First Place Program Edmonton

How Edmonton’s down-payment-deferral program works for first-time buyers

If you’re searching for the City of Edmonton First Place Program in 2026, here’s the honest answer: the program was phenomenal while it ran, deferring roughly $70,000-$90,000 of land cost interest-free for 5 years on 243 townhouses built on surplus school sites (City of Edmonton, 2023). The last units sold in 2022, and no new intake has been announced. But the program’s math still teaches you exactly how to stack the replacement tools available to Edmonton first-time buyers in 2026.

Key Takeaways

– The First Place Program deferred 100% of the land cost — roughly 15-20% of total purchase price — for 5 years interest-free, making it one of Canada’s most generous municipal housing programs (City of Edmonton, 2023).

– Over 10 years, the City built 243 townhouses across 6 Edmonton neighbourhoods and sold every single one — waiting lists ran 200+ deep for the final releases.

– The program is currently inactive as of 2026, with no new builds announced. Existing First Place owners still face the land-cost repayment at year 5.

– The modern replacement stack — FHSA + RRSP HBP + 5% down — can deliver comparable entry-cost savings for motivated buyers in 2026.

What Is the Edmonton First Place Program and How Did It Work?

The Edmonton First Place Program was a municipal initiative that sold 243 townhouses on surplus school sites to first-time buyers between 2006 and 2022, deferring the entire land cost interest-free for 5 years (City of Edmonton, 2023). Buyers paid only for the building portion upfront and took title to land and building together, with a caveat registered on title for the deferred amount.

Here’s the mechanic in plain English. A First Place townhouse might list at $320,000 total. The City split that into roughly $265,000 for the building (which you financed immediately like any normal mortgage) and $55,000-$70,000 for the land (which the City parked as an interest-free loan sitting on title). At year 5, the land portion came due — you either refinanced to absorb it into your mortgage or paid it out.

Where Were the First Place Developments?

The City built First Place townhouses on former school sites in six Edmonton neighbourhoods: Ritchie, Belvedere, Newton, Ottewell, Crestwood, and Britannia Youngstown. Every site followed the same playbook — surplus Edmonton Public or Catholic school land, low-rise townhouse format, 20-40 units per development, priced intentionally below market.

Who Was Eligible?

Eligibility locked the program tightly to genuine first-time buyers. Applicants needed to be Canadian citizens or permanent residents, first-time homeowners (nobody on title had owned a home in Canada in the prior 5 years), and had to occupy the unit as their principal residence. Household income caps sat around $117,500 for the final intakes, and buyers had to qualify for a conventional mortgage on the building-only portion.

How Much Did First Place Actually Save Edmonton Buyers?

