Prepayment Privileges Compared

Lump-sum, double-up, and increase-payment options across Canadian lenders

More than two million Canadian mortgages are set to renew between 2025 and 2026, with roughly 85% originally taken out when the Bank of Canada’s policy rate was at or below 1% (Bank of Canada Financial Stability Report). For those homeowners, every dollar of principal paid down before renewal is a dollar that won’t be subject to a potentially higher rate. That makes prepayment privileges — the amount you can pay above your regular payment without penalty — one of the most valuable, and most overlooked, features of any mortgage contract.

Yet most Canadians don’t even know what their prepayment privileges are, let alone compare them across lenders. Let’s fix that.

Key Takeaways

– Prepayment privileges let you make lump sum payments (typically 10-20% of original principal per year) and increase regular payments (typically 10-100%) without penalty (FCAC).

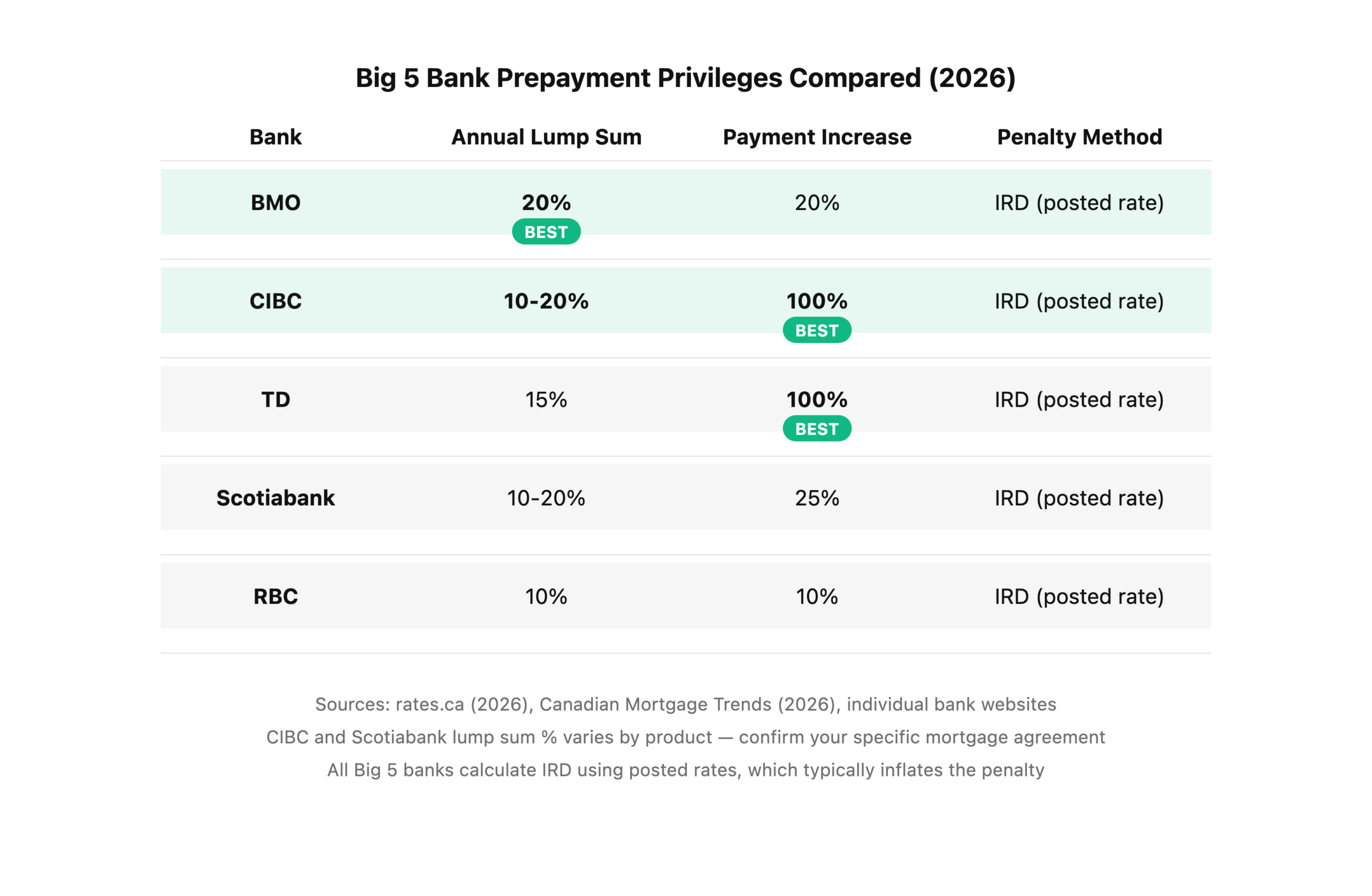

– Among the Big 5 banks, BMO and CIBC offer the most generous lump sum privileges at 20%, while RBC offers the lowest at 10% (rates.ca, 2026).

