninsured | Notes |

|---|---|---|---|

| Broker-access (best) | 3.64%-3.74% | 3.74%-3.89% | Monoline lenders via broker |

| Credit unions (ATB, Servus) | 3.79%-3.94% | 3.89%-4.04% | Negotiable at branch |

| Big Five banks (posted) | 4.19%-4.34% | 4.29%-4.49% | Negotiable, rarely advertised best |

| Big Five banks (negotiated) | 3.89%-4.09% | 3.99%-4.19% | Ask for “best rate” explicitly |

Source: Ratehub, WOWA, lender rate sheets, June 2026.

The gap between the best broker rate and the Big Five posted rate is currently 55-60 basis points. On a $450,000 Alberta mortgage amortized over 25 years, that difference works out to roughly $125-$140 per month — or approximately $7,500-$8,400 over a 5-year term in pure interest savings (Ratehub, June 2026). That’s real money, and it’s available to anyone willing to make a phone call.

Insured vs uninsured: why the gap?

If your down payment is less than 20%, your mortgage is insured through CMHC, Sagen, or Canada Guaranty. That insurance protects the lender against default, which means they take on less risk and can offer a lower rate — typically 10-20 bps cheaper than an uninsured mortgage with 20%+ down (CMHC, 2026). It sounds backwards, but it’s real: putting less down can actually get you a better rate. The catch? You’re paying an insurance premium (typically 2.8%-4.0% of the mortgage amount) that gets added to your balance.

Historical Context: Where Have 5-Year Fixed Rates Been?

