How Much Mortgage Can I Afford in Edmonton?

Stress test math, GDS/TDS ratios, and Edmonton-specific affordability examples

A median Edmonton household earning $108,000 in 2026 can typically qualify for a mortgage of $470,000 to $505,000 — enough to purchase Edmonton’s $470,819 average home with 5-10% down (Statistics Canada, 2024; REALTORS Association of Edmonton, 2026). That’s not a hypothetical. It’s what Metro Mortgage Group sees on actual pre-approvals every week. The real question isn’t whether you can qualify in Edmonton — it’s how much of that maximum you should actually borrow.

Key Takeaways

– Median Edmonton household income of ~$108,000 qualifies for roughly $470K-$505K at 2026 rates (Statistics Canada, 2024).

– Canadian lenders cap housing costs at 39% GDS and total debt at 44% TDS under CMHC and mortgage insurer qualifying guidelines (CMHC, 2025).

– The mortgage stress test qualifies you at contract rate +2% or the 5.25% floor, whichever is higher.

– Edmonton buyers can afford 2.4x more home than Torontonians on the same paycheque — the single biggest affordability advantage in Canada.

How Much Mortgage Can I Afford on an Edmonton Salary in 2026?

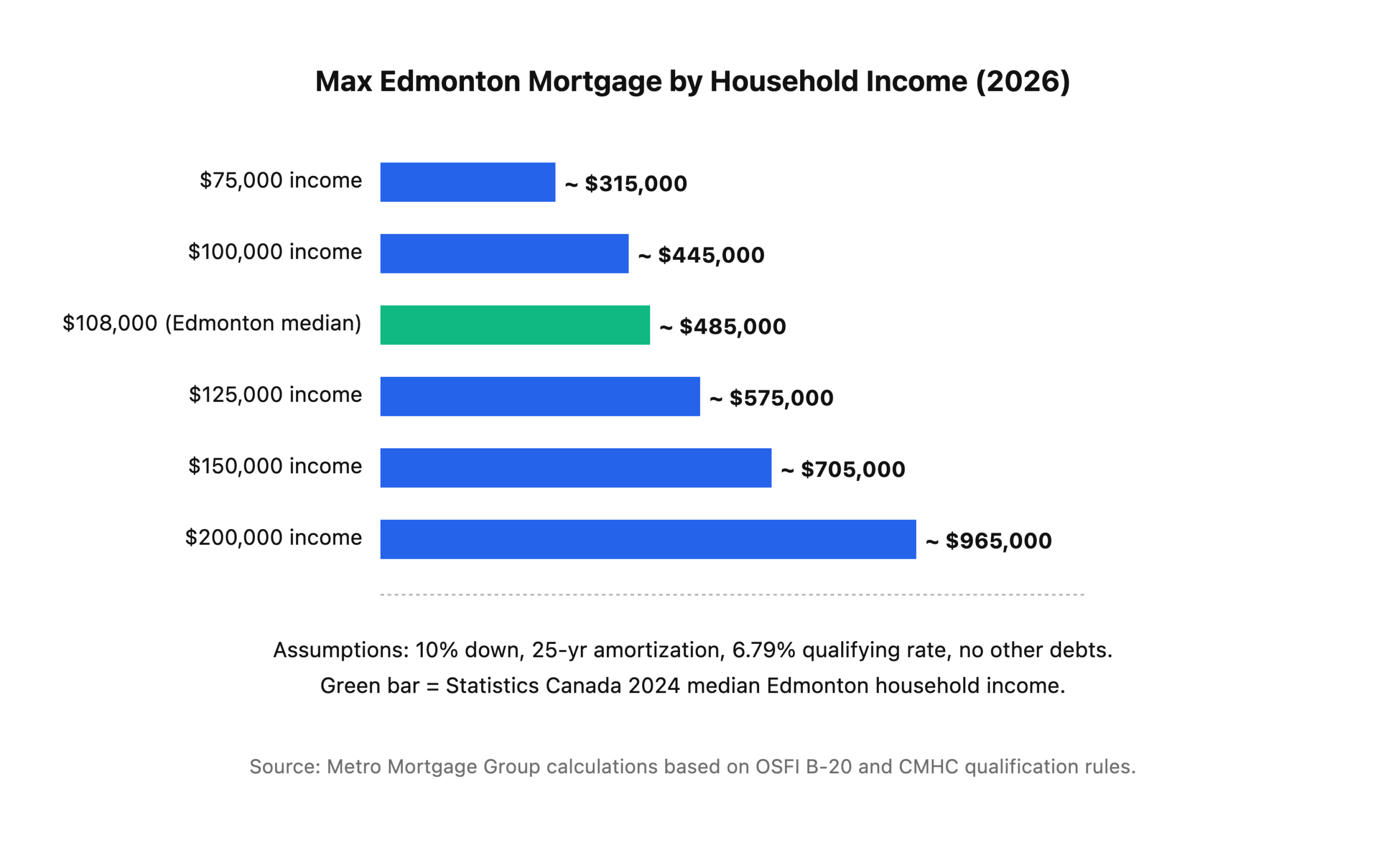