– Monoline lenders like First National typically offer 15% lump sum with fair penalty calculations that can save thousands if you break your mortgage (Canadian Mortgage Trends).

– A mortgage broker can negotiate custom prepayment terms — something you can’t do walking into a bank branch.

– On a $500,000 mortgage, the difference between 10% and 20% annual lump sum privileges is $50,000 per year in additional payment room.

What Are Prepayment Privileges, Exactly?

Prepayment privileges are contractual rights that let you pay down your mortgage faster without triggering a penalty. The Financial Consumer Agency of Canada (FCAC) requires lenders to disclose prepayment privileges in every mortgage contract (FCAC, 2026). There are two types:

Lump sum privileges let you make one-time payments — usually expressed as a percentage of your original principal amount — directly against your mortgage balance each year. If you have a 15% lump sum privilege on a $400,000 mortgage, you can put up to $60,000 against the principal in a calendar year without penalty.

Payment increase privileges let you raise your regular mortgage payment by a set percentage above the original amount. If you have a 25% payment increase privilege on a $2,200/month payment, you can increase it to $2,750/month without penalty.

Both types apply the extra money directly to principal, which reduces your amortization period and saves you interest over the life of the mortgage. So why don’t more people use them?

See our mortgage affordability guide for the basics.

Big 5 Bank Prepayment Privileges: Head-to-Head Comparison

The Big 5 banks vary significantly on prepayment generosity, and the differences add up fast on a large mortgage. Here’s how they stack up in 2026:

The headline numbers tell only part of the story. BMO offers a generous 20% annual lump sum, but their IRD penalty calculation uses posted rates — which means if you break your fixed-rate mortgage early, the penalty can be dramatically higher than the same calculation at a monoline lender. TD’s 100% payment increase privilege is outstanding, but their lump sum is only 15%. RBC is the least generous across the board at 10/10.

What does this mean in real dollars? On a $500,000 mortgage, the difference between RBC’s 10% lump sum ($50,000/year) and BMO’s 20% ($100,000/year) is $50,000 in additional annual payment room. If you receive a bonus, inheritance, or windfall, that flexibility matters enormously.

Citation Capsule: “Most lenders set annual limits on lump-sum payments ranging from 10% to 20% of the original principal each year. Exceeding your prepayment privilege triggers a penalty — typically three months’ interest on variable-rate mortgages or the interest rate differential on fixed-rate mortgages.” — rates.ca mortgage prepayment guide

Credit Unions: Alberta’s Flexible Alternative

Alberta credit unions often match or beat the Big 5 on prepayment flexibility, and they’re more willing to negotiate custom terms for strong borrowers. Servus Credit Union is the largest credit union in Alberta and serves the Edmonton and Calgary markets; Servus merged with Connect First Credit Union in 2024, bringing the combined institution’s membership together under one roof. ATB Financial is also a major Alberta-based lender worth comparing — it’s a Crown corporation owned by the Government of Alberta, not a credit union, but it offers many of the same member-focused pricing advantages.

Credit unions have two structural advantages when it comes to prepayment privileges. First, they’re member-owned, which means they’re not under the same shareholder pressure to maximise penalty revenue. Second, many Alberta credit unions calculate their IRD penalties using the contract rate minus the current comparable rate — not the posted rate. That single difference can reduce a break penalty by 50% or more compared to a Big 5 bank using posted rates.

The trade-off? Credit unions may offer slightly higher mortgage rates than the most aggressive monoline lenders, and their geographic reach is limited to Alberta (or whichever province they’re chartered in). If you’re staying in Alberta — and you’re reading a guide about Alberta lenders, so you probably are — that limitation doesn’t matter.

Are you paying attention to the penalty formula, or just the rate?

Monoline Lenders: The Fair Penalty Advantage

Monoline lenders like First National, MCAP, and THINK Financial have built their reputation on two things: competitive rates and fair prepayment penalties (Canadian Mortgage Trends, 2026). They’re broker-only, meaning you can’t walk into a branch — you access them through a mortgage broker like Metro.

