Mortgage Rate Holds in Canada Explained

120-day holds, when they expire, and how to use one strategically

Between March 2022 and July 2023, the Bank of Canada raised its policy rate ten consecutive times — from 0.25% to 5.00% — and borrowers without a rate hold watched their quoted mortgage rate climb mid-application (Bank of Canada, 2023). A rate hold would have frozen their quoted rate for up to 120 days, costing nothing and protecting thousands of dollars in monthly payments. If you’re buying, renewing, or refinancing in 2026, understanding how a mortgage rate hold works in Canada isn’t optional — it’s the cheapest insurance available.

Key Takeaways

– A mortgage rate hold guarantees your quoted fixed rate won’t increase for 90 to 120 days — and most lenders offer it free as part of a pre-approval (FCAC, 2025).

– If rates drop during your hold period, your lender or broker can typically renegotiate downward — you’re protected in both directions.

– Metro holds your rate with one lender at a time while continuously monitoring the broader market, so you’re not locked into a rate that a better option later beats.

– Rate holds apply to fixed-rate mortgages only — variable rates float with the Bank of Canada’s overnight rate and can’t be locked in advance.

What Exactly Is a Mortgage Rate Hold?

A mortgage rate hold is a lender’s written commitment to honour a specific fixed interest rate for a set number of days, regardless of what happens in the bond market between now and your closing date (FCAC, 2025). Think of it as a price guarantee on your interest rate. The hold starts the moment your pre-approval is issued and expires on a fixed calendar date, whether or not you’ve found a property yet.

The concept exists because Canadian fixed mortgage rates track the Government of Canada 5-year bond yield, which can shift meaningfully in a matter of weeks. Between January and April 2025, the 5-year bond yield swung roughly 60 basis points (Bank of Canada, 2025). Without a rate hold, a borrower who started shopping in January could’ve faced a noticeably higher rate by closing in March. With a hold, the rate was locked at the January level.

Rate holds are standard across every major Canadian lender — they aren’t a special product or a paid upgrade. They’re simply the mechanism that connects your pre-approval to a real, protected interest rate.

How Long Do Rate Holds Last in Canada?