At 2026 stress-test rates, a $108,000 Edmonton household qualifies for a mortgage of roughly $485,000 assuming minimal other debts and 10% down (OSFI, 2024). That number moves up or down quickly based on car loans, credit card balances, and Edmonton’s property tax and heating costs, which lenders fold directly into your qualifying ratios.

Here’s roughly what Edmonton households at different income tiers can qualify for in 2026, assuming a 5-year fixed contract rate of 4.79%, qualifying rate of 6.79%, 25-year amortization, 10% down, and no other debts:

The numbers look generous until you plug in a car payment and a credit card balance. Add a $550/month car loan and a $3,000 credit card balance, and that $108,000 household’s qualifying amount drops from $485,000 to roughly $410,000 — a $75,000 haircut triggered by a single payment.

What Are GDS and TDS Ratios, and Why Do They Decide Everything?

Canadian lenders use two hard caps on every mortgage approval: Gross Debt Service (GDS) ratio of 39% and Total Debt Service (TDS) ratio of 44%, as set out in CMHC and mortgage insurer qualifying guidelines (CMHC, 2025). Your qualifying mortgage is simply whichever of those two ratios you hit first — and in Edmonton, it’s almost always TDS because of consumer debt.

GDS: Your Housing-Only Ratio

GDS is the share of your gross monthly income that goes toward housing costs only:

- Mortgage principal and interest (at the stress-tested qualifying rate)

- Property tax

- Heating costs

- 50% of condo fees (if applicable)