Here’s where monolines shine:

First National offers 15% annual lump sum prepayment and 15% payment increase on fixed-rate terms (Canadian Mortgage Trends, 2026). Their IRD penalty calculation uses the actual contract rate minus the current rate for the remaining term — not the inflated posted rate that banks use. On a typical five-year fixed mortgage broken at Year 3, this contract-rate approach can mean a break penalty that’s a fraction of what the identical mortgage would cost to break at a Big 5 bank using the posted-rate method — often a difference of many thousands of dollars, though the exact gap depends on your rate, balance, and how much term is remaining.

THINK Financial (a subsidiary of True North Mortgage) is specifically marketed as a “fair penalty lender” (RateSpy, 2026). Their penalty calculation methodology is transparent, and they’ve built their brand around it. If there’s any chance you’ll break your mortgage before the term is up — job relocation, divorce, rate improvement opportunity — a fair penalty lender should be on your shortlist.

MCAP offers competitive prepayment terms through the broker channel with flexible amortization and straightforward penalty calculations.

Citation Capsule: “Monoline lenders typically offer better rates, prepayment privileges, and reduced penalties compared to traditional banks. Their IRD calculations use actual contract rates rather than inflated posted rates, which can cut a break penalty by 50% or more.” — REMIC monoline lender guide

B-Lenders and Private: Less Flexibility, Higher Risk

B-lenders and private lenders serve borrowers who don’t qualify at A-lenders or monolines — typically due to credit issues, irregular income, or unconventional properties. Their prepayment privileges are usually more restrictive, and their penalties are higher.

Most B-lenders offer a standard three months’ interest penalty on both fixed and variable products, with lump sum privileges of 10-15%. Private lenders (MICs and individual private lenders) often include lock-out periods of 6-12 months during which no prepayment is allowed at any price, followed by three months’ interest penalties.

The math here is straightforward: if you’re with a B-lender or private lender paying 7-10% interest, three months’ interest on a $400,000 mortgage is $7,000-$10,000. That’s a meaningful cost. The goal with any B-lender or private mortgage should be to improve your credit profile and refinance into an A-lender or monoline as quickly as possible — and when you do, you’ll want maximum prepayment privileges on your new mortgage to accelerate paydown. Our credit score guide covers what it takes to qualify for better terms.