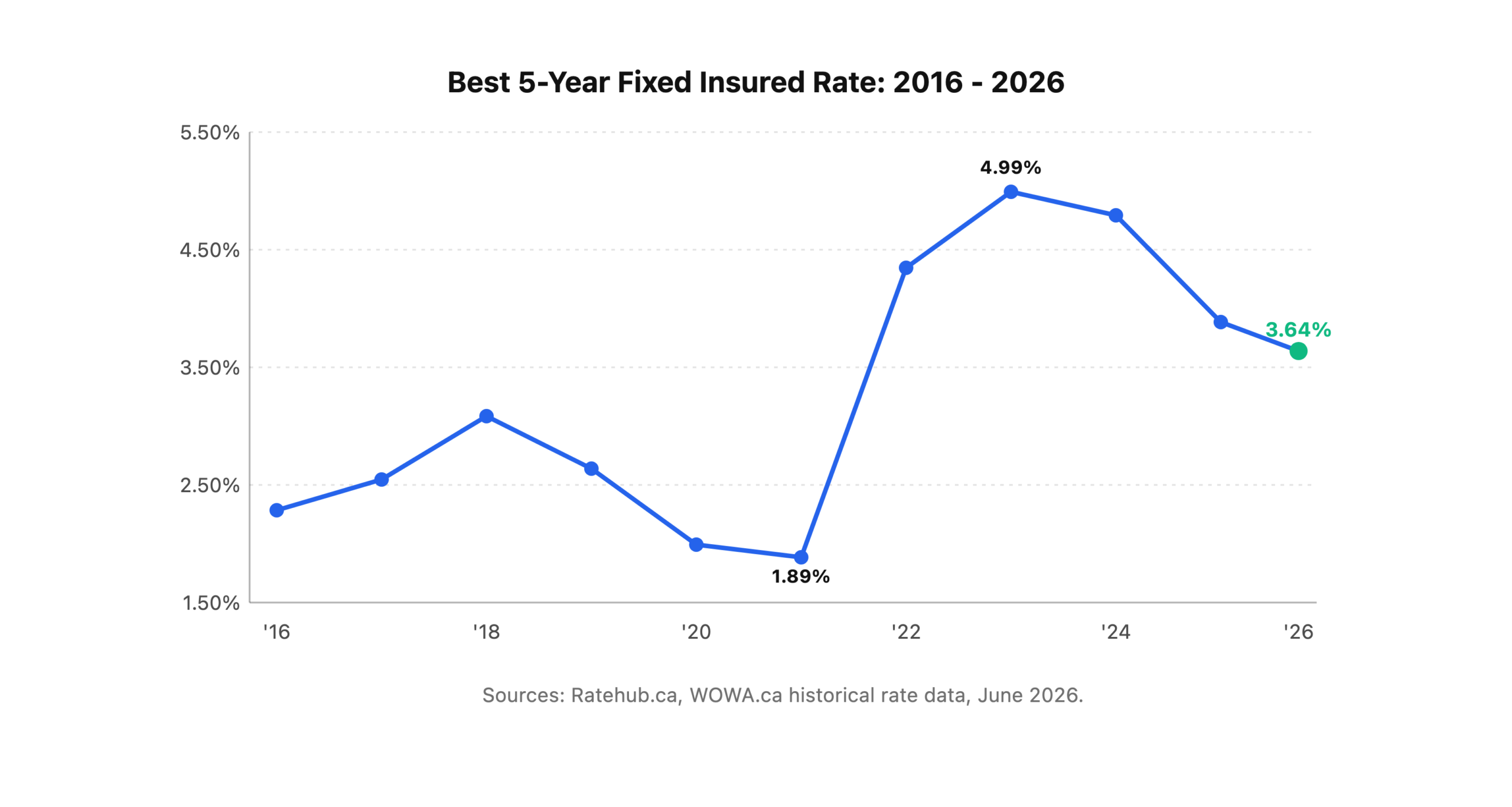

To understand whether today’s rates are good, you need context. Here’s where the best 5-year fixed insured rates have sat at key points over the past decade:

| Period | Best 5-Year Fixed Insured | Context |

|---|---|---|

| June 2016 | 2.29% | Post-oil crash, BoC at 0.50% |

| June 2019 | 2.64% | Pre-pandemic, BoC at 1.75% |

| June 2021 | 1.89% | Pandemic lows, BoC at 0.25% |

| June 2022 | 4.34% | Aggressive tightening begins |

| June 2023 | 4.99% | Near peak, BoC at 4.75% |

| June 2024 | 4.79% | First BoC cut cycle starts |

| June 2025 | 3.89% | Mid-easing, BoC at 2.75% |

| June 2026 | 3.64% | Held June 10, BoC at 2.25% |

Sources: Ratehub historical rates, Bank of Canada, WOWA.

Today’s 3.64% is not a generational low — those happened in 2020-2021 when pandemic-era central bank intervention pushed rates below 2%. But it is comfortably below the 10-year average of roughly 3.50%-4.00%, and it’s dramatically better than the 4.99% peak buyers were dealing with just three years ago. If you bought or renewed in 2023 at close to 5%, a rate of 3.64% at your next renewal represents a meaningful reduction in your monthly payment.

When Should You Choose a 5-Year Fixed Rate?

Not everyone should lock into a 5-year fixed. But there are specific situations where it’s clearly the right move, and others where variable makes more sense. Here’s the honest breakdown.

Fixed is the right choice when:

You’re at your payment ceiling. If your household budget can’t absorb another $150-$200 per month without stress, a 5-year fixed at 3.64% eliminates the risk entirely. You know exactly what you’re paying until June 2031. That certainty has real value, especially for first-time buyers stretching to qualify under the mortgage stress test.

You’re renewing from a 2021 ultra-low rate. If you locked in at 1.89%-2.49% in 2021, your renewal is going to sting no matter what. But locking a 5-year fixed now at 3.64% gives you a predictable adjustment period. Going variable adds rate risk on top of an already painful payment increase.

You sleep better with certainty. This isn’t a weakness — it’s self-knowledge. If you’ll check your mortgage rate every time the Bank of Canada meets, fixed is the product that lets you forget about interest rates for five years and focus on everything else.

Variable makes more sense when:

You can absorb a 75 bps upside. If your budget can handle your payment climbing by $175-$200 per month on a $450K mortgage without breaking, variable at ~3.05% saves you roughly $60-$70 per month out of the gate. Over five years, that adds up — especially if the Bank of Canada delivers one or two more cuts.