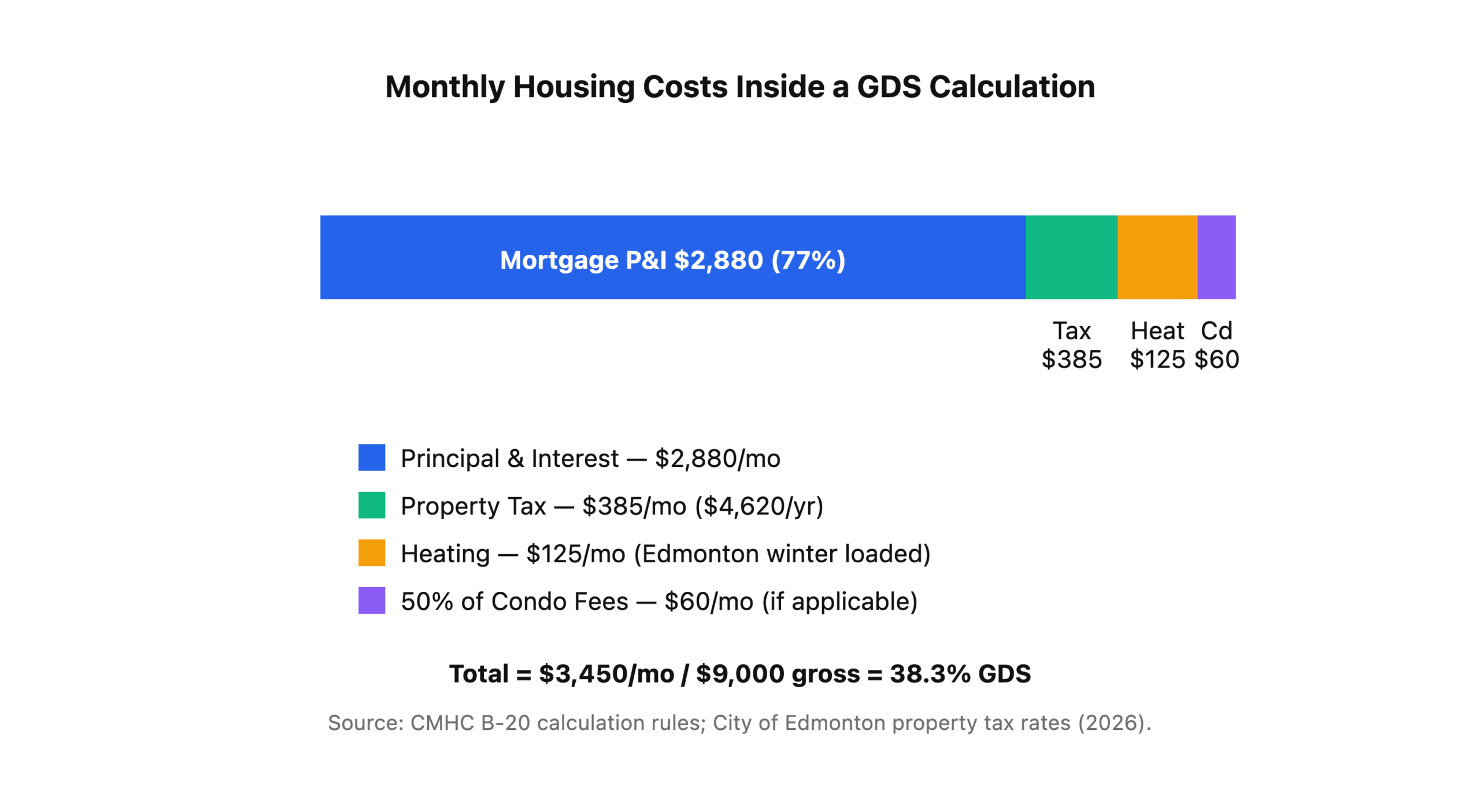

Divide that total by your gross monthly income. If the result is under 39%, you pass the GDS test. Here’s how those four components typically break out for a median Edmonton home:

Notice how much of the GDS calculation is not the mortgage payment. Property tax and heating alone eat $510/month on a typical Edmonton home — that’s enough to reduce your qualifying mortgage by roughly $75,000 compared to a lender that somehow ignored those costs. Edmonton’s harsh winter heating bills are factored in whether you like it or not.

TDS: Your Total Debt Ratio

TDS adds every non-housing debt obligation on top of GDS:

- Car loans and lease payments

- Credit card minimums (calculated at 3% of balance, not the actual minimum)

- Student loans

- Lines of credit (3% of limit, even if zero balance)

- Child support and alimony

Divide the new total by gross monthly income. If the result is under 44%, you pass. This is where most Edmonton buyers get trimmed. A $550 car payment consumes 6.1% of a $108K household’s TDS headroom all by itself.

What Is the Mortgage Stress Test and How Does It Affect Edmonton Buyers?