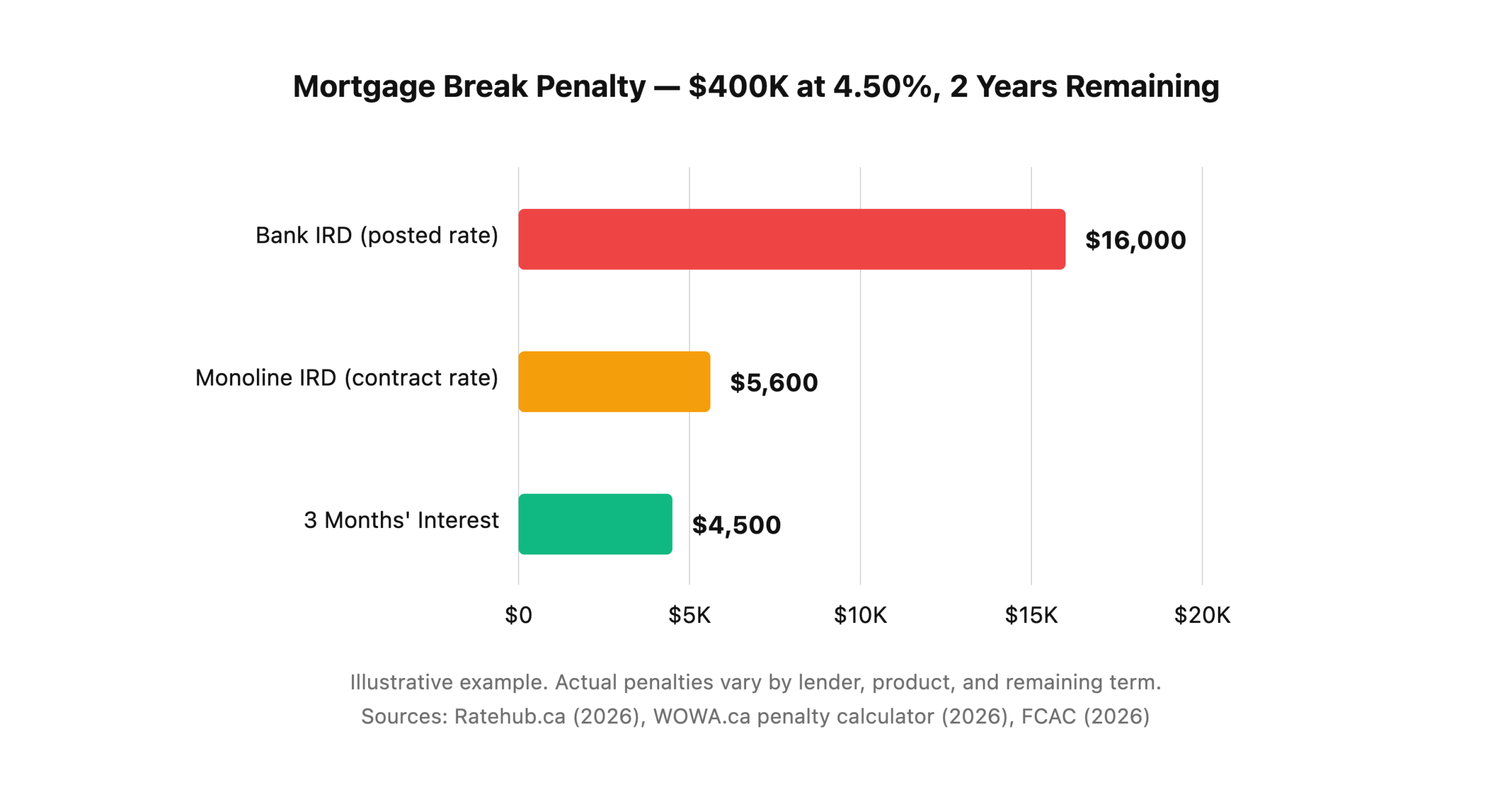

IRD vs. Three Months’ Interest: Why the Penalty Formula Matters More Than the Rate

The interest rate differential (IRD) penalty is where the Big 5 banks make billions of dollars per year from homeowners who break their mortgages early. Understanding how it works — and how it differs from the simpler three months’ interest penalty — is essential for anyone comparing prepayment terms.

Three Months’ Interest

The simpler formula: outstanding balance × annual rate × 3/12. On a $400,000 balance at 5.00%, that’s $400,000 × 0.05 × 0.25 = $5,000. Predictable, straightforward, and always the penalty on variable-rate mortgages.

Interest Rate Differential (IRD)

The more complex formula: outstanding balance × (contract rate – comparison rate) × remaining term in years. Banks use their posted rate as the comparison rate, which is typically 1.5-2.5% above the rate they actually gave you. This inflates the differential and therefore inflates the penalty.

Here’s a real example. You have a $400,000 fixed-rate mortgage at 4.50% with 2 years remaining:

- Bank IRD (posted rate method): $400,000 × (4.50% – 2.50% posted 2-year rate) × 2 years = $16,000

- Monoline IRD (contract rate method): $400,000 × (4.50% – 3.80% actual 2-year rate) × 2 years = $5,600

- Three months’ interest: $400,000 × 4.50% × 3/12 = $4,500

Same mortgage. Same borrower. The penalty ranges from $4,500 to $16,000 depending on the lender. That’s why the penalty formula matters more than a 0.05% rate difference.

Citation Capsule: “To calculate your mortgage prepayment charge, your lender will use the greater of three months’ interest or the interest rate differential (IRD). The IRD is based on the difference between your existing mortgage interest rate and the interest rate the lender can charge today when re-lending the funds for the remaining term.” — FCAC mortgage penalty guide

How a Mortgage Broker Negotiates Better Prepayment Terms

Most Canadians don’t realize prepayment privileges are negotiable — especially through the broker channel. Banks set standard prepayment terms for walk-in customers, but brokers have access to rate exceptions and product variations that aren’t on the public rate sheet.

Here’s what we can do at Metro Mortgage Group that you can’t do at a bank branch:

Access monoline and broker-only lenders. First National, MCAP, RMG, THINK Financial — these lenders don’t have branches. They’re only available through a mortgage broker. They consistently offer better prepayment terms and fairer penalty calculations than the Big 5.

Compare apples to apples across 30+ lenders. When we present mortgage options to a client, we include the prepayment privilege details side by side — lump sum percentage, payment increase cap, and penalty calculation method. The “lowest rate” option and the “best prepayment terms” option aren’t always the same lender. We help you decide which combination fits your situation.

Negotiate custom terms for strong files. On large mortgages or borrowers with exceptional credit profiles, some lenders will offer enhanced prepayment privileges — bumping from 15% to 20% lump sum, or from 15% to 25% payment increase. A bank branch employee can’t make that call. A broker with volume relationships can.

Match you to the right penalty structure. If you’re buying your forever home and you’re confident you’ll stay the full term, penalty structure barely matters — take the lowest rate. If there’s any chance you’ll move, refinance, or pay a lump sum larger than your privilege allows, the penalty formula is worth more than a 0.10% rate discount.