You plan to sell or refinance before the term ends. Variable mortgages carry a three-month interest penalty for early termination. Fixed mortgages carry an interest rate differential (IRD) penalty that can run into five figures. If there’s any chance you’ll move, upsize, or refinance within 3-4 years, variable’s lighter penalty structure is a significant advantage. Read our rent vs buy breakdown for more on timing your purchase.

You believe the Bank of Canada will cut further. Markets are pricing in one more 25 bps cut before year-end, which would drop prime to 3.95% and pull the best variable rates toward 2.80% (Reuters, June 2026). If that plays out, variable wins decisively.

5-Year Fixed Rates Across Lender Types in Alberta

Not all lenders are created equal, and the type of institution you get your mortgage from matters as much as the rate itself. Here’s how the landscape breaks down for Alberta borrowers in 2026.

Monoline lenders (via broker)

Companies like First National, MCAP, RMG, and Merix don’t have branches. They originate mortgages exclusively through brokers and pass the cost savings on through lower rates. Best 5-year fixed insured rates from monolines are currently 3.64%-3.74% in Alberta. The trade-off: no branch to walk into, and prepayment privileges vary by product. But for rate-conscious Alberta buyers, monolines consistently beat banks.

Credit unions (ATB, Servus, Connect First)

Alberta’s credit unions sit between brokers and banks on pricing, typically 3.79%-3.94% for a 5-year fixed insured. ATB Financial, which operates like a bank but is provincially owned, often has competitive promotions and is more flexible on non-standard properties (acreages, rural lots) than monolines. If you’re buying outside Edmonton or Calgary city limits, credit unions deserve a look.

Big Five banks

TD, RBC, BMO, CIBC, and Scotiabank post 5-year fixed rates in the 4.19%-4.34% range. These are negotiable — walk in with a competing broker quote and most branch mortgage specialists will sharpen their rate by 30-50 bps. But even their “best” negotiated rates typically land at 3.89%-4.09%, still 25-40 bps above what a broker can access. The banks compete on convenience, bundled products, and relationship pricing for high-net-worth clients — not on raw rate.

What about online-only lenders?

Platforms like Nesto and Pine offer fixed rates competitive with broker-access monolines, typically 3.64%-3.79%. The experience is fully digital. If you’re comfortable with a self-serve application process and don’t need hand-holding, these can be excellent options. But if your file has any complexity — self-employed income, rental properties, non-standard down payment sources — you’ll likely get better results with a broker who can advocate on your behalf.

What Could Move Fixed Rates This Summer?

The June 10 Bank of Canada decision won’t directly move your fixed rate — but it will move market expectations, and those expectations feed into bond yields. Here are the three scenarios I’m watching:

Scenario 1: BoC holds at 2.25% (confirmed outcome). Bond yields stay near 2.65%, and 5-year fixed rates hold in the 3.64%-3.79% range through July. This is the base case, and it means today’s rates stick around for at least another six weeks.

Scenario 2: BoC cuts 25 bps to 1.75%. If inflation continues softening and the labour market weakens further, the Bank could cut again. Bond yields would likely dip toward 2.45%-2.50%, and fixed rates could drift to 3.49%-3.64% — the best fixed rates we’d have seen since early 2022. This is a 25-30% probability in current swap pricing.

Scenario 3: US Treasury yields spike. Canadian 5-year bond yields track US 5-year Treasuries with a correlation above 0.85 most years. If the US Fed signals a hawkish pause or US inflation reaccelerates, Canadian bond yields could push back above 3.00%, and fixed rates would drift toward 3.89%-4.04% regardless of what the Bank of Canada does. This is the tail risk most Alberta borrowers aren’t pricing in.

Here’s what I tell every Metro client shopping for a 5-year fixed: don’t try to time the absolute bottom. The difference between today’s 3.64% and a possible 3.49% in August is about $30 per month on a $450,000 mortgage. The difference between locking at 3.64% and missing your window if bonds spike is $90-$120 per month. The asymmetry favours locking when you find a rate you can live with. Our how much mortgage can I afford calculator can help you test your comfort zone.