Under OSFI B-20, every federally regulated Canadian lender must qualify you at the greater of your contract rate + 2% or the 5.25% qualifying floor (OSFI, 2024). In April 2026, with 5-year fixed contract rates around 4.79%, that means you’re actually being tested at 6.79% — not the rate you’ll pay.

Here’s what the stress test does in real Edmonton numbers. On a $108K household with 10% down and zero other debts:

- Qualifying at the actual 4.79% contract rate = you could borrow ~$580,000

- Qualifying at the stress-tested 6.79% = you can borrow ~$485,000

The stress test strips roughly $95,000 of borrowing power off the table. That’s not a bug — it’s the buffer Ottawa built in after 2016 so that if rates climb, you can still make your payment. You’ll feel frustrated at the pre-approval table and grateful at every renewal for the next 25 years.

For a deeper walkthrough, read our complete mortgage stress test 2026 guide.

How Do Down Payment, Credit, and Side Income Change Your Affordability Number?

Four inputs drive every Canadian mortgage pre-approval: gross income, existing debts, down payment, and credit score (CMHC, 2025). Change any one of them and your qualifying amount can swing by $50,000-$150,000 in either direction. Here’s how each one moves the needle for a typical Edmonton buyer.

Down Payment Size

Minimum down payment in Canada is 5% on the first $500K and 10% on the portion from $500K to $1.5M, up to a $1.5M purchase price cap for insured mortgages (Financial Consumer Agency of Canada, 2025). Under 20% down, you pay CMHC insurance (which actually increases your qualifying amount because the insurer backstops the lender’s risk). Over 20%, you avoid insurance premiums but your qualifying ceiling drops slightly. Most Edmonton first-time buyers qualify for more home with 10% down than with 20% down — counterintuitive but true.

For the full breakdown, see our Alberta down payment guide.

Credit Score

CMHC-insured mortgages require a minimum 600 credit score for at least one applicant, a threshold CMHC reverted to in July 2021 (CMHC, 2025). Below that, you’re looking at uninsured lending with 20%+ down and higher rates. Above 740, you unlock the sharpest rates on offer, which translates into roughly $15,000-$25,000 more qualifying mortgage on the same income. Read our Alberta credit score guide for the full picture.

Side Income: Bonus, Commission, Self-Employed

This is where Edmonton buyers get surprised. Lenders apply a “haircut” to any income that isn’t guaranteed base salary:

- Bonus and commission income — typically averaged over the last 2 years, not the most recent year

- Overtime — often averaged or discounted 15-30% depending on lender

- Self-employed income — based on 2-year average of net business income from line 13500 of your T1, not gross revenue

- Rental income — typically 50-80% of gross rents, depending on the lender

Imagine an Edmonton energy-sector buyer pre-approved at $620K based on a $165K T4 income, then a spouse’s commission income adds another $85K on paper — but the lender only counts $52K of that commission after the 2-year average haircut. The file closes at $575K instead of the $720K originally chased. Commission and bonus income always needs a conservative projection.

How Does Edmonton Affordability Compare to Toronto and Vancouver?