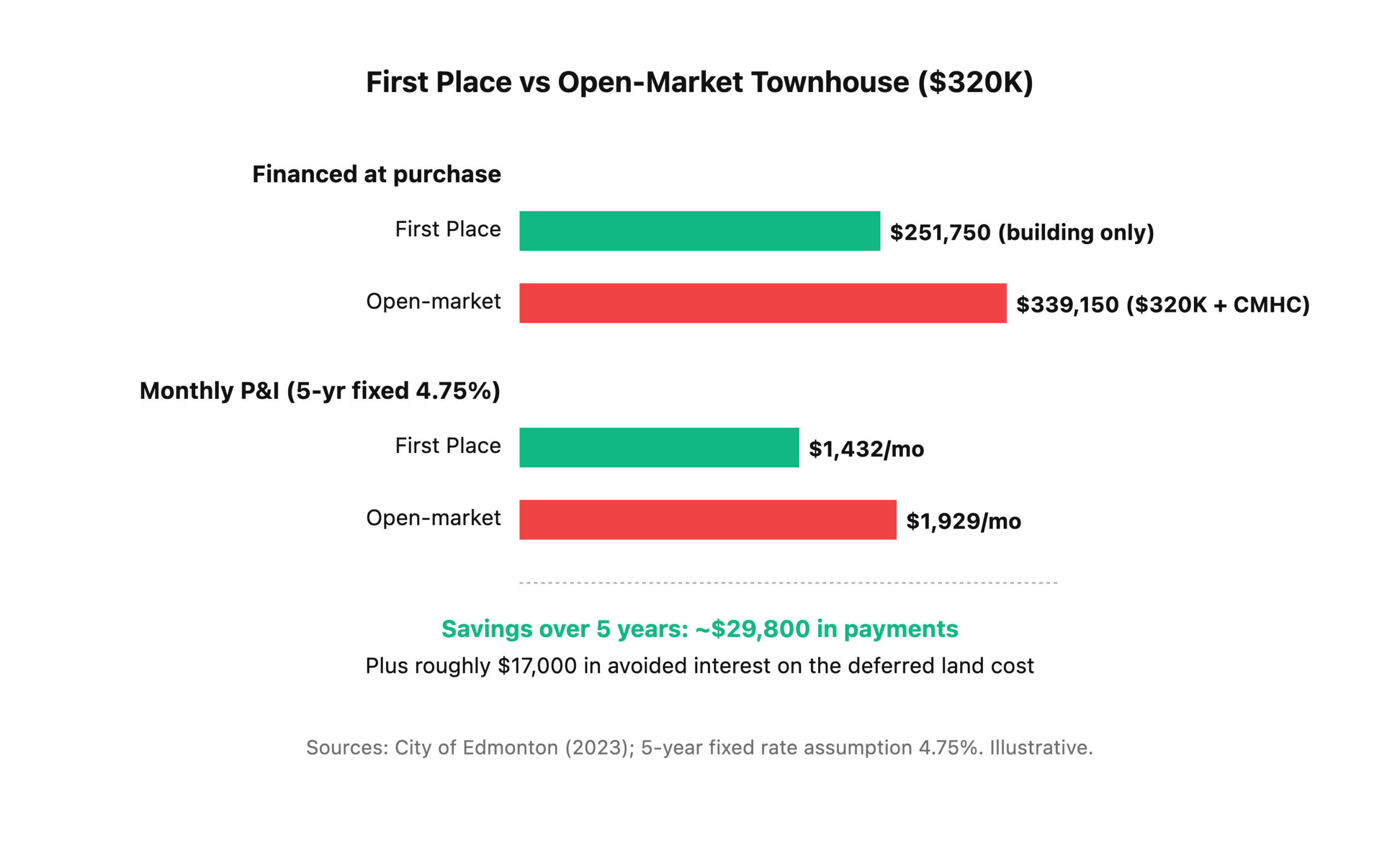

On a typical $320,000 First Place townhouse, the program deferred roughly $55,000-$70,000 in land cost — about 17-22% of the purchase price — for 5 years at 0% interest, saving buyers $12,000-$18,000 in interest charges alone over the deferral window (City of Edmonton, 2023). The real entry-cost impact was bigger than the interest savings suggest.

Run that math from a cash-flow perspective. A First Place buyer carried roughly $500/month less in mortgage payment for the first 5 years compared to the same townhouse bought on the open market, freeing up cash for emergency fund, FHSA contributions, or simple breathing room. At year 5 the land cost came due, and most owners absorbed it by refinancing into a new mortgage term.

What Was the Catch With the First Place Program?

The First Place Program had three real catches — and they mattered enough that a handful of buyers regretted their purchase even with the massive upfront savings (City of Edmonton, 2023). I watched the year-5 refinance season firsthand in 2018-2022 and the story wasn’t always pretty.

The most honest version of the catch is this: in year 5, the deferred land cost doesn’t disappear, it becomes your problem. Imagine a Belvedere couple navigating their First Place refinance in 2021 — they’d bought in 2016 for $285,000 with roughly $58,000 of land cost deferred. When year 5 hits, their mortgage balance has paid down to about $200,000, but they need to roll in the $58,000 land payout, pushing the new mortgage to $258,000. Rates have moved, their renewal payment jumps $340/month, and they briefly consider selling. They don’t. They stay in the unit and the math still works — but the year-5 shock is real.

Catch 1: The Balloon Land Payment at Year 5

The deferred land cost is not forgiven — it becomes a lump sum due at the end of year 5. Most owners refinanced to absorb it, which meant taking on a higher mortgage principal right as the original 5-year term came up for renewal. If interest rates moved against you between purchase and year 5, the payment shock could be severe.

Catch 2: Location Constraints

First Place buyers didn’t get to pick their neighbourhood. Units were built where the City had surplus school land — not always where buyers wanted to live. Some of the sites (Britannia Youngstown, Newton, Belvedere) were excellent mature neighbourhoods with strong schools and transit. Others sat further from downtown with weaker resale demand.

Catch 3: Limited Inventory and Long Waiting Lists

Total program production was 243 units over 16 years, roughly 15 units per year on average. Demand always outstripped supply. Final releases had waiting lists of 200+ qualified first-time buyers competing for 20-40 units per site. Most Edmontonians who applied never got a unit.

Is the First Place Program Still Running in 2026?

No — the City of Edmonton First Place Program is currently inactive, with the final units sold in 2022 and no new development sites announced as of 2026 (City of Edmonton, 2023). The City has shifted its affordable housing focus toward partnership projects with Homes for Heroes, Civida, and community housing providers rather than direct-to-buyer surplus school site sales.

Here’s what most “is First Place still running” articles miss: the program ended because it worked too well for a narrow window of buyers and became politically difficult to scale. Every surplus school site the City released sparked years of rezoning fights with surrounding neighbourhoods. The administrative burden of qualifying 200+ applicants per site, managing the 5-year deferred land caveats, and handling year-5 refinance disputes eventually outweighed the political wins. The program didn’t fail — it just stopped being the right tool.

What About Existing First Place Owners?

If you already own a First Place townhouse and you’re approaching year 5, the deferral still works exactly as signed. The City honours every existing caveat. Your options at year 5 remain: refinance to absorb the land cost, pay it out in cash, or sell the unit and let the transaction clear the caveat. Talk to a mortgage broker at least 6 months before your year-5 date so you have room to lock a rate.