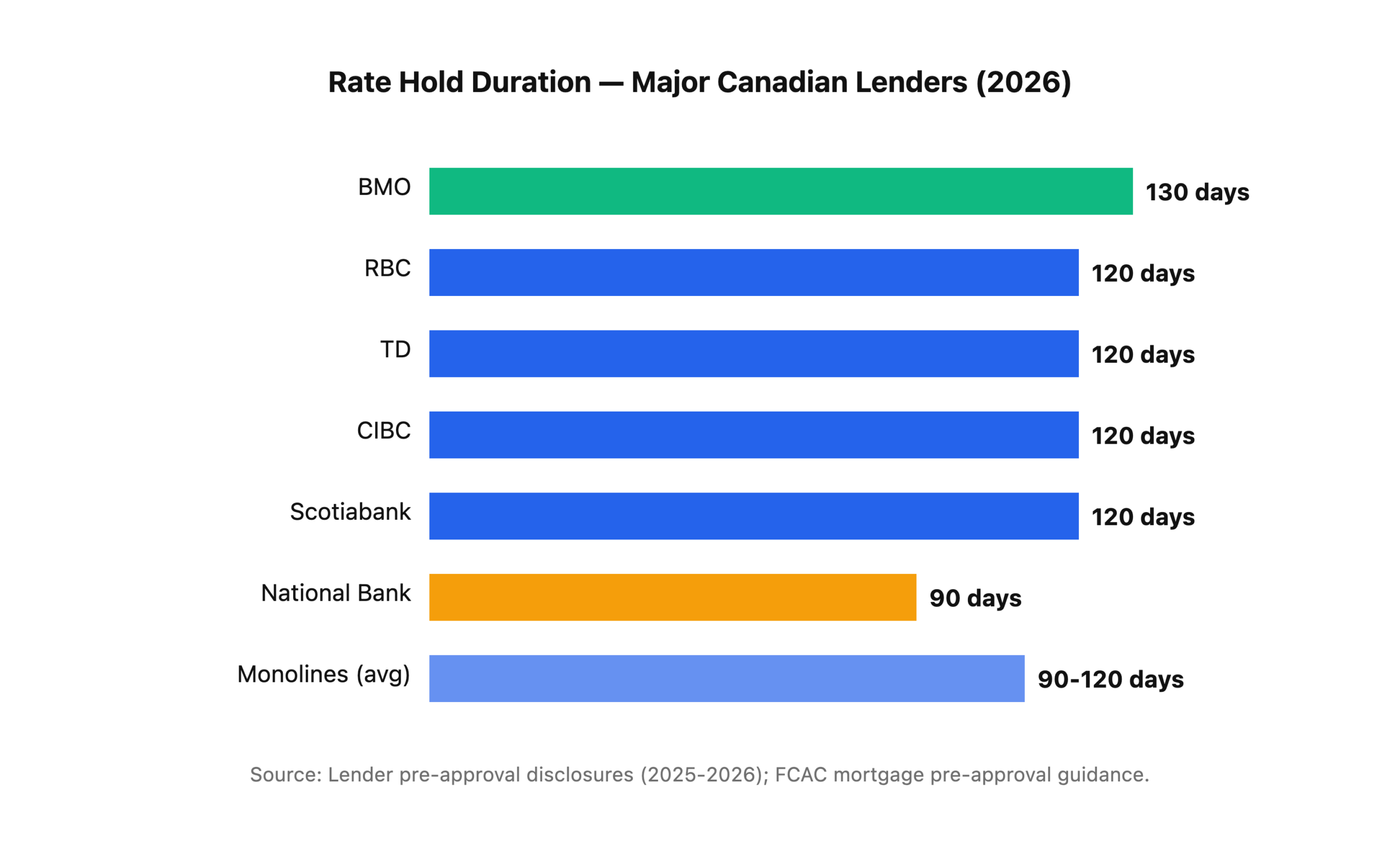

Most Canadian lenders offer rate holds between 90 and 120 days, though the exact duration varies by institution (FCAC, 2025). The Big Six banks and major monoline lenders have largely standardised around the 120-day window, giving purchasers roughly four months of rate protection from the date of pre-approval.

Here’s where the major lenders currently sit:

Exact hold periods are set by each lender and can change, so it’s worth confirming the current number with your broker at the time of application. In general, rate hold periods typically range from 60 to 180 days depending on the lender, with most major banks and monoline lenders clustering around the 90-to-120-day window described above.

The lesson? Start your pre-approval at least 120 days before your expected closing or renewal date to maximise your protection window. See how much mortgage you can afford before you begin.

Are Rate Holds Free?

Yes. Rate holds are free in Canada and come standard with any mortgage pre-approval (FCAC, 2025). There’s no application fee, no deposit, and no penalty for walking away. The lender runs a credit check during the pre-approval process, but the rate hold itself costs nothing. You’re not committed to that lender, and if a better rate turns up elsewhere before you close, your broker can move your hold to that lender instead.

That said, the rate you’re offered on a hold isn’t always the absolute lowest rate the lender has available. Some lenders build a small cushion into their held rate — a few basis points above their best “quick close” rate — as a hedge against market movement. A broker can tell you whether the held rate is truly competitive or whether a better deal exists at a different lender.

What Happens If Rates Drop During Your Hold?

Here’s the part most borrowers don’t realise: a rate hold protects you from increases, but it doesn’t trap you at a higher rate. If the bond market drops and fixed rates fall during your hold period, your lender will typically honour the lower rate when you finalise your application (Ratehub, 2025). You get a one-way protection — rates can’t go up on you, but they can come down.

This “float down” feature isn’t always automatic. Some lenders require you or your broker to formally request the lower rate before closing. Others adjust automatically. The distinction matters, because missing the window means staying at the original held rate even though a better one was available. Working with a broker who monitors rate sheets daily eliminates this risk entirely.

In practice, this means a rate hold is never a bad bet. You’re either protected from a rate increase or positioned to capture a rate decrease. There’s no scenario where having a hold makes you worse off than not having one.