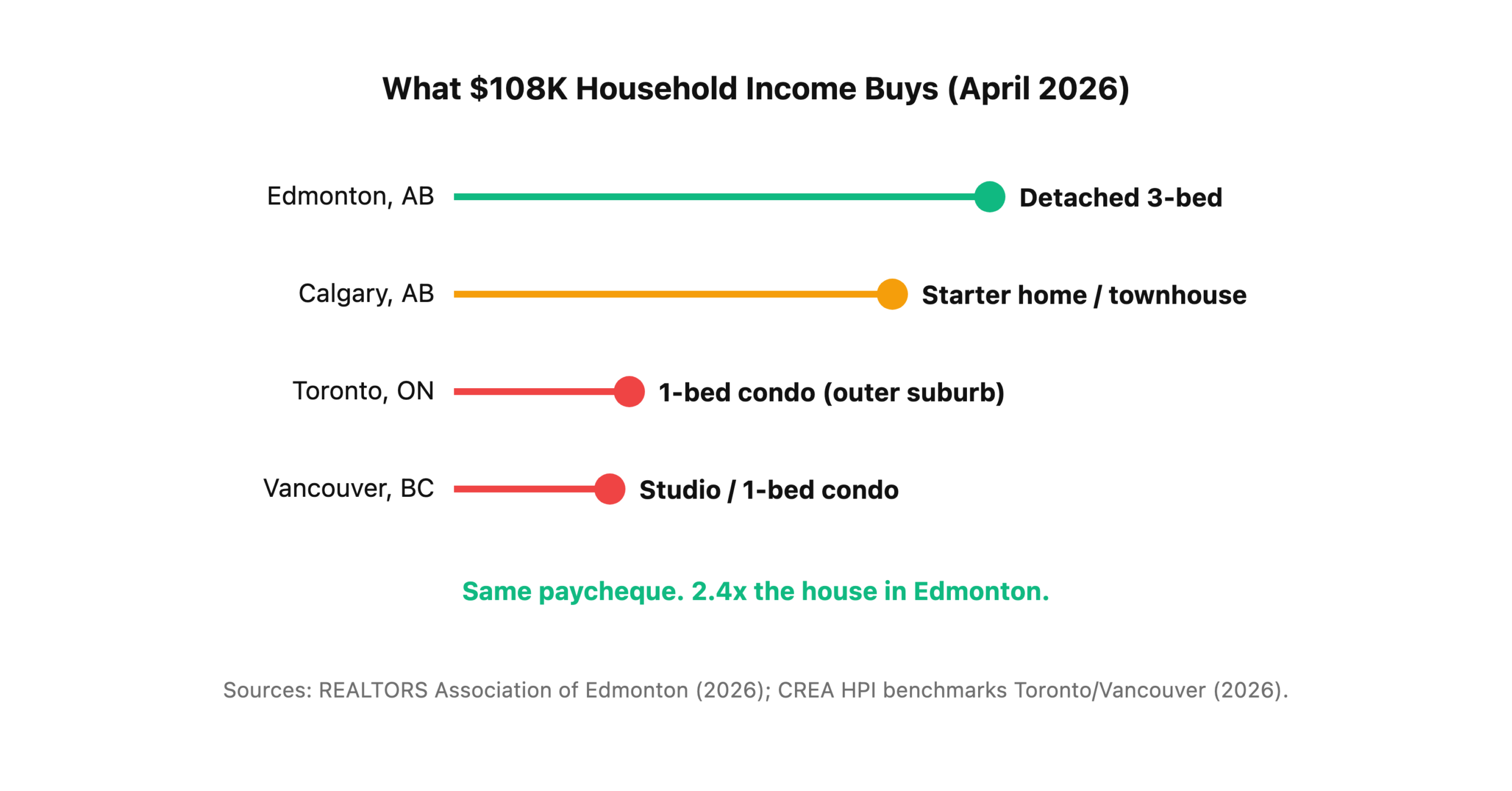

On a $108,000 household income, an Edmonton buyer can afford roughly 2.4x more home than the same family in Toronto and 2.2x more than in Vancouver (REALTORS Association of Edmonton, 2026). That’s not because lenders are more generous in Alberta — the B-20 rules are identical nationwide. It’s because Edmonton home prices are roughly 40% of Toronto’s on comparable property types.

The Edmonton affordability advantage is structural, not cyclical. Even in 2014 at peak oil, Edmonton detached prices barely cracked $400K while Toronto was already at $550K. The spread between Edmonton and Toronto hasn’t narrowed in two decades. That’s the real reason Alberta keeps attracting interprovincial migrants — the B-20 math works here in a way it simply can’t in Ontario or BC.

What’s the Difference Between What a Bank Approves and What You Should Actually Spend?