What Should Edmonton First-Time Buyers Do Instead in 2026?

The replacement for First Place isn’t a single program — it’s a stack of three federal tools that, layered correctly, can match or exceed the original program’s entry-cost savings for most Edmonton first-time buyers (Canada Revenue Agency, 2026). Here’s the honest broker version.

The FHSA + HBP + 5% Down Stack

- First Home Savings Account (FHSA) — up to $8,000/year, $40,000 lifetime, fully tax-deductible going in and fully tax-free coming out. A couple can stack $80,000 combined. Full breakdown in our FHSA Alberta guide.

- RRSP Home Buyers’ Plan (HBP) — withdraw up to $60,000 per person ($120,000 per couple) from existing RRSPs tax-free for your down payment, repayable over 15 years. See our RRSP HBP Alberta guide.

- 5% minimum insured down payment — Alberta has no land transfer tax, so 5% down gets you in the door faster than any other province. See exactly how much down payment you need in Alberta.

Stack those three tools on a $420,000 Edmonton starter townhouse and a motivated dual-income couple can enter ownership with roughly $21,000 of their own money, a $60,000+ HBP/FHSA supercharge, and a manageable insured mortgage. That’s not First Place — but it’s the closest modern equivalent, and it’s available to everyone, not 15 lucky lottery winners per year.

Alberta-Specific Helpers Still Available

Alberta also offers the federal First-Time Home Buyers’ Tax Credit of up to $1,500 in the tax year you buy, and you’ll benefit from Alberta’s zero land transfer tax at closing. Combined with low Alberta closing costs, your total cash-to-close is among the lowest in Canada.

Who Was First Place Actually Worth It For?

First Place was a home run for one specific buyer profile: dual-income first-time buyers in the $60,000-$100,000 household income range who were flexible on neighbourhood, planned to hold for at least 7-10 years, and had a stable enough career trajectory to handle the year-5 refinance (City of Edmonton, 2023). For that buyer, the program was the best municipal housing deal in Canada.

It wasn’t worth it for three types of buyers. Single buyers stretching their budget got hit hardest by year-5 refinance shock because they had no income diversification if rates moved. Buyers planning to move within 5 years couldn’t realize the full savings, because selling before the deferral matured just triggered the land-cost payout early. And buyers who needed a specific neighbourhood (school catchment, proximity to aging parents, commute to a specific workplace) often found the available First Place sites didn’t match their actual life.

Frequently Asked Questions

Is the First Place Program accepting applications in 2026?

No. The City of Edmonton First Place Program sold its final units in 2022, and no new development sites have been announced as of 2026 (City of Edmonton, 2023). Edmonton’s current affordable housing strategy routes through partnerships with Civida, community housing providers, and rent-to-own pilots rather than direct-to-buyer surplus school site sales.

How much did the First Place Program actually defer?

The program deferred 100% of the land cost — typically 15-22% of total purchase price — for 5 years interest-free, which translated to roughly $55,000-$90,000 on most First Place townhouses depending on site and year of purchase (City of Edmonton, 2023). Avoided interest over the 5-year deferral window added another $12,000-$18,000 of effective savings.

What happens to First Place owners at year 5?

At year 5, the deferred land cost becomes due as a lump sum. Most owners refinance their mortgage to absorb the land payout into a new principal balance (CMHC, 2025). Others pay it from savings, and a small number sell the unit and clear the caveat through the sale. Start planning the refinance 6 months before your year-5 date.

Can I still buy a resale First Place townhouse?

Yes. When an original First Place owner sells, the unit transacts like any normal Edmonton townhouse — the deferred land cost gets paid out of the sale proceeds and the caveat is cleared at closing. Resale First Place units occasionally appear on the open market through the REALTORS Association of Edmonton MLS and trade at standard market prices.

What’s the best modern alternative for Edmonton first-time buyers?

The strongest 2026 replacement is the FHSA + RRSP HBP + 5% down stack, which can deliver $100,000+ of combined tax-advantaged down payment capital for a dual-income couple (Canada Revenue Agency, 2026). It’s not a subsidized townhouse, but it’s available to everyone who qualifies and it isn’t limited to 15 units per year.

Ready to Build Your First-Time Buyer Strategy Without First Place?

First Place isn’t coming back in 2026, but the underlying goal — getting Edmonton first-time buyers into ownership with the least cash out of pocket — is still absolutely achievable. Metro’s first-time buyer team runs full FHSA + HBP + down payment scenarios for Edmonton clients every week, free of charge. We’ll map your exact cash-to-close, show you the 12-month savings plan, and pre-approve you before you start shopping. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full first-time buyer playbook, start with our complete Edmonton first-time home buyer guide. To make sure your credit is ready before you apply, read our guide on credit score requirements for Alberta mortgages.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and specializes in first-time home buyer financing across Alberta. Metro Mortgage Group has served Edmonton, Calgary, and greater Alberta since 2011 with 229 five-star Google reviews.

Last updated: May 1, 2026