How a Broker Manages Your Rate Hold

This is where the real strategy lives. A mortgage broker doesn’t just submit your application and disappear — they hold your rate with one lender at a time while continuously monitoring the broader market, and if a better option shows up before you close, they move you to it (Ratehub, 2025). It’s active management of your one hold, not a set-it-and-forget-it approach.

Here’s how a typical broker-managed rate hold works at Metro:

- Day 1: Submit your pre-approval and select the lender offering the best current fit for your situation

- Day 1-3: That lender issues a rate hold with their current best fixed rate

- Days 4-119: Your broker continues monitoring rate sheets across the market as the bond market moves — if a meaningfully better rate becomes available, they can move your hold to that lender

- Closing day: Confirm the held rate, factor in cashback offers, prepayment privileges, and penalty calculations, then fund with the best overall package available at that time

The advantage of working with a broker is that you’re not stuck with the first quote from the first lender you called. If a better rate becomes available before you close, your broker can act on it — something a borrower who went directly to a single bank isn’t positioned to do.

A single borrower going directly to their bank has no one tracking the broader market on their behalf once the hold is placed. A broker keeps watching after the hold is in place, so a rate improvement during your 120-day shopping window doesn’t get missed.

Real Savings: What a Rate Hold Is Actually Worth

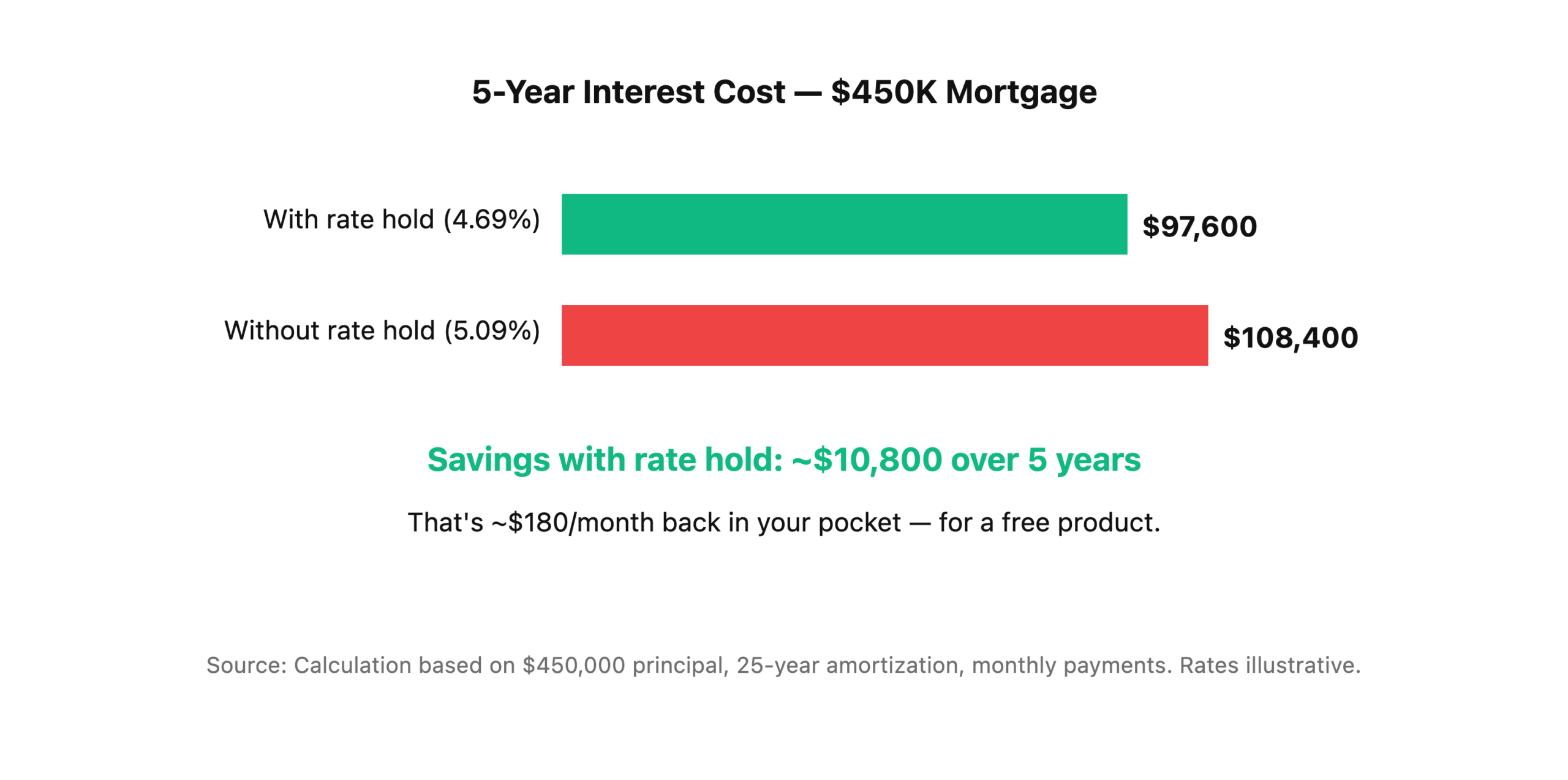

Let’s put real numbers on it. Suppose you’re buying a home in Edmonton with a $450,000 mortgage, 25-year amortization, 5-year fixed term. You secure a rate hold at 4.69% in mid-February. By your closing date in late May, the 5-year Government of Canada bond yield has climbed 40 basis points, pushing unprotected rates up to 5.09%.

The savings scale with the size of the mortgage. On a $700,000 mortgage — a higher-end detached home purchase in the Edmonton market — the same 40 bps rate swing represents roughly $14,000 in five-year interest savings. For a product that costs absolutely nothing, the risk-reward math is as lopsided as it gets. See our guide to down payment requirements in Alberta to plan your purchase amount.

Rate Holds vs. Rate Locks: Is There a Difference?