The bank’s maximum mortgage is calculated off gross income before tax, but you pay your mortgage with after-tax dollars — which is why most Edmonton households feel stretched at 35% GDS even though mortgage insurer guidelines allow 39% (Financial Consumer Agency of Canada, 2025). There’s a meaningful gap between the “bank max” and the “lifestyle max,” and the smartest buyers we work with target the lower number on purpose.

Run the math for a $108,000 Edmonton household:

- Gross monthly income = $9,000

- Take-home after Alberta tax + CPP + EI ≈ $6,600

- At 39% GDS on gross, housing = $3,510 = 53% of take-home

That leaves roughly $3,100/month for groceries, gas, child care, insurance, savings, RRSP, retirement, vacations, and every other line item a real family has. Most households hit the wall well before the bank does.

A healthier Edmonton target is 32-34% GDS, which on a $108K household works out to roughly $430,000-$445,000 in mortgage. You leave $40,000-$55,000 of qualifying room on the table and keep your monthly breathing room. Your future self will thank you at every renewal.

Ready to Get Your Actual Edmonton Affordability Number?

The qualifying calculators online are useful for ballpark — but they can’t account for your car loan terms, your spouse’s commission history, or whether your lender of choice uses a 3% or 3.5% credit card minimum assumption. A proper Metro Mortgage Group pre-approval runs the full B-20 math on 30+ Canadian lenders and shows you the actual maximum three different ways: insured, conventional, and stress-tested. It’s free and takes about 15 minutes. Call 780-974-1270 or email info@MetroMortgageGroup.ca.

For the full context on buying your first Edmonton home, start with our complete first-time home buyer Edmonton guide. Once you know your number, line it up against Alberta closing costs in 2026 to build your total cash-to-close budget.

Frequently Asked Questions

How much mortgage can I afford on a $100,000 Edmonton salary?

A single earner on $100,000 in Edmonton with no other debts and 10% down qualifies for roughly $445,000 at April 2026 stress-test rates (OSFI, 2024). Add a $500/month car payment and that drops to approximately $375,000 — a $70K swing from a single line of debt.

What’s the 39% GDS rule in Canada?

Gross Debt Service ratio caps housing-only costs at 39% of gross income — mortgage principal and interest, property tax, heating, and 50% of condo fees (CMHC, 2025). Edmonton’s typical property tax ($350-$400/month) and winter heating ($100-$150/month) together consume roughly 6% of a median household’s GDS room before the mortgage payment is even counted.

Does my credit card balance really affect how much I can borrow?

Yes, significantly. Canadian lenders calculate credit card payments at 3% of the outstanding balance (not the actual minimum payment) when computing TDS (CMHC, 2025). A $10,000 credit card balance adds $300/month to your TDS calculation — enough to reduce your qualifying mortgage by roughly $45,000 on a typical Edmonton file.

Should I max out what the bank approves?

Almost never. CMHC and mortgage insurer guidelines cap housing at 39% of gross income, but after Alberta tax and CPP that’s roughly 53% of your actual take-home pay (Financial Consumer Agency of Canada, 2025). Most Metro clients target 32-34% GDS, which on a $108K household means borrowing about $40,000-$55,000 less than the maximum but preserves room for groceries, savings, and life.

How does self-employed income affect Edmonton affordability?

Lenders use your 2-year average net business income from line 13500 of your T1, not gross revenue (CMHC, 2025). A self-employed Edmonton buyer showing $120,000 gross but writing down to $72,000 net will qualify off the $72K number — roughly $320,000 in mortgage. Alternative “Business for Self” lenders offer higher qualifying treatment at slightly elevated rates.

About the author: Daniel De Sousa is co-owner of Metro Mortgage Group and has helped Edmonton and Alberta families secure mortgages since 2011. Metro Mortgage Group has earned 229 five-star Google reviews serving Edmonton, Calgary, and greater Alberta.

Last updated: April 29, 2026