The Metro Advantage on Fixed Rates

Metro Mortgage Group accesses 30+ lenders for every Alberta client — which means we’re not limited to one institution’s rate sheet. When you call a bank, you get that bank’s rate. When you call Metro, we pull rate sheets from every monoline, credit union, and institutional lender we have access to, and quote you the lowest rate you qualify for. The result is consistently 40-60 basis points below Big Five posted rates on 5-year fixed products.

On a $500,000 Edmonton mortgage at today’s spread, that’s roughly $14,000 in interest savings over a 5-year term. And it costs you nothing extra — our compensation comes from the lender, not from you.

Beyond rate, we negotiate prepayment privileges (most monolines offer 15-20% annual prepayment vs the standard 10%), portability terms (critical if you’re buying your first home and might move within 5 years), and penalty structures that protect you if life changes.

Frequently Asked Questions

What is the best 5-year fixed mortgage rate in Alberta right now?

As of June 2026, the best insured 5-year fixed mortgage rate in Alberta sits near 3.64%, available through broker-access monoline lenders. Uninsured rates (20%+ down payment) are typically 10-20 bps higher at 3.74%-3.89%. Big Five bank posted rates are 4.19%-4.34%, though these are negotiable down to about 3.89%-4.09% with a competing quote.

Why is the 5-year fixed rate different from the Bank of Canada rate?

The Bank of Canada’s overnight rate (currently 2.25%) controls variable mortgage rates through the prime rate. Fixed rates are determined by the 5-year Government of Canada bond yield, which is traded on the open market and influenced by inflation expectations, US Treasury yields, and global economic conditions. The two rates can move in opposite directions.

Is a 5-year fixed or variable mortgage better in 2026?

It depends on your risk tolerance and budget flexibility. Variable is currently ~60 bps cheaper (3.05% vs 3.64%), saving roughly $65 per month on a $450K mortgage. But variable exposes you to rate increases if the Bank of Canada reverses course. If you can absorb a $150-$200/month payment increase, variable has historically outperformed fixed over most 5-year periods. If you can’t, fixed provides certainty. Our team can run both scenarios against your actual numbers — call 780-974-1270.

Should I wait for rates to drop further before locking in?

Waiting is a gamble. Markets are pricing one more possible 25 bps Bank of Canada cut, which could pull fixed rates down 10-15 bps. But an unexpected US Treasury spike could push rates 25-40 bps higher overnight. The risk is asymmetric — the potential downside of waiting is larger than the potential savings. If today’s rate fits your budget, lock it.

How much does a 5-year fixed mortgage cost per month in Edmonton?

On a $450,000 mortgage at 3.64% amortized over 25 years, your monthly payment would be approximately $2,282. At a Big Five posted rate of 4.19%, the same mortgage costs $2,424 — a difference of $142 per month or $8,520 over the 5-year term. For help calculating your specific scenario, see our down payment guide.

Get Your Best 5-Year Fixed Rate This Week

Whether you’re buying your first home in Edmonton, renewing an existing mortgage, or refinancing to consolidate debt, the first step is finding out what rate you actually qualify for — not the posted rate, not the advertised teaser, but the real rate based on your credit, income, and property. Metro Mortgage Group pulls quotes from 30+ lenders and delivers the lowest available rate at no cost to you. Call 780-974-1270 or email info@MetroMortgageGroup.ca for a free rate comparison.

For more context on where the market is headed, read our June 2026 Alberta mortgage rate update. First-time buyers should start with our complete Edmonton guide, and if you’re weighing the rent-vs-buy math, our Edmonton rent vs buy analysis breaks down the real numbers. To understand the federal qualifying rules that apply to every fixed-rate application, see our mortgage stress test 2026 explainer.

About the author: Nathan Danzo is a mortgage broker at Metro Mortgage Group specializing in fixed-rate strategy, renewals, and rate comparisons across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: June 4, 2026