In Canadian mortgage language, the terms “rate hold” and “rate lock” are used interchangeably by most lenders and brokers, but some industry professionals draw a subtle distinction (Ratehub, 2025). A rate hold typically refers to the pre-approval stage — you’ve been conditionally approved and your rate is protected while you shop. A rate lock sometimes refers to the commitment stage — you’ve found a property, your full application is submitted, and the rate is formally locked for closing.

In practice, the protection is the same: the lender guarantees a rate for a defined period, and you’re shielded from increases. Whether your lender calls it a hold or a lock, the questions to ask are identical: How long does it last? Does it float down if rates drop? And what happens if I need an extension?

Don’t get caught up in terminology. Focus on the three things that matter: duration, float-down policy, and renewal options. Your pre-approval is where all three get locked in.

Can You Extend a Rate Hold?

Extensions are possible but not guaranteed. Most lenders will consider a 30 to 60 day extension if your original hold is expiring and you haven’t yet closed, but the extended rate may be adjusted to reflect current market conditions (Ratehub, 2025). If rates have risen since your original hold, the extension might come at the new, higher rate — which defeats the purpose.

The better strategy is to time your pre-approval correctly from the start. If you’re planning to close in September, begin the pre-approval process in May or early June so your 120-day window covers the closing date with room to spare. If you start too early and the hold expires, you’ll need a fresh pre-approval at whatever rate is available that day.

A broker adds value here because they’re tracking your hold expiry date and continuously watching the broader market, so they can proactively renew your hold or move you to a better lender before the original hold lapses. It’s one of those administrative details that sounds minor but can cost thousands if it slips. Budget for closing costs in Alberta while your hold is active so there are no surprises at funding.

When Should You Get a Rate Hold?

The short answer: as early as possible. There’s no downside to getting a pre-approval with a rate hold even if you’re months away from buying. The hold costs nothing, doesn’t commit you to anything, and protects you from the single biggest variable in Canadian mortgage pricing — interest rate movement.