Real Cost Scenario: Using Prepayment Privileges to Beat Renewal Shock

Here’s a scenario we see regularly at Metro as the 2025-2026 renewal wave hits:

The situation: An Alberta homeowner has a $450,000 mortgage at 1.89% fixed, taken in 2021. The five-year term renews in late 2026. Current five-year fixed rates are approximately 4.50%. Without any principal paydown beyond regular payments, they’ll owe roughly $395,000 at renewal. Monthly payment at 4.50% on a 20-year amortization: approximately $2,500.

With aggressive prepayment use: Their mortgage has a 20% lump sum privilege. Over the final two years before renewal, they make two lump sum payments of $45,000 each (within the 20% annual limit on the original $450,000 balance), plus they increase their regular payment by 15%. By renewal, they owe approximately $290,000. Monthly payment at 4.50% on a 20-year amortization: approximately $1,835.

The difference: $665/month — or roughly $8,000 per year — for the entire next five-year term. Over five years, that’s $40,000 in savings, simply by using prepayment privileges that were already in their contract.

Not everyone has $90,000 in lump sums available. But even smaller amounts — a tax refund, a bonus, an inheritance — compound when applied as a lump sum. A $10,000 lump sum on a $400,000 mortgage at 4.50% saves roughly $14,800 in interest over a 25-year amortization. The mortgage you don’t pay interest on is the cheapest money you’ll ever save.

If your renewal is coming up, see our renewal planning guide and our down payment guide for how the math works.

Frequently Asked Questions About Prepayment Privileges

Can I make multiple lump sum payments per year?

It depends on your lender. Most Big 5 banks allow lump sum payments at any time during the year, as long as the total doesn’t exceed your annual privilege percentage. Some lenders restrict lump sums to specific dates (e.g., your anniversary date). Your mortgage agreement specifies the exact terms. At Metro, we review this with every client before they sign — not after.

Do prepayment privileges reset each year?

Yes. Most lenders reset your lump sum privilege annually — either on January 1 (calendar year) or on your mortgage anniversary date. If you don’t use your privilege in a given year, it does not carry forward to the next year. Use it or lose it.

What happens if I exceed my prepayment privilege?

You’ll pay a penalty on the amount that exceeds your privilege. On a variable-rate mortgage, that’s typically three months’ interest on the excess amount. On a fixed-rate mortgage, it’s the greater of three months’ interest or the IRD — and the IRD can be substantial (FCAC). Always check your remaining privilege before making a lump sum payment.

Are prepayment privileges different for variable vs. fixed mortgages?

The lump sum and payment increase percentages are usually the same. The key difference is the penalty for exceeding them. Variable-rate mortgages always use the three months’ interest penalty (the cheaper option). Fixed-rate mortgages use the greater of three months’ interest or IRD (which can be the expensive option). This is one reason some borrowers choose variable specifically for the penalty flexibility.

Can I negotiate better prepayment privileges at renewal?

Absolutely. Renewal is the best time to renegotiate every term of your mortgage — rate, amortization, and prepayment privileges. Your existing lender’s renewal offer is a starting point, not a final answer. Bring it to Metro and we’ll show you what’s available across 30+ lenders. You might keep the same lender at better terms, or you might move entirely. Either way, you’ll know you got the best deal available. See our renewal guide for more on timing it right.

Don’t Leave Money on the Table

Prepayment privileges are a free option embedded in your mortgage contract — you never pay extra to have them, you only lose by not using them. With the 2025-2026 renewal wave in full swing and rates sitting well above the pandemic-era lows, every dollar of extra principal you can pay down now reduces your interest burden for decades to come.

If you’re not sure what your current prepayment privileges are, or you want to compare your existing mortgage terms against what’s available in today’s market, call Metro Mortgage Group at 780-974-1270 or email info@MetroMortgageGroup.ca. We’ll review your mortgage agreement, show you the math on lump sum savings, and — if refinancing makes sense — find the lender with the best combination of rate and prepayment flexibility.

You don’t pay for our service. The lender does. That’s how the broker model works.

Contact us to get started, or see all our mortgage services.

About the Author

Miguel Cunha is a mortgage broker at Metro Mortgage Group Inc. in Edmonton, Alberta. He helps first-time buyers, renewals, and refinance clients across Edmonton and Calgary navigate the mortgage market with access to 30+ lenders. Metro Mortgage Group: 5.0 stars from 229 Google reviews.

Last updated: June 25, 2026