Specific timing triggers where a rate hold becomes urgent:

- You’re 90-120 days from a purchase closing — this is the sweet spot for maximum protection

- Your renewal is coming up in 4-6 months — lock a hold now and shop for a better rate as the renewal date approaches

- The Bank of Canada just paused or signalled a policy shift — rate volatility tends to spike around BOC announcements, making holds more valuable

- Bond yields are trending upward — the 5-year GOC bond directly drives fixed rates, and a rising trend means today’s rate could be tomorrow’s bargain

For renewals specifically, most lenders send renewal offers 120 to 180 days before maturity. Don’t sign the first offer. Get a broker to secure a rate hold with a competitive lender and use it to negotiate from a position of strength. The renewal offer from your existing lender is almost never the best rate available. Learn more about mortgage renewals in Alberta.

What a Rate Hold Doesn’t Cover

A rate hold protects your interest rate, but it doesn’t guarantee final mortgage approval. The hold is conditional — the lender still needs to underwrite the specific property, verify your income and employment at closing, confirm the appraisal, and complete their standard due diligence (FCAC, 2025). If your financial situation changes between the pre-approval and closing — a job loss, a large new debt, a credit score drop — the lender can withdraw the approval even though the rate is held.

Rate holds also don’t apply to variable-rate mortgages in most cases. Because variable rates are tied to the lender’s prime rate, which moves with the Bank of Canada’s overnight target, they can’t be meaningfully locked in advance. If you’re leaning toward variable, the rate hold conversation is less relevant — your rate will adjust on the next BOC announcement regardless.

Finally, rate holds don’t cover mortgage default insurance premiums (CMHC, Sagen, or Canada Guaranty). The insurance premium is calculated based on your LTV at closing and added to your mortgage balance or paid upfront. It’s a separate cost from the interest rate.

Frequently Asked Questions

Can I switch lenders after my rate hold is in place?

Yes. Your rate hold is placed with one lender at a time, but you’re not locked out of the rest of the market. If your broker spots a better rate at another lender before you close, they can move your pre-approval and start a fresh hold there instead (Ratehub, 2025). The practical consideration is that each new pre-approval generates a credit inquiry, though multiple mortgage inquiries within a 14-day window are typically treated as a single inquiry by credit bureaus.

Do rate holds work for mortgage renewals, not just purchases?

Yes. You can secure a rate hold 120+ days before your renewal date and use it as leverage against your current lender’s renewal offer. Brokers regularly place renewal rate holds to ensure their clients get the best available rate at maturity, not just the default offer from the existing lender. See our full renewal guide for the details.

Can I get a rate hold on a refinance?

Absolutely. Refinance rate holds work identically to purchase holds — the lender guarantees a rate for 90-120 days while your refinance application is processed. Since refinances typically take 30 to 45 days from application to funding, the hold window provides comfortable coverage.

What’s the longest rate hold available in Canada?

Hold periods vary by lender and can run anywhere from 60 to 180 days, with some institutions occasionally offering longer windows in select cases. Most major lenders sit around 120 days, which is the de facto industry standard in 2026 — but it’s worth confirming the current figure directly with your broker, since terms can change.

Does getting a rate hold affect my credit score?

The rate hold itself doesn’t affect your score, but the pre-approval process includes a hard credit inquiry, which may temporarily lower your score by a few points (Equifax, 2025). Multiple mortgage inquiries within a short window (typically 14-45 days) are grouped as a single inquiry by credit bureaus, so switching your hold to a different lender within that window doesn’t multiply the credit impact.

Ready to Lock In Your Rate Before It Moves?

Rate holds cost nothing, protect everything, and work in your favour whether rates go up or down. Metro Mortgage Group has access to 30+ lenders and holds your rate with the one that’s the best fit at the time of your pre-approval — purchase, renewal, or refinance — while continuously monitoring the broader market for a better option before you close. Call 780-974-1270 or email info@MetroMortgageGroup.ca to start your pre-approval and lock in today’s rate for up to 120 days.

Already have a pre-approval from your bank? Bring it in — we’ll tell you if there’s a better hold available. Check our rates guide to see where fixed and variable rates sit right now, or start with our mortgage affordability calculator.

About the author: Nelson Sousa is co-owner of Metro Mortgage Group with 9+ years of experience in construction and roughly 16 years in mortgage financing across Alberta. Metro Mortgage Group has served Edmonton and Calgary homebuyers since 2011 with 229 five-star Google reviews.

Last updated: April 30, 2026